With interest rates rising and debt capital becoming less plentiful, some commercial real estate developers might want to look into the viability of including C-PACE (Commercial Property Assessed Clean Energy) financing in their capital stack. This relatively new loan program offers fixed-rate, long-term, non-recourse, non-dilutive financing for up to 30 years to pay for energy- and water-related features that improve a building’s operating performance in both ground-up and value-add projects. Currently, the program offers a 7 percent interest rate.

The features that can qualify a project for C-PACE financing include improvements to the roof, building envelope, lighting, HVAC systems, insulation and plumbing systems. They also include resiliency upgrades in certain markets prone to adverse weather events, such as inclusion of seismic and hurricane infrastructure in California and Florida, respectively, and the labor required to install them. Additional components that would improve energy and water efficiency, such as electrical upgrades, are also included. The only caveat is that improvements must exceed those required by the existing building code or, when it comes to projects based in California, meet the state’s Title 24 requirements for energy conservation.

Lenders are able to offer funding with favorable terms for C-PACE loans because C-PACE is a public-private partnership that uses private capital, but taps into the public benefit funding mechanism typically used to finance public infrastructure such as improvements to city roads, notes Jessica Bailey, CEO and co-founder of Connecticut-based Nuveen Green Capital (NGC), one of two major C-PACE lenders nationally.

This mechanism provides low-cost, long-term funding for infrastructure assessments with no down payment and repayment as a benefit assessment on the property tax bill over a term that matches the life of improvements and/or new construction infrastructure, typically 20 - 30 years. Similar to other tax assessment funding utilized by homeowners or private businesses to pay for infrastructure upgrades, C-PACE loans are also transferrable to new owners upon sale of the property.

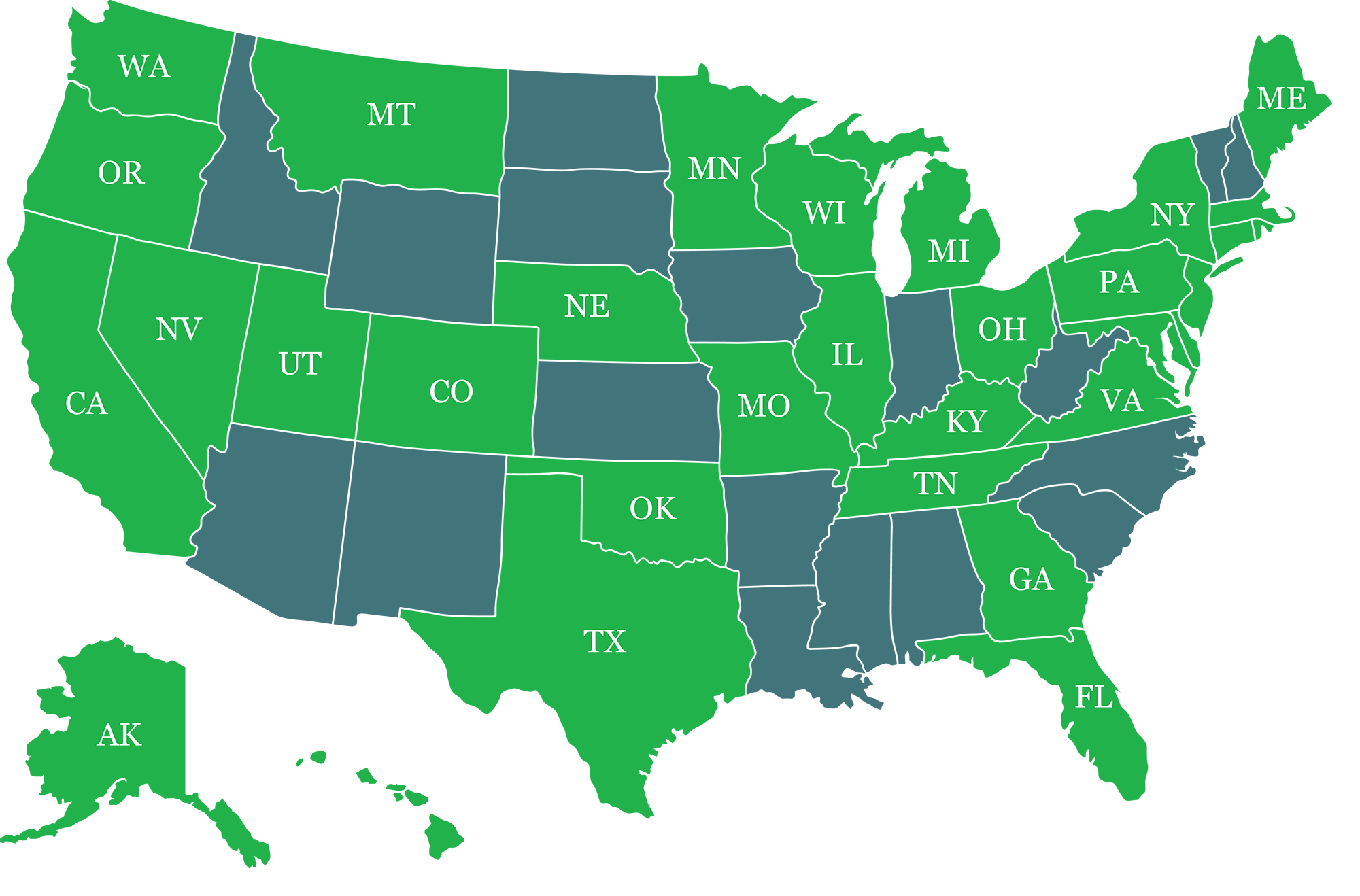

However, C-PACE loans are only available in states that have passed legislation that recognizes energy and water efficiency upgrades as a public benefit to enable tax assessment financing for this purpose. So far, 37 states plus the District of Columbia have adopted C-PACE enabling legislation, notes Bailey. Over the last decade, C-PACE programs have resulted in more than $2 billion in private capital investment in commercial building upgrades in more than 20 states.

States adopting C-PACE enabling legislation

In the current lending environment, C-PACE loans can take the place of high-interest mezzanine financing, says Jason Schwartzberg, president and co-founder of MD Energy Advisors, a provider of energy management and efficiency solutions. Additionally, C-PACE loans can be leveraged to fill an equity gap or pay for project cost overruns, Schwartzberg says, noting that the program offers funding retroactively for one to three years, depending on the state where the project is located.

Although C-PACE funding is available for commercial properties across all sectors, as long as they exhibit strong cashflow at stabilization, Schwartzberg notes that in the current environment, self-storage, hotels and senior housing projects could fit the program’s guidelines particularly well because they might have a better chance of hitting those cashflow goals once stabilized.

The value of the C-PACE loans is based on the project’s energy savings, sponsor’s credit rating and underwriting that looks for sufficient cashflow to service all debt, according to Bailey. NGC has done C-PACE deals in excess of $10 million, she adds.

For example, the company recently provided developer Matthew Gordon, who was building a $28-million, mixed-use project in Carlsbad, Calif., with $10.1 million for the project’s energy and water efficiency features. Gordon notes that the C-PACE loan reduced the interest expense on the first lender’s construction loan and featured a built-in 30-year, amortized loan for the commercial condominium portion of the development. NGC tailored its loan to pay off the construction loan with the sale of the condos and keep the long-term financing in place for the project’s commercial space, he says.

Another developer, Ian Horwitz, a principal with Baltimore-based Equity Warehouse, accessed C-PACE loans to fund improvements to a 76-unit apartment complex and renovate a historic 80,000-sq.-ft. mixed-use property consisting of six dilapidated buildings that include 40,000 sq. ft. of office space and retail and entertainment components—a wedding venue, a beer brewery and a Karate studio.

The seller of the 76-unit apartment complex wanted to do owner financing, so the $700,000 C-PACE loan bridged capital costs “for upgrades we were going to do anyway,” including plumbing improvements, such as installing low-flow faucets and toilets, reinsulating the roof and installing heat-reflective roof sheeting, Horwitz says.

Improvements to the historic mixed-use project were funded with a $1.2 million C-PACE loan. Horwitz notes that it not only funded common energy improvements, like insulation, energy-efficient windows and electrical and mechanical upgrades, the loan unexpectedly funded regrouting of the brick façade with new mortar because it covers the building envelope.

The project is still under construction and Horwitz says that a major benefit of the program is that loan interest can be capitalized there by delaying repayment for one to three years until the project is completed and stabilized with lease-up.

Developer Eugene Poverni, a principle at Maryland-based Poverni Sheikh Group, received $3 million in funding at 5.75 percent interest from C-PACE last June, just as the Fed began raising rates, to finance energy- and water-related components of a 120,000-sq.-ft., ground-up self-storage project in Connecticut. Calling this a “smart program,” Poverni notes that C-PACE funding, which provides incremental access to funds as the project progresses, improved the debt ratio for the $20-million project, which was also funded with a $12-million, floating-rate bank loan.

C-PACE financing can provide up to 20-30 percent of a project’s total cost, but Schwartzberg notes that there are three hurdles to qualifying for this loan. First, financial underwriting must demonstrate the project will generate enough cashflow to service both the primary mortgage and the C-PACE loan. Second, the project must pass a technical review, which uses permit plans, the schedule of values and COMcheck forms to quantify and confirm the project’s energy- and water-related content exceeds local building code. And third, the borrower must ascertain written consent for a C-PACE loan from the primary mortgage lender.

So fa, more than 300 national, regional and local mortgage lenders across the U.S. have consented to C-PACE financing, Schwartzberg says. He notes that consenting to C-PACE loans is often in the primary mortgage lender’s best interest, as C-PACE improvements tend to lower operating costs, and the lender will maintain their lien position in the event the borrower defaults on the loan or files for bankruptcy. Therefore, if the property goes into foreclosure, it can be sold free and clear, but subject to the C-PACE assessment. As the C-PACE assessment is non-callable/accelerable, any delinquent portion of the C- PACE assessment would be due and payable by the winning bidder. Schwartzberg also notes that if the property should go to tax sale, everyone with an interest in the property is notified in plenty of time to cure the problem.