“Investors Are Finally Warming Up to Bond ETFs,” so reads a story in the Wall Street Journal’s Funds & ETFs section.

While equity ETFs have gained hugely in popularity, bond ETFs have lagged, but according to the story, that’s changing. A report by Blackrock from October says that bond ETFs have grown 25 percent each year for five years and are expected to hit $1.5 trillion in 2022, nearly double the current level.

It makes sense. The popularity of equity ETFs was a teaser for bonds to follow. In the case of bonds, the enhanced liquidity vs. individual bonds is apparent (if potentially problematic in a rout, especially as you move away from the liquidity of Treasurys). Also, there’s been an increase in tailored sorts of funds beyond broad ones like the AGG, the article points out.

There are implications for bond fund managers, of course, but there are other implications from a broader market perspective that I’ve touched on before, which seems that much more relevant in light of the article’s findings.

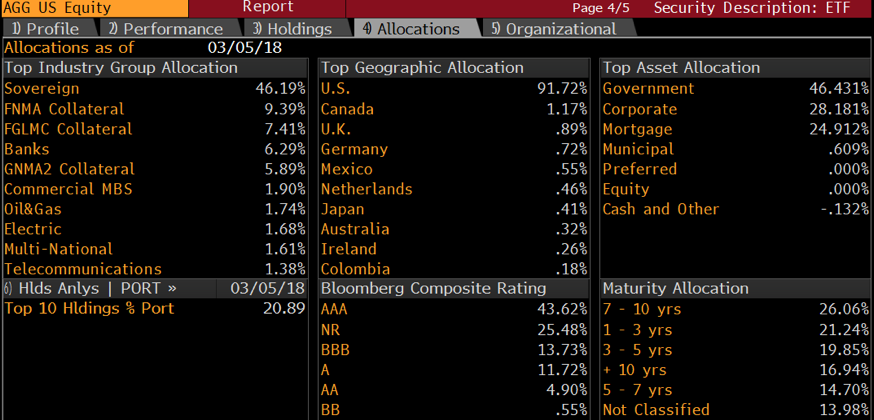

First, the big story is of passive management vs. active management. What this means is more money following a given index, such as the AGG which tracks Bloomberg Barclays US Aggregate Bond Index. The latter has an allocation of 46.4 percent in governments. Given what’s happening with the deficit that weighting is bound to increase, and how. Also, if you’re in my camp, you believe the duration of the index will increase with the addition of more 10s, 30s and, possibly, 40-year bonds or more. Then there’s the Fed’s balance sheet reduction “returning” the securities they would have bought to the market’s float. Then there’s the idea that in a higher rate environment, mortgage prepays slow.

What you’re left with is a sharply increasing amount of Treasurys in a given index and more duration to boot. Passive investors will have to follow those changes. As a result, the passive’s needs over time will provide a forced need to buy Treasurys with duration, which may soothe a generic rise in rates. It’s not bullish per se, but it does underscore one source of buying.

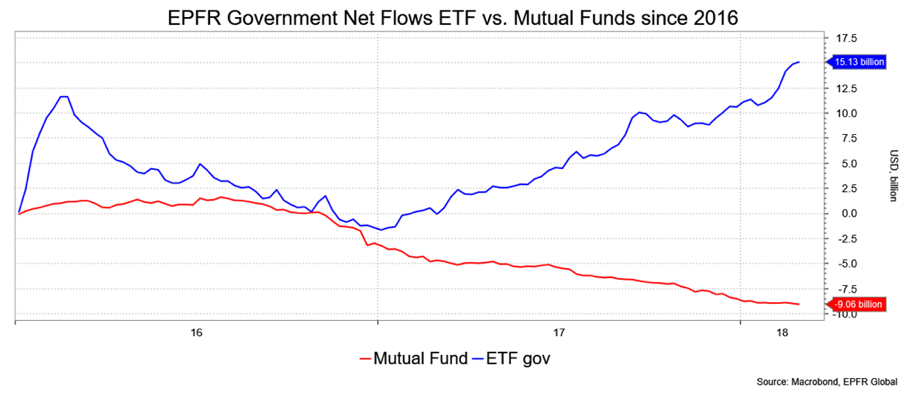

Here’s where EPFR flows add to the narrative. First, there’s confirmation that flows into U.S. Government ETFs have greatly outperformed mutual funds. If I did this correctly, since 2016 the cumulative net flow into ETFs is $15 billion vs. a $9 billion outflow from government mutual funds.

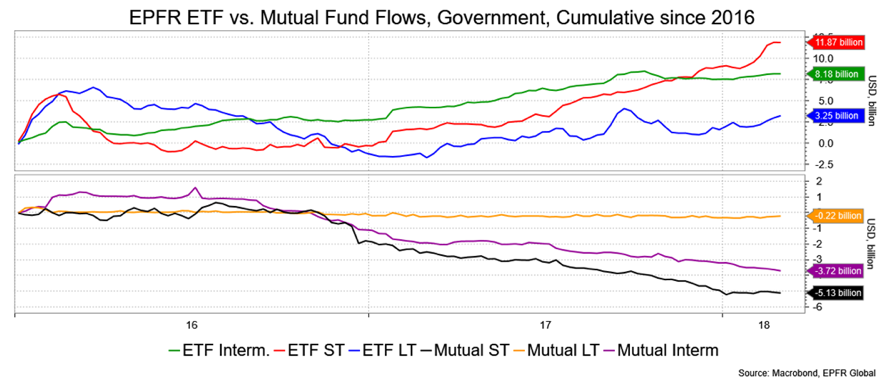

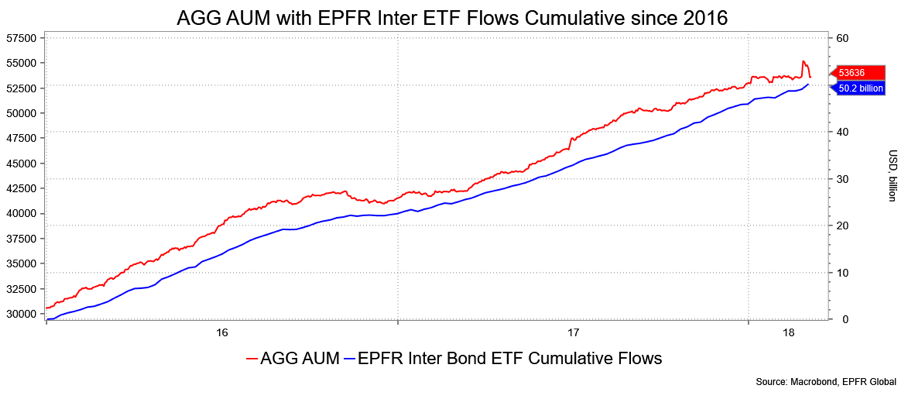

When looking at maturity buckets, the striking image is of flows into short-term government bonds. Here you have seen $12 billion going into short-term government ETFs—a paean to rising short-end rates no doubt— vs. a $5 billion mutual fund outflow. For what it’s worth, the category that’s seen the single biggest inflow is the ETF intermediate one, not just governments, with $50 billion coming against nearly $4 billion flowing out of intermediate-term mutual funds. Intermediate ETFs would include the AGG. For example, the AGG has about $53.6 billion assets under management today vs. $30.5 billion at the start of 2016.

David Ader is Chief Macro Strategist for Informa Financial Intelligence. Read more of Ader’s Musings here.