In 2011, the news from abroad threatened to swamp global markets. Headlines warned that the Eurozone could implode. Pundits predicted that China would suffer a hard landing, as the country’s growth machine faltered. But the worst did not happen. As investors gained confidence, global markets rallied. Take Europe. During 2012, Europe funds returned 20.9 percent, 5 percentage points ahead of the S&P 500, according to Morningstar. Foreign small growth funds returned 22.0 percent.

Now there is good reason to expect that foreign stocks will continue climbing. Plenty of Wall Street analysts expect that economies will grow in Europe and Asia this year. But clients may still be wary. They could reasonably argue that a foreign disaster could suddenly appear. To protect nervous clients, consider a low-risk international fund with a track record for excelling in downturns. By focusing on high-quality stocks or using other techniques, top funds limited losses during the turmoil of 2008 and delivered decent returns in recent rallies.

Is All About Risk Control

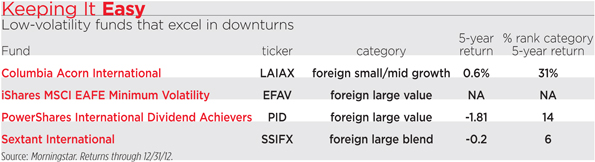

Among the safest choices is Sextant International (SSIFX). Portfolio manager Nicholas Kaiser favors rock-solid businesses that sell at modest prices. Kaiser looks for steady performers that can increase earnings at annual rates of 10 percent to 12 percent. He often holds big cash stakes when markets look hazardous. During 2008, Sextant kept most assets in cash. That enabled the fund to outdo 98 percent of peers in the foreign large blend category. By avoiding big losses, Sextant has compiled a sterling long-term record. During the ten years ending in 2012, the fund returned 11.2 percent annually, outdoing 94 percent of peers.

Lately Kaiser has become more bullish, and the fund has cut its cash stake down to 16 percent of assets. “We see plenty of opportunities outside the U.S.,” says Kaiser.

He is keen on Canadian markets, where commodities exporters are generating healthy profits. A favorite holding is Potash, which supplies fertilizer to farmers around the globe. The company should increase its profits as the world gets richer and demands more food, says Kaiser.

To control risk, balanced funds hold mixes of stocks and bonds. Typical portfolios focus on blue-chip stocks and high-quality bonds. Calamos Global Growth & Income (CVLOX) offers a different variation of the traditional package. The fund starts by keeping about half its assets in stocks. The rest of the portfolio goes mainly into convertible securities. Hybrid securities, convertibles offer bond-like yields along with some of the appreciation potential of stocks.

Convertibles come in a variety of flavors. Some securities pay high yields and are more like bonds, while other issues have lower yields and rise and fall like stocks. The Calamos portfolio managers typically stay in the middle of the convertible spectrum, keeping securities that offer two-thirds of the upside of stocks and only one-third of the downside. As a result of the strategy, the fund has outdone stocks in downturns, while trailing slightly in rallies. When the MSCI world index lost 5.6 percent in 2011, Calamos only declined 2.5 percent. Over longer periods, the caution has paid dividends. While the benchmark lost 1.2 percent annually during the past five years, Calamos returned 0.6 percent.

For its stock holdings, Calamos favors companies that can benefit as emerging markets grow and spend more on health care and consumer goods. A favorite holding is Novo Nordisk, a Danish pharmaceutical giant that provides treatments for diabetes. “They are the number one name in a business that is growing around the globe,” says Calamos portfolio manager Scott Becker.

Some new ETFs aim to limit losses by focusing on low-volatility stocks. An intriguing choice is iShares MSCI EAFE Minimum Volatility Index (EFAV). The fund emphasizes such steady blue chips as Nestle and drug maker Roche. The ETF has only been operating for a year, but it tracks a benchmark that has been running since 2002. Since its inception, the minimum volatility benchmark has excelled in downturns and outpaced the broad MSCI EAFE index by a wide margin. When the broad EAFE index lost 11.7 percent in 2011, the minimum volatility benchmark about broke even. So far the ETF has been living up to its promise. In the second quarter of 2012, the minimum volatility ETF dropped 1 percent, while the EAFE index lost 7.1 percent.

Morningstar analyst Alex Bryan cautions that the low-volatility fund should provide solid long-term returns, but it will not win every year. “You are probably going to lag during strong rallies,” he says.

Another low-volatility choice is PowerShares International Dividend Achievers (PID). Holdings in the portfolio must have increased their dividends for at least five consecutive years. Companies that pass the test tend to have steady cash flows and rock-solid balance sheets. Many holdings are dominant players that enjoy near-monopoly status. The portfolio has 20 percent of assets in reliable Canadian companies, including Canadian Pacific Railway and Canadian National Railway. The fund has 21 percent in stable telecoms, including China Mobile and Telefonica, a Spanish provider that is a major force in Latin America.

The giant holdings helped the fund to excel in the downturn of 2011 when it outpaced the EAFE benchmark by 9 percentage points. By avoiding big losses, the fund has surpassed EAFE by nearly 2 percentage points annually during the past five years.

Investors seeking a steady small-cap choice should consider Columbia Acorn International (LAIAX). The mutual fund focuses on companies that dominate niches and can grow consistently for years. “We prefer companies with good balance sheets and reliable sources of financing,” says Columbia Management's Chris Olson.

The steady approach has enabled the fund to deliver consistent results. Columbia Acorn outdid most peers during the downturn of 2008 and in the recovery of 2009. During the past ten years, the fund returned 14.0 percent annually, outdoing 80 percent of peers.

Olson likes REITs in Singapore. He says that the small nation has little debt and a solid economy. The real estate markets remain healthy because foreign corporations are establishing regional headquarter in Singapore. Holdings include Ascendas Real Estate Investment Trust, which owns premier office parks.

(Note: A previous version of this story mis-identified Chris Olson as the portfolio manager of the Columbia Acorn International fund. He is the portfolio manager of the Columbia Acorn International Select fund.)