The recent failure of Silicon Valley Bank raised investor concerns about systemic risks to the banking system because many regional banks have similar problems of mismatched duration risk and large percentages of uninsured deposits. It was also a reminder that even the actions taken during the 2008 global financial crisis did not forever resolve banking crises.

While each financial crisis is different to some degree, what can investors learn from examining the history of financial crises and their impacts on the economy and both equity and bond markets? Are there patterns that can be observed? To learn what lessons history can provide, Carola Frydman and Chenzi Xu, authors of the January 2023 study Banking Crises in Historical Perspective, surveyed the literature on historical banking crises, defined as events that took place before 1980. With their focus on empirical work published in 24 leading general interest and field journals between 2000 and 2022, they reviewed 218 papers that covered the 1800-1980 period (there are few articles on crises prior to 1800, and no crisis in the last 40 years is considered historical). Here is a summary of their key findings:

There are common underlying economic forces that lead to costly crises, such as liquidity mismatch and deterioration in intermediation; the instruments and institutions that introduce risk in the system evolve and often outpace regulation. Financial crises are associated with worse declines in output and consumption than other types of crises on average—they have large negative effects on the real economy, affecting a wide range of outcomes, from employment and output to political participation, and the effects tend to be large and long-lasting. Widespread corporate default crises, on the other hand, do not appear to have the same large negative real effects as banking crises.

Financial institutions with higher leverage are more likely to experience turmoil. Leverage in the financial system is a systematic precursor to crises, playing a significant role in exacerbating downturns. Financial systems tend to become more and more speculative, with increasing amounts of debt financing used to fund investments, leading to the creation of financial bubbles.

The accumulation of debt can be particularly pernicious because it can create a positive feedback loop in which the increased value of assets leads to even more borrowing and speculation, which in turn drives an even greater increase in asset values. This creates a sense of false security and encourages further risk-taking, ultimately leading to an unsustainable level of leverage. When market conditions change, such as a rise in interest rates or a fall in asset prices, it creates a sudden demand for debt repayment and leads to a sudden decrease in the values, leading to financial instability and economic crisis. This in turn can trigger a downward spiral of asset sales and fire sales, causing a crash in the asset prices and a broader economic crisis—a “Minsky moment”.

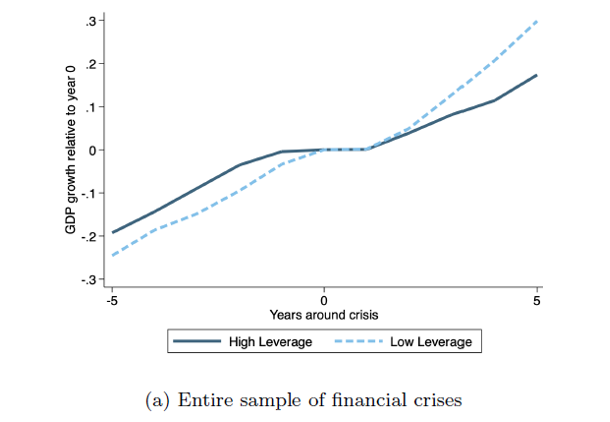

Countries that entered a recession with low leverage experienced stagnation in GDP growth for about a year, but that growth resumed quickly and continued on trend. However, within the set of high-leverage crises, GDP stagnated for about two years and did not recover the losses relative to the trend in the five years that followed.

Relative to standard recessions, those that follow a financial crisis are more likely to be preceded by credit growth to households and to the nonfinancial sector in the five years leading up to the event. In the five years following a high-leverage event, there was a 36% probability of a financial crisis relative to only a 22% probability following a low-leverage event (t-stat = -1.64)—there were 27 events in the high-leverage group and only 17 in the low-leverage bucket. Low-leveraged countries’ GDP growth was 6.4 times higher than high-leveraged countries five years after the crisis. Unusually high credit growth was correlated with unusually low credit spreads, where widening spreads presaged crises, at least among advanced economies since the 1870s.

Living through a banking crisis may affect economic outcomes over the long run by shaping the risk preferences of a generation.

In addition to leverage, another source of bank fragility is the maturity mismatch between its on-demand liabilities and longer-term assets, where self-fulfilling runs can lead to insolvency even when assets are safe. Once a few depositors perceive a bank to be in trouble, they share their views with others, who also act on it. This type of behavior is also evidenced in modern settings where deposit insurance is present (the SVB episode demonstrated that social media and the ability to move funds with a “click” has increased the risk of bank runs unless there is government intervention).

Banks are usually interlinked—an adverse event on less robust institutions transmits domestically and internationally to others, amplifying the crisis. Bank contagion may also arise in contexts where interbank deposits are an important source of funding, leading to chains of intermediation. Shocks to domestic banking systems often transmit internationally through banks’ investment in foreign assets. International banks may also contribute to spreading crises globally because their funding can be directly exposed to one market while their investment activity is elsewhere—as was the case in 2008.

For emerging markets, capital inflows can import financial crises and can also be coupled with sovereign debt crises. However, while open capital flows may lead to contagion, they can also aid in recovery.

Early and widespread government intervention (such as aggressively expanding money supply, injecting liquidity broadly and providing fiscal stimulus) is an important tool to arrest panics, limit the contraction of the banking sector, and ameliorate the impact on the economy. Historical crises that have not benefited from intervention have been particularly costly. The amount of public sector debt impacts the degree to which the private sector can deleverage and the fiscal capacity for states to intervene directly.

Summary

The research into financial crises has uncovered three major common threads: Leverage in the financial system is a systematic precursor to crises; crises have large negative effects on the real economy; and government interventions through easy monetary policy (lowering interest rates and quantitative easing) can ameliorate these costs.

Let’s look at how these threads apply to the recent crisis. SVB’s failure led to a general tightening of financial conditions, increasing the downside risk to the economy because the regional banks impacted are large lenders to smaller businesses and the commercial real estate and industrial loan markets. Banks smaller than the largest 25 account for around 38% of all outstanding loans and 67% of commercial real estate lending.

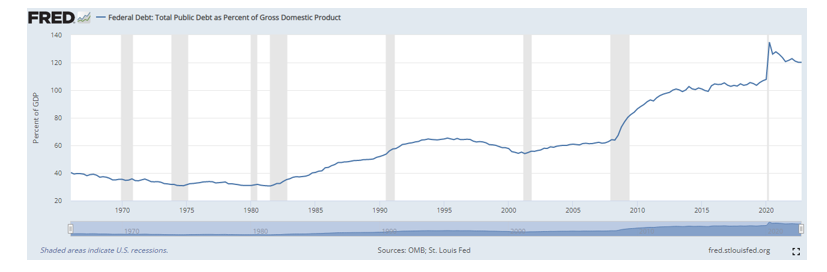

While the Fed is providing the market with all the liquidity it needs, and effectively guaranteeing all deposits (at least in the short term), it is constrained from lowering interest rates as it continues to focus on inflation that remains well above its 2% target. At the same time, fiscal policy is constrained by already large budget deficits and a split Congress. The Congressional Budget Office projects a federal budget deficit of $1.4 trillion for 2023, with the deficits rising in future years. For example, the debt will swell to 6.1% of GDP in 2024 and 2025 and will reach 6.9% by 2033. In addition, the debt-to-GDP ratio is now well above 100%.

These constraints seem to increase the risks of a recession with longer-lasting effects.

Larry Swedroe has authored or co-authored 18 books on investing. His latest is Your Essential Guide to Sustainable Investing. All opinions expressed are solely his opinions and do not reflect the opinions of Buckingham Strategic Wealth or its affiliates. This information is provided for general information purposes only and should not be construed as financial, tax or legal advice.