Decisive actions by central bankers altered the course of global markets in the third quarter of 2012-at least temporarily.

Overview

Policy interventions overshadowed other factors in global markets during Q3. After investors began the quarter in a defensive stance carried over from Q2, strong actions by the European Central Bank and the US Federal Reserve cast aside-at least temporarily- fears of a Eurozone split and global recession, sparking broad rallies in most major indices. The decisive moves also brought to a halt two of the year's more powerful market trends: The steady decline of the euro and ascent of US Treasuries. As September unfolded, even the most bearish investors began to capitulate to the central bankers as the broad rally gained steam.

However, a series of lackluster economic data releases in late September and the outbreak of anti-austerity protests in Spain and Greece in the final week of the quarter caused a stall in the market rally and raised questions about whether the positive impact of these policy interventions would prove sustainable.

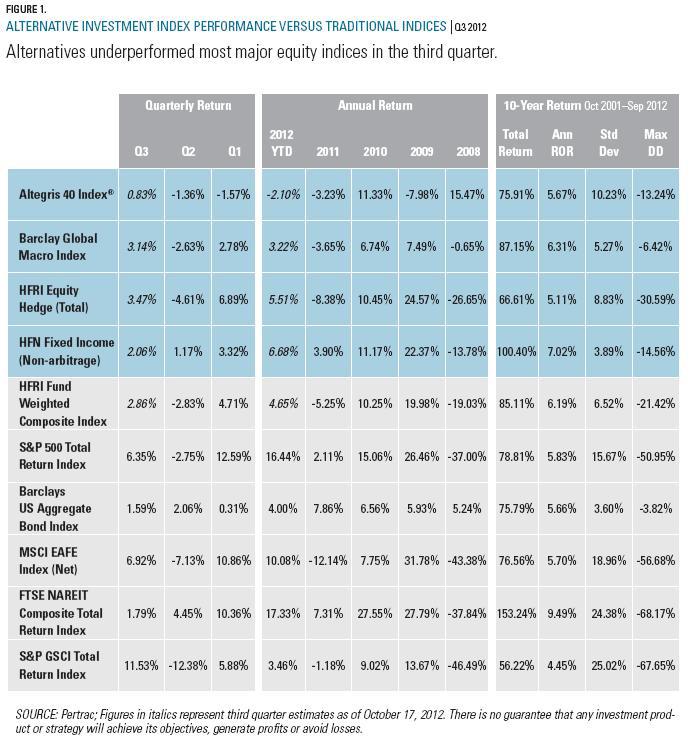

As shown in Figure 1 on the following page, equities (S&P 500 Total Return Index) were up 6.35% in Q3, and bonds (Barclays US Aggregate Bond Index) were up 1.59%. Meanwhile, managed futures (Altegris 40 Index®) were up 0.83% during the quarter, while global macro (Barclay Global Macro Index) was up 3.14%. Long/short equity (HFRI Equity Hedge [Total] Index) was up 3.47% and long/short fixed income (HFN Fixed Income [Non- Arbitrage] Index) was up 2.06%.

A Push from Policy-Makers

Inaction or ineffectiveness on the part of government had been one of the defining features of the year to date. As noted in our Q2 2012 Market Commentary, a "lack of impactful policy responses" had left the market "at the mercy of new recessionary fears." Throughout that quarter, policy-makers' responses to a mounting set of risks were largely limited to words rather than concrete action, and after months of talk, markets were reacting less and less to policy-maker comments. Although European governments did finally take action on the last day of Q2 with a well-received agreement to use European bailout funds to directly recapitalize European banks, the positive effects of that move proved short lived, and markets entered Q3 again gripped by fears of a Eurozone breakup and a possible slide toward global recession.

Those concerns were heightened by a series of negative US economic data releases in early July, led by a discouraging US employment number and a report showing contracting US manufacturing activity. In Europe, yields on sovereign bonds from Spain and Italy continued their climb to dangerous heights. By mid-July, economic prospects had become dire enough to prompt widespread speculation that the US Federal Reserve would be forced into a third round of quantitative easing, and ECB President Mario Draghi was stating in clear terms that Europe would do whatever was necessary to avert disaster.

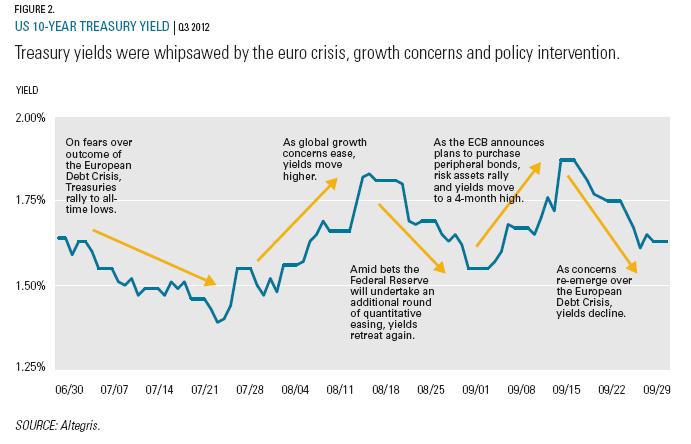

As illustrated in Figure 2 on the following page, markets in August began to move in anticipation of policy action following Fed Chairman Ben Bernanke's statements that in light of a "loss of momentum" in the economy, "additional steps might be necessary."

Meanwhile, Draghi spent the month seeking to overcome widespread aversion to direct action by the central bank and putting in place the details of a new bond buying program aimed at reining in yields on troubled Eurozone sovereigns.

Then, over the course of seven days in September, Bernanke and Draghi shattered the status quo with the announcements of unlimited sovereign bond purchases in Europe as part of "OMT" (Outright Monetary Transactions) and open-ended quantitative easing in the United States under QE3. These strong actions put to rest many investors' fears about a near term tail risk and set off a broad rally in global markets.

However, this sense of certainty faded in subsequent weeks as lackluster data releases capped off by a disheartening report on US manufacturing activity spurred fresh concerns about the global economy, and the European crisis threatened to flare up again with the outbreak of anti-austerity protests in Spain and Greece and new worries about the health of Spanish banks. These developments caused a stall in the market rally and left observers to close the quarter with a question: Now that policy-makers have taken decisive action and promised ongoing support, can economic fundamentals build upon the positive momentum enough to become self-sustaining?

Tail Risk: Tamed, Not Eliminated

Together, the strong central bank interventions were a game-changer for market direction in Q3. By rolling out their heaviest artillery, the central bankers made clear that they would do whatever it takes to stave off economic stagnation or catastrophe. The actions by the European Central Bank and the US Fed sharply reduced tail risk in the short-term, clearing the way for investors to come off the sidelines.

However, even in the midst of the powerful rally in the days following these actions, two points served as reminders that tail risk, although perhaps diminished for the moment, nonetheless remained.

1. Although markets seemed to have temporarily avoided disaster, a positive outcome is by no means assured. Much of the first two quarters of 2012 were dominated by fears of Armageddon in the form of a Eurozone breakup or equity market collapse, and into the second week of September markets were still holding their collective breath awaiting a decision from a German court that could have scuttled the ECB bond-buying plan. Had any one of several variables gone in a slightly different direction, the market could have experienced a severe negative event.

2. We are not out of the woods yet. While the ECB action has calmed the waters in Europe, bond-buying alone cannot address the severe budgetary crises facing Eurozone countries, implement required political and fiscal integration or single-handedly pull Europe back from recession. Meanwhile, across the Atlantic, the Congressional Budget Office warns that a failure on the part of legislators to reach a compromise to avoid the coming "fiscal cliff" could knock four percentage points off 2013 US GDP and trigger a recession.

Because of such risk factors, we continue to believe that the adaptable and opportunistic nature of alternative investment strategies will serve investors well in what remains over the longer term an unpredictable market environment.

Primary Market Effects

In terms of market direction, Q3 was split into four distinct periods defined mainly by the prospects and reality of policy intervention:

Period 1 | First Weeks of July

In the first weeks of July, weak economic data releases from the United States and a lack of significant progress toward resolving the European crisis weighed heavily on global markets. During this period, the cautious and/ or risk-off positioning that many alternative managers carried over from Q2 served them well, and the most successful, defensive trades from earlier this year- long positions in interest rates and short positions in the euro-continued to provide many futures-focused managers with strongly positive returns. Within fixed income markets, continued demand for the excess yield of investment grade and high-yield corporate bonds resulted in strong performance across the corporate credit space during the month.

Period 2 | Late July and August

Late July and August represented a transitory phase, with anticipation of policy action representing the most pervasive theme. Amid a string of signals that decisive government action was on the way, stock markets rallied, helping to boost returns for long-biased equity long/short managers. As details of the ECB bond buying program emerged, the euro trade began to reverse-inflicting losses on many global macro and managed futures managers with sizable short euro positions.

Period 3 | Early September

In early September, announcements that the central banks were bringing out the big guns in the form of QE3 in the United States and unlimited sovereign bond purchases in Europe sparked a rally in global stock markets, a sell-off in long-term US Treasuries and a further strengthening of the euro. The US mortgage backed bond market-the focus of the Fed's QE3 activities-also rallied strongly during the month. In the face of these strong moves, the big risk-off trades of the first half of the year largely gave way as investors saw the folly of betting against the central bankers' actions.

Period 4 | Closing Weeks of the Quarter

In the closing weeks of the quarter, weak economic data releases and anti-austerity protests in Spain called into question the ability of Q3 policy interventions to break the cycle of volatility and uncertainty that has plagued global markets for the past two years.

Against this backdrop, following is a detailed assessment of the managed futures, global macro, equity and fixed income markets.

Managed Futures Strategy Summary

A Shift to Neutral

Managed futures strategies performed well in the month of July but gave back gains throughout the rest of Q3 to end flat for the period, with the Altegris 40 Index closing the quarter 0.83%.

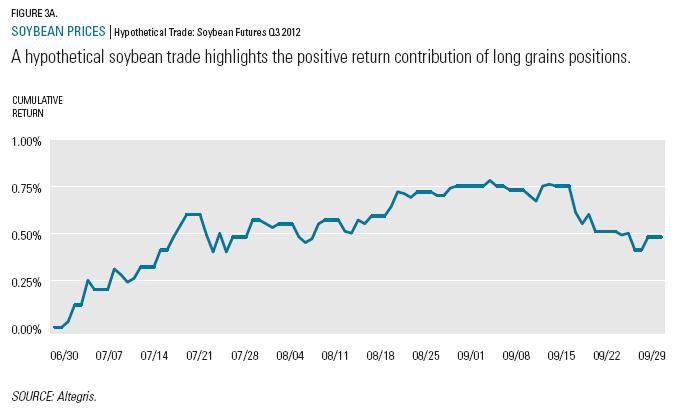

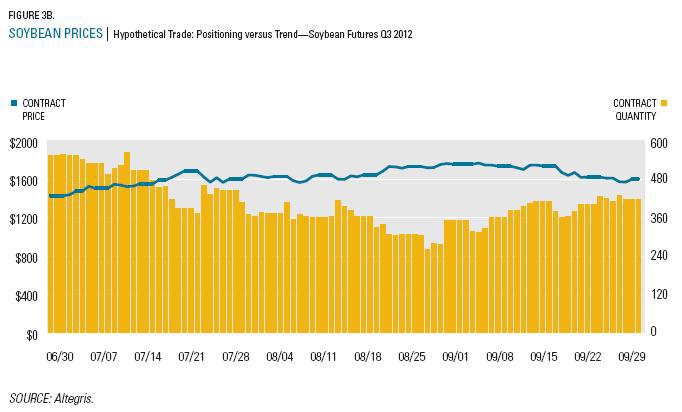

Trend following managers benefited early in the quarter from the continued strength of risk-off positions such as the short euro and long bond trades in place from Q1 and Q2. Long grain positions also produced significant gains early in the quarter, as soybean and corn prices rallied due to a continuation of the drought that took hold earlier in the summer (Figure 3).

Performance among managers following this strategy began to disperse in August as speculation about possible actions by central bankers in the United States and Europe began to influence markets. Subsequent losses were attributable in large part to the reversal of the euro trade in anticipation of and following the ECB's announcement of its bond-buying program in September, as well as the Federal Reserve's announcement of QE3. Managers with quicker-turning models adjusted portfolios faster in response to directional changes in markets and avoided some of these losses, while those with longer term models gave back much of the gains realized earlier in the quarter.

As Q3 drew to a close, managed futures portfolios were markedly changed from the start of the quarter. After entering July in a clear risk-off mode, portfolios had shifted to a more neutral position. In particular, the big defensive trades of the first half-short the euro and long bonds-were reduced over the course of the quarter. Meanwhile, managers increased long positions in stock indices and commodities, and maintained mixed profiles in FX.

Global Macro Strategy Summary

Going "Long Economy"

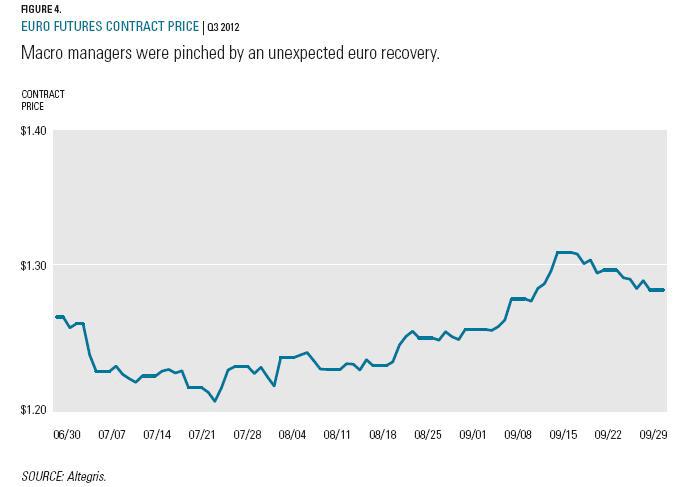

Due in large part to a combination of modestly bullish positioning, emerging fundamental opportunities in commodities and timely anticipation of central bank stimulus, global macro managers performed relatively well in Q3. The one significant exception: Macro managers with FX concentrations generally struggled due to the sharp and unexpected reversal in the euro (Figure 4).

Against a backdrop of broad economic slowdown and concerns that the Eurozone crisis was worsening, macro managers began the quarter profiting from a number of trading opportunities. Bearish bets on the euro and long bond positions continued to pay off. Later in the quarter, managers benefited from bullish stances in commodities as fundamentals came to the fore. In particular, concerns about supply related largely to the imposition of sanctions on Iran provided a strong boost to performance in energy, and a drought in the Midwest of the United States that significantly reduced crop yields and drove prices higher allowed managers who were attuned to the supply/ demand dynamics to profit in grains.

As with trend following managed futures managers, performance among macro managers began to diverge in August due to differing reactions to signals from central bankers that strong intervention was on the way. Managers with an FX concentration performed worse than their more diversified counterparts who generally shifted towards a more bullish positioning in response to speculation of actions by the ECB and the Fed. Across the board, some losses in FX were offset by bullish positions in commodities-particularly in grains-and in stock indices.

By quarter's end, global macro managers had shifted to what would best be described as a "long economy" position. As they did so, however, these managers retained a generally cautious outlook by limiting exposures overall until they get a clearer picture of whether Q3 policy interventions will result in sustained improvement to the global economic outlook.

Equities and Long/Short Strategy Summary

Riding A Rally

By temporarily taking the downside risk of European disintegration and a sharp economic downturn off the table, central bankers cleared the way for a strong rally in global equity markets. The result was a 6.35% gain in the S&P 500 TR Index during the quarter. While returns were strong for most sectors and styles, top performers for the quarter included financials, technology and energy.

Equity markets ended the period on a less than optimistic note, however, with the S&P 500 falling more than 1% in the last week of quarter. Weighing on markets in the final days of September were tepid to negative economic data releases in the United States and Europe, heightened concerns around Spain and Greece, and uncertainty about corporate earnings.

Long/short equity managers entered Q3 with a cautious bent that had been in place since the Q3 2011 systemic scare. As central bankers hinted at more aggressive action in August and sentiment began to improve, managers began to relax this conservative positioning. They began shifting to an even more aggressive stance in September as US policy-makers divulged the details of their bond buying plans.

As a result of this positioning, long/short equity managers participated in the strong Q3 rally in global equity markets, but to a lesser extent than equity market indices. Long/ short equity strategies generally underperform in strong market rallies due to their less than 100% net long exposures. Indeed, the HFRI Equity Hedge Index performance in Q3 vs. the S&P reflects this tendency, finishing up 3.4%-a nearly 3% disadvantage.

In Q3, performance in the strategy was dampened by the defensive stance maintained by many managers in July. The expanded risk profile adopted by managers in August and September resulted in improved levels of relative and absolute performance in the second half of the quarter. Among the strong-performing sectors for long/short equity managers during the quarter: energy, industrials, financials, materials and technology/media/telecom.

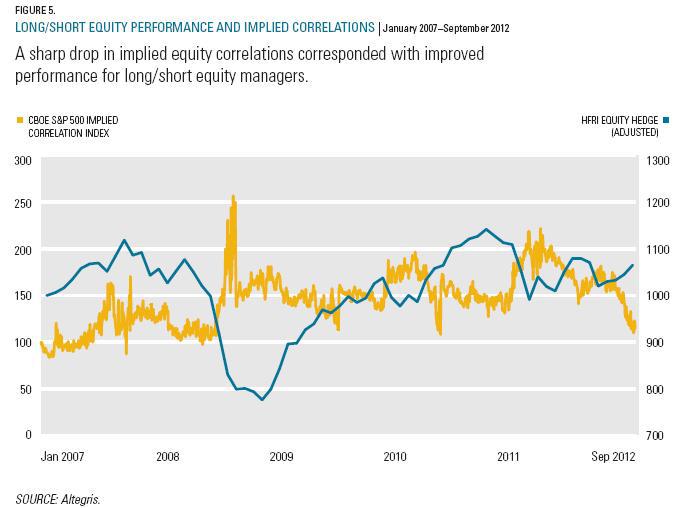

In the recent past, conditions have been challenging for long/short equity managers due to frequent and dramatic swings in market direction. At the end of Q3, however, the market seemed to be experiencing tailwinds, not the least of which were strong corporate balance sheets and funding positions. In addition, decreasing equity correlations over the year and into Q3 translated to an improved stock-picking environment for managers on both the long and short sides (Figure 5).

At the same time, with expected volatility at recent lows, managers have been able to lock in relatively cheap hedges. The end result: Risk was back on in Q3, but managers were employing it carefully and tactically. That approach proved helpful as the broad market rally faltered at the close of the quarter.

Fixed Income Strategy Summary

Back Where It Started

After a series of dramatic swings, the US Treasury market ended the Q3 roughly back where it began, with yields on 10-year Treasuries settling at 1.64% (as shown in Figure 2 on page 4).

The quarter began with a rally that brought 10-year yields to all-time lows. However, that rally lost steam amid speculation of impending action by the Fed and finally gave way to a sharp sell-off in August and September on the announcement of QE3 and renewed growth expectations. Those expectations were in turn shaken in late September when the outbreak of antiausterity protests and rioting in Spain and Greece awoke concerns about a renewed flare-up of the European crisis. These concerns sparked the late September rally that carried Treasury yields back to their starting range for the quarter.

While Treasuries vacillated, corporate credit and highyield bond spreads tightened dramatically over the course of the quarter on continued strong demand from investors seeking excess yields. With 10-year Treasuries yielding less than 2% and the Fed giving investors yet another green light to embrace risk, credit markets were buoyed in Q3. However, outside of mortgage-backed securities, where the Fed is aggressively purchasing bonds as part of QE3, spreads are nowhere near historic lows and, as a result, could potentially tighten further as the economy improves and corporate balance sheets remain strong.

At quarter's close, two risks linger on the horizon, one short-term and one long-term. The most immediate: The so-called "fiscal cliff" in the United States. At present, bond markets appear to be pricing in a positive outcome. However, it is far from a given that politicians in Washington will be able to agree to a compromise. If they cannot, the combination of tax increases and government spending cuts that will take effect at the end of 2012 could reduce US GDP by four percentage points in 2013, according to some estimates, thus triggering a recession. Over the longer term, with the Fed on record with a commitment to provide open-ended stimulus, investors are keeping a wary eye on the looming risk of inflation and rising treasury yields, which poses a meaningful risk to the entire fixed income market.

Conclusion

Central bankers have not eliminated the short-term uncertainty that has gripped global markets throughout this year.

A market that entered the quarter listless in the face of serious concerns of renewed crisis headed into the second half of September fueled by strong policy interventions in both Europe and the United States.

In keeping with the fundamental rule that you can't fight central bankers, investors were abandoning bearish positions that had proven profitable in the first half of the year in favor of increased risk exposures. Indeed, the fact that alternative investment managers were positioned to be successful at different times during the quarter reflected the adaptable nature of these strategies.

However, markets limped into the close of the quarter amid fresh worries about the European situation and lackluster economic data. Looking to the not-so-distant future, investors see the considerable risk associated with the US "fiscal cliff"-a challenge that will have to be addressed amid the complex political environment of a presidential election year.

Counterbalancing that risk is the promise of open-ended monetary stimulus, the effects of which will soon begin to impact market fundamentals. The question for the upcoming quarter and beyond: Which influence will prevail?

Entering Q4, one thing seems certain: Regardless of the long-term effectiveness of Q3 policy interventions, central bankers have not eliminated the short-term uncertainty that has gripped global markets throughout this year. As a result, we remain firm in our conviction that flexible, opportunistic alternative investment strategies that have demonstrated the ability to generate alpha and limit downside risk amid uncertain markets- such as managed futures, global macro, long/short equity and long/short fixed income-can serve as a valuable component of investors' portfolios.

About Risk

Alternative investment strategies that utilize managed futures, global macro, long/short equity and long/short fixed income strategies are subject to risks such as market risk, commodity risk, potential loss due to adverse weather and geological conditions or regulatory and political developments. Other risks include concentration risk, derivatives risk, foreign investment risk, foreign currency risk, emerging market risk, higher expenses, liquidity risk, interest rate risk, credit risk, and significant use of leverage risk which can magnify gains or losses.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: IMPORTANT RISK DISCLOSURE: Hedge funds, commodity pools and other alternative investments involve a high degree of risk and can be illiquid due to restrictions on transfer and lack of a secondary trading market. They can be highly leveraged, speculative and volatile, and an investor could lose all or a substantial amount of an investment. Alternative investments may lack transparency as to share price, valuation and portfolio holdings. Complex tax structures often result in delayed tax reporting. Compared to mutual funds, hedge funds and commodity pools are subject to less regulation and often charge higher fees. Alternative investment managers typically exercise broad investment discretion and may apply similar strategies across multiple investment vehicles, resulting in less diversification. Trading may occur outside the United States which may pose greater risks than trading on US exchanges and in US markets. PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. There are substantial risks and conflicts of interests associated with managed futures and commodities accounts, and you should only invest risk capital. Mutual funds involve risk, including the possible loss of principal.* Altegris and its affiliates are subsidiaries of Genworth Financial, Inc. and are affiliated with Genworth Financial Wealth Management, Inc., and include: (1)Altegris Advisors, LLC, an SEC registered investment adviser, CFTC-registered commodity pool operator, commodity trading advisor, and NFA member; (2) Altegris Investments, Inc., an SEC-registered broker-dealer and FINRA member; (3) Altegris Portfolio Management, Inc. (dba Altegris Funds), a CFTC-registered commodity pool operator, NFA member and SEC-registered investment adviser; and (4) Altegris Clearing Solutions, LLC, a CFTC-registered futures introducing broker and commodity trading advisor and NFA member. The Altegris Companies and their affiliates have a financial interest in the products they sponsor, advise and/or recommend, as applicable. Depending on the investment, the Altegris Companies and their affiliates and employees may receive sales commissions, a portion of management or incentive fees, investment advisory fees, 12b-1 fees or similar payment for distribution, a portion of commodity futures trading commissions, margin interest and other futures-related charges, fee revenue, and/or advisory consulting fees. Genworth Financial, Inc. (NYSE: GNW) is a leading Fortune 500 insurance holding company dedicated to helping people secure their financial lives, families and futures. Genworth has leadership positions in offerings that assist consumers in protecting themselves, investing for the future and planning for retirement— including life insurance, long term care insurance, financial protection coverages, and independent advisor-based wealth management—and mortgage insurance that helps consumers achieve home ownership while assisting lenders in managing their risk and capital. Genworth has approximately 6,400 employees and operates through three divisions: Insurance and Wealth Management, which includes US Life Insurance, Wealth Management, and International Protection segments; Mortgage Insurance, which includes US and International Mortgage Insurance segments; and the Corporate and Runoff division. Its products and services are offered through financial intermediaries, advisors, independent distributors and sales specialists. Genworth Financial, Inc., which traces its roots back to 1871, became a public company in 2004 and is headquartered in Richmond, Virginia. For more information, visit genworth.com. From time to time, Genworth Financial, Inc. releases important information via postings on its corporate website. Accordingly, investors and other interested parties are encouraged to enroll to receive automatic email alerts