Many financial and estate planners will recall the “Golden Age” of the charitable remainder trust (CRT) that took place from the mid-1980s until the late 1990s. Many welcomed it as concrete evidence of the unfolding of the “Great American Wealth Transfer” being touted at the time.

This boom in charitable gift planning began shortly after the passage of the Tax Reform Act of 1986—legislation that ushered in historically high capital gains rates, along with ordinary tax rates of 33 percent or more.

At the same time, investment values were growing at record rates, which many assumed would continue indefinitely. In that environment, many planners began to see CRTs as a welcome way to enjoy immediate income tax savings while bypassing higher capital gains rates and “unlocking” income from highly appreciated, low yielding assets.

An Era of Growth

During this period, advisors created large numbers of CRTs for financial and tax reasons, and charities created them as effective tools for structuring gifts to fuel increasingly ambitious campaigns and other fundraising efforts.

According to annual reports issued by the Council for Aid to Education, colleges and universities reported a more than four-fold increase in the face value of CRTs and other deferred gifts funded during that time period. Other giving by individuals grew at just half that pace.1

During that same time period, an increasing number of charitable trusts were structured with very large payouts and decades-long time frames, resulting from younger individuals receiving payments for life. Trusts were reportedly created to last for young children’s lifetimes and resulted in very small charitable remainder percentages—in some cases close to zero.

Multiple Impediments

These perceived abuses led to new provisions in the Taxpayer Relief Act of 1997 that required a maximum CRT payout rate of 50 percent and a minimum charitable deduction of 10 percent. In retrospect, this legislation contributed to a lessening of interest in CRTs. This decline was especially true of trusts motivated primarily by the desire to bypass or delay capital gains taxes and build tax-free income over decades-long time periods.

On top of the newly restrictive legislation, the investment market correction that began with the bursting of the “tech bubble” in 1998 also reduced the amount of appreciated assets available to fund CRTs.

Lower income, capital gains and estate tax rates enacted in 2001 further reduced the attractiveness of CRTs as tax planning tools. With lower income tax rates, maximum federal capital gains tax rates at 15 percent and the practical time limitations placed on CRTs by the 1997 legislation, CRTs no longer held the same attraction for planners as they had during the previous decade. Higher thresholds for the imposition of federal estate taxes that were phased in during the 2000s served to lessen the attraction of CRTs for estate tax planning purposes.

At the same time, there was a demographic “echo” of the 20-year downturn in U.S. birth rates between 1925 and 1945. This slump resulted in fewer individuals in the prime age range when CRTs are typically created. The combination of these factors led to a number of years in which the growth of CRTs slowed and flattened.

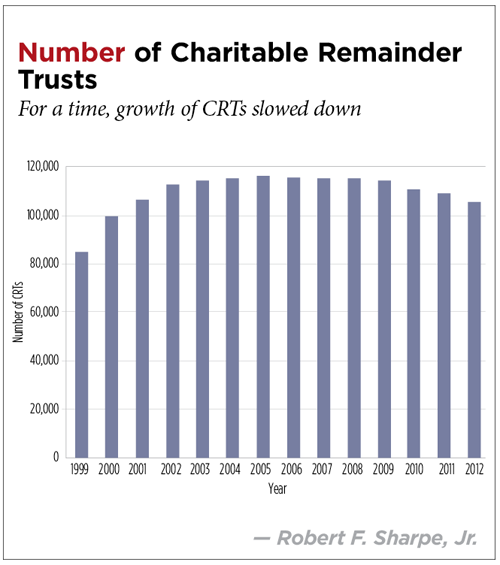

According to Internal Revenue Service figures, the total number of CRTs in existence actually shrank slightly during between 2007 and 2012. (See “Number of Charitable Remainder Trusts,” this page.)

Given the multiple headwinds facing CRTs during the past decade, one might be surprised the numbers haven’t shrunk to an even greater extent.

A New Golden Age?

Many factors that limited the growth of CRTs in recent years are now simultaneously reversing course and combining to create what may well be the largest growth period for these trusts in history.

From a financial planning perspective, consider:

1. Over the last five years, since the depths of the post-2008 market decline, the Dow has increased by over 150 percent.

2. Higher capital gains rates and the Medicare contribution tax now imposed on gains have increased the effective federal tax rate on realized capital gains from 15 percent to 23.8 percent. The rate for art and other tangible personal property can be as high as 31.8 percent.

3. The combination of higher taxes on capital gains, federal tax on income over 40 percent in some cases and state tax levies have resulted in tax incentives associated with CRTs that now approach or exceed those of the 1990s.

4. Lower investment returns for a growing senior population make the prospect of unlocking additional retirement income through a CRT an attractive alternative.

When considering the benefits of a CRT from a fundraising perspective, the following factors driving growth are in play:

1. Studies indicate the average age of an individual creating a CRT is 68. Trusts remain in existence for 15 years, on average. For many, that’s an acceptable time frame for realization of return on investment.

2. The first of over 72 million baby boomers will reach age 68 this year, and this growth will continue for the next two decades.

3. When dealing with older donors with substantial donative intent, CRTs are increasingly seen as an alternative to gifts via wills and other revocable gifts that may not offer the same level of financial security as an irrevocable trust.

4. Those seeking gifts from wealthier baby boomers are now beginning to encounter natural resistance based on stage-of-life factors (for example, the worry about not having enough for retirement, which could last 25 years; concerns about children in their 20s coming home unemployed and needing financial support or health insurance; or the worry about parents getting ill and depleting their own finances). As a result, gifts that won’t be completed until the death of one or more individuals are taking on increased importance to donors considering major gifts.

5. CRTs are also becoming attractive to older donors who no longer anticipate being subject to federal estate tax. CRTs offer a way to make testamentary charitable gifts that will no longer yield estate tax benefits, while providing lifetime tax benefits. Other traditional tax incentives remain, including income tax deductions, bypass of capital gains tax, tax-free diversification and growth of assets, professional asset management and some degree of asset protection.

Lessons to be Learned

What can we learn from the last Golden Age of charitable planning as we move forward? First, experience from 1987 through 1997 indicates that, if planners push the envelope on CRTs and similar gift plans, Congress can be expected to take action to restrict perceived abuses of the law.

The good news is that Congressional leaders now appear to believe that earlier legislation was sufficient to prevent a repetition of the events that gave rise to it.

Note that the recent Camp Proposal for tax reform didn’t include any provisions that would place direct limits on CRTs or other split-interest charitable gifts. (For more information on the Camp Proposal, see my article, “Camp Proposal and Charitable Giving,” in the May 2014 issue of Trusts & Estates, p. 11.)

Unlike the earlier CRTs from the Golden Age, there’s now a generation of estate and financial planners who have matured during an environment in which many population centers have a planned giving council made up of planners and non-profit representatives. There’s much greater awareness on the part of both groups as to how charitable trusts are structured and what abuses to watch for.

Another change over the past 25 years is the growing availability of fiduciary services to supplement the efforts of charities that often served in this capacity in the past. Many wealthy individuals and their advisors now have relatively ready access to sophisticated charitable trust fiduciary services, aided by more advanced software and automated tax preparation tools.

In light of increased professional knowledge and greater access to services required to create and manage CRTs, a greater degree of cooperation is needed among nonprofits raising funds from those donors and professionals advising and raising funds from both clients and donors.

From the advisors’ perspectives, there needs to be an increased awareness of the charitable motivations driving client interest in these trusts and the fact that, by definition, a gift is based on a combination of complex personal motivations, rather than a desire to profit.

Gone are the days when advisors commonly illustrated to clients how they could come out ahead when creating a CRT, so donative intent will be paramount when considering the structure of these types of gifts.

From the charities’ perspectives, fundraisers who are working with high-net-worth individuals considering larger gifts need to be more aware of the concerns that can naturally quell interest in those gifts.

For example, a donor who may have completed a seven-figure gift 10 years ago, when he was in his early 50s, may now be approaching retirement age. The donor may be more concerned about the need to preserve assets for a potentially long retirement. In those cases, charities must be prepared to help donors and advisors structure gifts that meet these concerns, while also providing for a reasonable gift that offers real economic value to an institution.

Regardless of their age, donors may increasingly be interested in gifts that last for a period of years sufficient to meet natural concerns. For example, a 60-year-old may need additional income only for the 10-year period before he begins mandatory withdrawals from his retirement plan at age 70. In that case, he might, for example, decide to fund a CRT with a fixed payout rate of

10 percent for a period of just 10 years.

While such a trust may have a relatively high payout compared to a traditional trust that’s structured for life, it has a natural “stop” of its term before the trust results in unacceptable levels of erosion of principal.

For trusts that are designed to last for the lifetime of younger donors, it’s also possible to carve out an income interest. This strategy will result in an immediate and ongoing stream of income for the charity prior to receiving the remainder.

Take, for example, a 55-year-old couple with a 34-year life expectancy. If they were to fund a 5 percent straight charitable remainder unitrust with $5 million, and the trust earns 8 percent total return over time, the trust will grow to $13.7 million dollars over their anticipated life expectancy.

However, if the charity to be benefited in the future is earning a total return of 8 percent on its endowment funds and considers its opportunity cost, while awaiting the remainder, then the present value of the remainder is just over $1 million.

In addition to that economic reality, the charity will have to wait 34 years before receiving any funds that can be expended for charitable purposes. Charities devoted to meeting urgent needs can’t be expected to welcome such gifts.

In addition, the donor may not understand why the charity may only wish to credit the $1 million present value of the trust as a campaign gift because, in the donor’s mind, he’s transferred $5 million to the trust.

If the donor in this situation decided to include a provision for an immediate and ongoing income stream for the charity, the picture changes. In the case of the trust above, with a 5 percent payout, if the charity begins to receive 20 percent of the income from the trust, the first year the income would be 20 percent of $250,000, or $50,000. The donor receives $200,000.

If the trust earns the anticipated amount, both the income to the donor and the charity will continue to grow, and the donor’s share will build back to the $250,000 level within eight years.

The charity could expect to receive income of over $3 million during the anticipated 34-year period the trust is in existence, prior to receiving the remainder of nearly $14 million. The charity would, from the outset, enjoy the equivalent of a $1 million endowment with a 5 percent spend rate and could be expected to credit the donor with a much larger campaign gift.

Keep in mind that the money going to charity in this case doesn’t pass through the donor’s taxable income. The charitable portion of the trust payments won’t be subject to any deduction limitations on traditional charitable gifts that might apply as a result of recently proposed adjusted gross income limits, maximum limits on tax brackets to which deductions apply or existing Pease reductions. Not receiving income is the same as receiving it and fully deducting it.

If restrictions result in a floor or ceiling on charitable deductions in the future, the structure of this trust will serve as a very effective planning tool for a donor who wishes to make his charitable gifts from funds that aren’t diminished by taxation.

Asset Management Issues

Charitable entities acting as trustees of CRTs should also be cognizant of the fact that their donors often have their asset portfolios managed by trusted advisors. In many cases, these financial professionals benefit from fee structures based on management of a client’s total assets.

This setup can lead to a disconnect between the interests of charities and donors and the asset managers. Charities may also be seeking to maximize their amount of funds under management. In addition, charities want to be assured that the assets in the trust are being managed prudently, so that the charity can be confident in extending credit in fundraising campaigns for those particular gifts.

Careful discussion and attention to creating investment parameters and risk management guidelines that are understood and agreed to by donors’ asset managers can help alleviate these concerns.

It behooves charities to work closely with donors and their financial advisors. Otherwise, trusts may be created without input from the charity. The donor may then present the charity with the trust as a fait accompli, along with a request for unrealistic credit in a campaign.

Given the factors outlined in this article, it’s more critical than ever for all parties involved in a proposed gift to work together in good faith. They can achieve results that overcome seemingly conflicting goals for charitably minded individuals and help charities benefit from all of the factors that should lead to unprecedented sums being devoted to charitable uses in coming years.

Endnote

1. Figures based on annual reports from Council for Aid to Education, http://cae.org/fundraising-in-education/category/vse-survey/.