As Andrew Berkin and I demonstrated in our book The Incredible Shrinking Alpha, and in the annual S&P Active Versus Passive Scorecards, the persistent underperformance of most actively managed funds has been well documented. But what’s the actual cost to investors of engaging active managers?

To answer that question, Moshe Levy, author of the study “The Deadweight Loss of Active Management” published in the July 2023 issue of The Journal of Investing, evaluated the performance of U.S. active equity funds based on their Sharpe ratios (which he argued is more relevant than alpha for most investors as a measure of utility) relative to the market (proxied by the S&P 500). Levy’s data sample is from the CRSP Survivorship-Bias-Free Mutual Fund Database for all U.S. domestic actively managed equity funds and covered the period from December 1991-March 2021. Here is summary of his key findings:

The aggregate annual loss to investors in U.S. active equity funds was $235 billion, the composite of an inefficient portfolio allocation of $186 billion and fees of $49 billion.

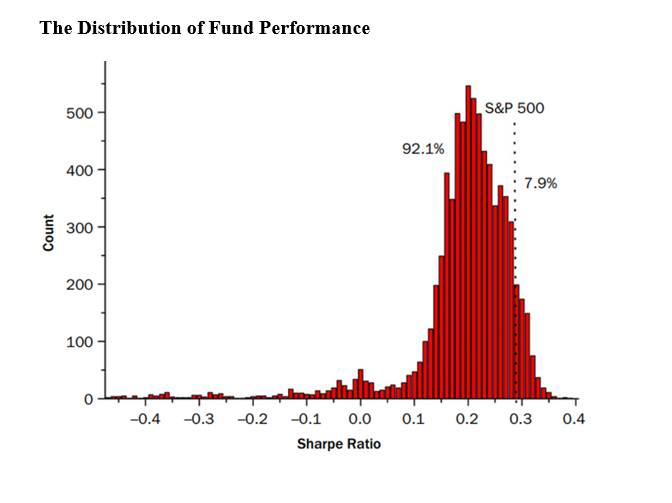

Most funds (92.1%) underperformed relative to the passive index.

There wasn’t a strong association between fund size and performance—the correlation between funds’ Sharpe ratios and size was only 0.098—an indicator of the difficulty in identifying outperforming funds ex ante.

A further indication of the difficulty in identifying ex-ante future outperformers was the relationship between performance over the period April 2011-March 2021—the R-squared between the performance over the first half and the second half was just 0.060, with most of that driven by the worst performers (excluding them, the R-squared fell to 0.028).

Outperformance, when it existed, was typically moderate; in contrast, underperformance could be spectacular. While the Sharpe ratio of the S&P 500 Index was 0.288 and the mean Sharpe ratio of active funds was 0.192, the maximum Sharpe ratio across all funds was 0.392 (outperforming by just 0.104) and the minimal Sharpe ratio was -0.475 (underperforming by ‑0.763).

Levy’s findings led him to conclude: “When choosing their funds, investors apparently attach too much weight to historical returns.” He also added this important insight: “It could be argued that the loss is actually higher [than $235 billion], because most individuals in the active equity mutual fund industry do not seem to be creating economic value, and the wealth transfer component actually reflects an opportunity cost for the economy—these individuals’ talents could be more productive elsewhere.”

Despite the enormity of the costs, Levy’s estimate, if anything, is too low. It does not account for the incremental burden of higher taxes incurred by active investors with taxable holdings.

Levy’s findings are consistent with those of Ken French, author of the 2008 study “The Cost of Active Investing.” His study covered the period 1980-2006 and included mutual funds, ETFs, hedge funds and institutional funds. French compared the estimated total amount society spends to invest with an estimate of costs if everyone invested passively—the difference is the cost of active management. He estimated that in 2006 the fees and expenses paid for mutual funds, investment management costs paid by institutions, fees paid to hedge funds and funds of funds and transaction costs paid by all traders was 0.75% of the value of all NYSE, AMEX and Nasdaq stocks. He also estimated that if all investors paid passive fees and there were no hedge funds, the cost of investing would have been just 0.09%.

The difference between the actual and passive estimates measured the cost of active investing: Active investors had engaged in a massive transfer of wealth—about $80 billion annually based on the then-market capitalization of about $12 trillion—from their own wallets into those of the purveyors of actively managed products and market makers. At the end of 2022, the total market capitalization of U.S. stocks was about $40 trillion (3.33 times what it was in 2006). Proportionally, that would increase French’s estimate to about $267 billion a year, close to Levy’s estimate.

Investor Takeaways

The most effective way to influence behavior in the long run is through education—providing investors with the evidence from peer-reviewed research. The dissemination of the findings on the performance of active managers has influenced investors, as the proportion of wealth invested passively has consistently grown since John Bogle introduced the first public index fund in 1975. However, much of that growth has been at the expense of direct holding in stocks. Active managers still have trillions of dollars under management in U.S. stocks. So, there is a long way to go.

With all that said, we don’t want active managers to disappear, as their efforts at price discovery help keep markets and capital allocation efficient. Thus, while each individual investor, acting in their self-interest, should abandon the quest for the holy grail of outperformance, we need hope to ‘spring eternal’ with at least some investors so that passive ones can be ‘free riders.’

Larry Swedroe has authored or co-authored 18 books on investing. His latest is Your Essential Guide to Sustainable Investing. All opinions expressed are solely his opinions and do not reflect the opinions of Buckingham Strategic Wealth or its affiliates. This information is provided for general information purposes only and should not be construed as financial, tax or legal advice.