For the last couple of years, the independent broker/dealer channel has been in a tough spot. Post-crisis, IBDs have been buried by increased compliance burdens, greater demand for investment in technology and a lot of additional risks and costs associated with a broad move into alternative investments.

In the full bloom of the economic recovery, we’d like to say that things are looking better—that firms are more profitable—but it isn’t so. Margins remain thin in this business. Most small b/ds have profit margins at around 2 percent, compared to 2 to 4 percent margins for mid-sized firms.

“It has always been the case in the broker/dealer business that margins have been challenged,” says Philip Palaveev, founder of The Ensemble Practice LLC.

“Much like farmers are never happy with the weather, I don’t think broker/dealers are ever happy with their margins.”

Payouts for independent advisors are steadily rising toward 90 percent, Palaveev says. And with expenses in the 12 to 18 percent range, depending on the firm’s size, the payout grid doesn’t leave much room to operate the business.![]()

In addition, those expenses for independent firms are variable, not fixed, because so much is being paid out to the rep, says Joel Jeffrey, equity analyst at Keefe, Bruyette & Woods, Inc., who covers LPL Financial and Raymond James.

“You’re never going to see great pre-tax margins out of this business,” he says. “The math just doesn’t really work because you’re not getting the operating leverage on the upside in this model.”

At the same time, interest rates remain low, so whatever revenues b/ds were earning from cash accounts have dried up. While interest rates on longer-term securities have started to rise, many firms are holding clients’ cash in short-term securities and not seeing any benefits yet, Jeffrey says.

On the Bright Side

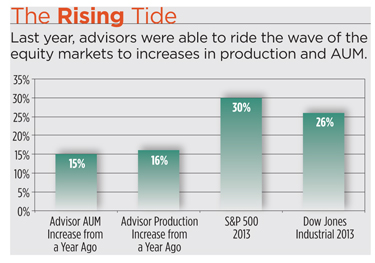

While it will never be a high-margin business, there are some signs that the environment is improving. For one, the S&P 500 Index was up 30 percent last year, providing a lift to b/d and advisor profits. On average, advisor productivity increased 16 percent from a year ago, while assets under management grew 15 percent, according to REP.’s annual Independent Broker/Dealer Report Card.

CEOs are also feeling more confident in the future outlook of the business; they’re starting to invest more in the firm infrastructure and upgrading the advisor service model, says Matt Lynch, principal at Tiburon Strategic Advisors.

“The executives of these firms have taken action to contain cost because we’ve lived in this low interest rate environment for quite a number of years,” says Lynch.

The movement towards fee-based business is another positive development for broker/dealers. On average, fees accounted for nearly 49 percent of independent advisors’ income in 2013, compared to 46 percent from commissions, according to the IBD Report Card. That compares to last year’s survey, when advisors’ mix of business was 40.5 percent fees and 54 percent commissions, on average.

“It’s kind of ironic that the modern broker/dealer is a giant RIA,” Palaveev says.

Firms with the highest percentage of fee-based income included Cambridge Investment Research, Commonwealth Financial Network, Raymond James Financial Services and NFP Advisor Services Group. They were also among the firms with the highest overall scores. (See “Smaller Firms, Happier Advisors

Can it Last?”.)

A firm can get 40 to 50 percent better margins on advisory business, says Steve Dunlap, executive vice president of wealth management at Cetera Financial Group.

The valuations of IBDs are also going up, with recent deals seeing multiples higher than they were three to four years ago, says Tiburon’s Lynch.

Nicholas Schorsch, head of RCS Capital Corp. (RCAP), recently purchased Cetera from private equity firm Lightyear Capital for about one times Cetera’s trailing 12-month revenue. Because of their small profit margins, IBDs tend to sell for 30 to 40 percent of their trailing 12-month revenue.

What has changed—and perhaps the reason prices are going up—is the institutional interest in b/ds, Palaveev says.

“There’s a new wave of buyers who are opportunistic, private equity-financed buyers, who previously would ignore this industry,” Palaveev says. Like real estate speculators, however, opportunistic buyers tend to come in quickly and sometimes leave just as fast, he warns.

“It’s a thriving, growing industry right now. But you know how they say that the seeds of destruction are sown in good times.”