Gathering fee-based advisory assets and continuing to leverage referrals to and from Bank of America are what Merrill Lynch says is setting it apart from all other wealth managers.

Andy Sieg, head of Merrill Lynch Wealth Management, told attendees during a presentation on Wednesday at the Barclays Global Financial Services Conference that now is a “great time” to be in the wealth management business, and he believes the industry is “still in the early stages of what will turn out to be a bull market for advice.”

Clients—especially millennials—are increasingly looking to wealth managers to deliver holistic advice on their entire financial life and the combination of Merrill Lynch and Bank of America create a suite of services to which “frankly, our competitors simply don’t have access,” Sieg said.

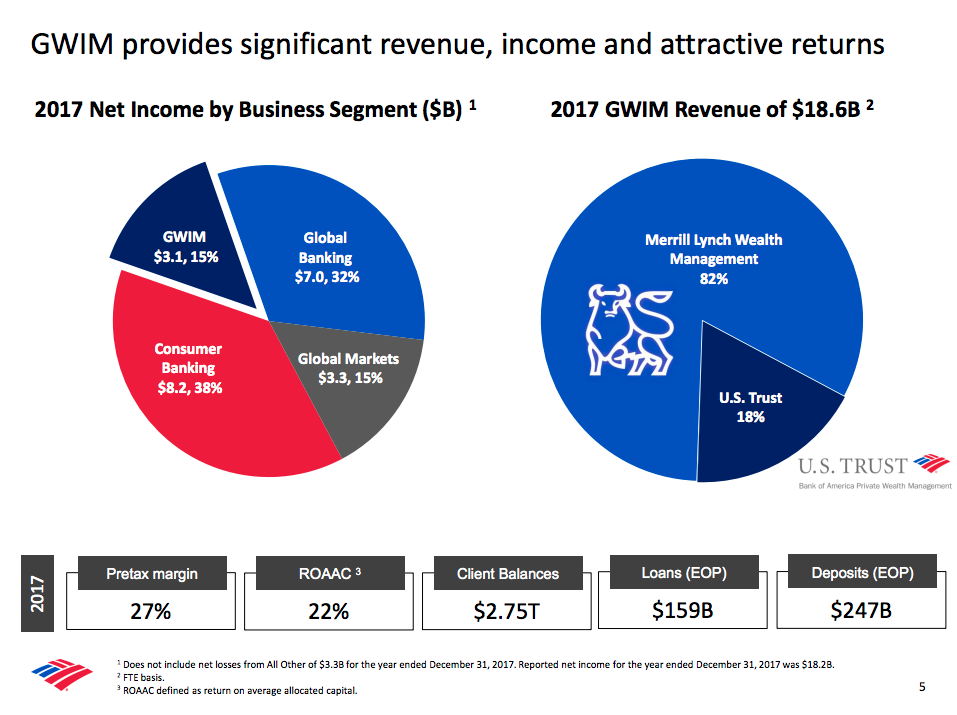

Market performance over the last 18 months has pushed profits at wealth management businesses to record highs, as client assets increasingly transition to more lucrative fee-based advisory accounts, driving up revenue. Over the past 9 years, total revenue of Bank of America’s Global Wealth and Investment Management division, which includes Merrill Lynch and U.S. Trust, grew from $14.9 billion to $18.6 billion as the percent of revenue from asset management fees and net interest income improved from 71 percent to 85 percent.

In 2017, the segment accounted for $3.1 billion or 15 percent of the bank’s income. If Merrill Lynch were an independent company today, it would be the eight largest bank in the United States, in terms of client assets, with more than $2.8 trillion.

For comparison, Bank of America’s consumer banking segment brought in $8.2 billion or 38 percent last year.

Merrill Lynch is also highly profitable and, despite some industry headwinds, is getting more efficient. Sieg said the GWIM segment had a pretax margin of 27 percent in 2017 but had already improved to 28 percent this year.

The wealth manager recently faced criticism for reversing course and once again allowing commission-based brokerage activity in client retirement accounts. But if Sieg’s presentation is any indication, the future of Merrill is in untapped opportunities through Bank of America and its growing advisory business.

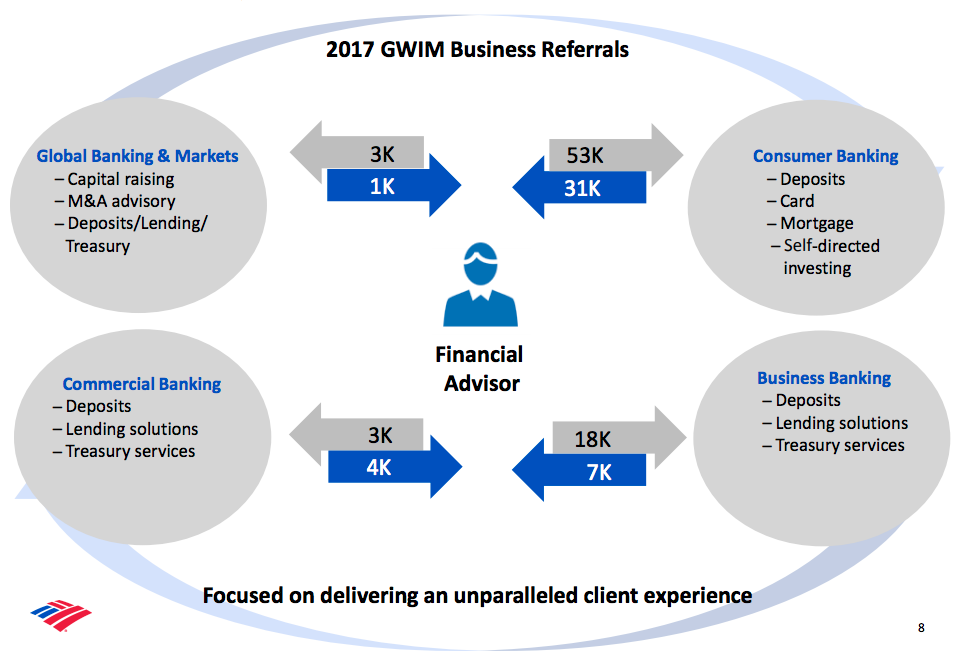

Last year, Bank of America’s four other segments sent more than 44,000 business referrals to the wealth management segment. Meanwhile, GWIM sent more than 77,000 to the other segments. Roughly half of all referrals coming and going from GWIM were with the consumer banking segment, creating a model “unique and very powerful” in wealth management, Sieg said.

“This is not a transactional business,” Sieg said—an eyebrow-raising declaration from the head of the largest brokerages. But he said the change has insulated the business from shifts in the industry.

Wealth managers continue to face pricing pressure that Merrill Lynch does not expect will abate anytime soon, Sieg said, but the need for more cost-effective investments and investing passively shouldn’t hinder the firm’s fee-based revenue.

“Even if it’s two or three basis points per year, and not four, the pressure is out there and, for us, that is all the more reason to accelerate the focus on asset gathering, and build a larger asset base, as well as broaden the banking activities that are happening with our client base so that we have as diversified a source of revenue streams as possible.”