Economic theory suggests that political uncertainty impacts countries’ expected cash flows. Highly rated (low political uncertainty) countries exhibit higher expected cash flows. The same holds true for economic policy uncertainty, with highly rated (low economic uncertainty) countries exhibiting higher expected cash flows. Economic theory also suggests that political and economic uncertainty are reflected in discount rates (risk premiums required), with highly rated (low uncertainty) countries having lower discount rates and thus higher valuations. Those lower discount rates lead to lower expected returns: Risk and expected return are positively correlated. The result is that countries with greater political and economic policy uncertainty (riskier countries to invest in) should have higher expected returns.

To test whether theory aligns with empirical evidence, Vito Gala, Giovanni Pagliardi and Stavros Zenios, authors of the study “Global Political Risk and International Stock Returns,” published in the June 2023 issue of the Journal of Empirical Finance, examined whether politics-policy uncertainty predicts variation in stock market returns across countries. They constructed a “P-factor” that recognizes “two distinct, yet interrelated, dimensions of the multifaceted political risk: instability of a government, i.e., electoral risk; and uncertainty about its economic policies, i.e., policy risk.” They integrated these two measures of political risk (politics-policy) into a bivariate risk factor (P-factor). They proxied politics-policy using survey-based measures of political stability and confidence in government economic policy from the Ifo World Economic Survey (WES). The survey provided data on the economic, financial and political climate across 42 countries and covered the period 1992-2016. Politics ratings ranged from 1 to 9 for the most politically stable countries and from 0 to 100 for countries with the highest confidence in government economic policy.

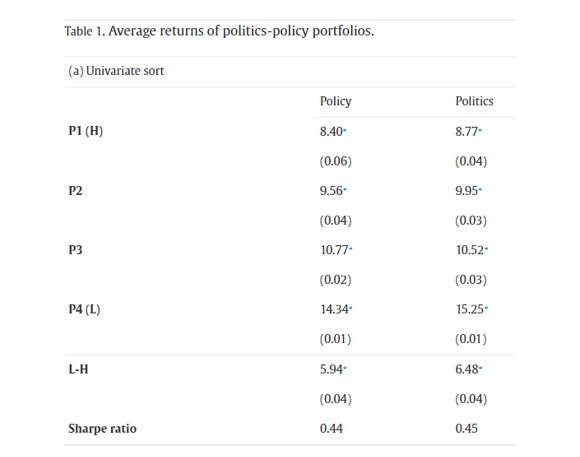

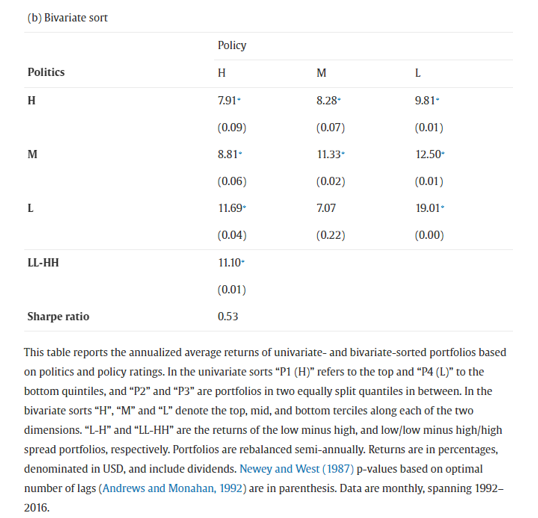

The authors sorted countries first by the less volatile politics and then by the more volatile policy. They then constructed the P-factor as the return of an equally weighted zero-cost tradable portfolio, going long on the countries in the bottom terciles of politics and policy and short on the countries in the top terciles. Portfolios were based on the last day of the month of each WES announcement and were rebalanced semiannually. Here is a summary of their key findings:

Political and policy uncertainty predicted stock market variability across countries—politics-policy ratings forecast economic growth and stock market returns across countries and using both politics-policy measures improved the political risk factor identification. High politics and policy ratings forecast high future cash flow growth. They estimated that an increase in a country’s policy (politics) ratings up to the next quartile would yield on average an increase in future annual GDP growth of 0.52% (0.80%). High politics and policy ratings also forecast low future volatilities.

Forming portfolios of countries sorted on their politics and/or policy ratings produced a monotonic cross section of portfolio returns along both dimensions. The low politics portfolio outperformed the high politics portfolio by a statistically significant 6.48% per annum, and the low policy portfolio outperformed the high policy portfolio by 5.94% per annum, with similar Sharpe ratios.

Global ratings showed considerable time-series variation, and they deteriorated with significant political or economic policy shocks having negative effects, indicating strong spillovers across countries.

The bivariate spread portfolio that was long on low politics-policy and short on high politics-policy (the P-factor) produced a statistically significant average return of 11.10% per annum and a Sharpe ratio of 0.53.

Exposures to global and local risk factors of six prominent asset pricing models could not account for politics-policy predictability—tests showed that differences in returns across politics, policy and politics-policy portfolios were not due to risk premia on existing factors.

Augmenting the global market portfolio with the P-factor significantly reduced pricing errors and improved cross-sectional fit.

Politics-policy uncertainty affected returns through both cash flow and discount rate channels. They showed that political ratings affect the discount rate by demonstrating that they predicted future market volatilities at the six- and 12-month horizons. For the 12-month investment horizon, they estimated that an increase in a country’s policy (politics) ratings up to the next quartile would yield on average a decrease in future annual stock market returns of 1.73% (3.24%).

Correlations of the politics-policy variables with 16 other macroeconomic and financial variables from the WES data are low and insignificant. A political factor on the 16 variables still carried a large and statistically significant premium.

In tests of robustness, the authors confirmed their results using alternative measures of political risk—the International Country Risk Guide (ICRG) country ratings, the Economic Policy Uncertainty Index (EPU) and the World Bank political stability indicators (WB).

Their findings led the authors to conclude: “Political uncertainty around the world, while originating locally, creates common systematic variation across countries leading to priced global political risk. … Asset pricing tests confirm that global political risk is priced.” They added: “We confirm empirically that politics-policy ratings forecast economic growth and stock market returns across countries, and using both politics-policy measures improves the political risk factor identification.”

Investor Takeaways

The economic theory suggests that countries with greater political and economic policy uncertainty (riskier countries to invest in) have higher expected returns (though not guaranteed). It is not surprising that the empirical evidence demonstrates that countries with greater political and economic policy uncertainty have produced higher returns, as risk and expected returns were positively correlated. For investors seeking higher returns, there are no free lunches—they have to accept greater risk. Another important takeaway is that Gala, Pagliardi and Zenios demonstrated that lower political uncertainty increases future expected cash flows (which increase stock prices, increasing realized returns) but reduces future expected returns.

Larry Swedroe has authored or co-authored 18 books on investing. His latest is Your Essential Guide to Sustainable Investing. All opinions expressed are solely his opinions and do not reflect the opinions of Buckingham Strategic Wealth or its affiliates. This information is provided for general information purposes only and should not be construed as financial, tax or legal advice.