There’s been no shortage of speculation about the impact of the Tax Cuts and Jobs Act of 2017 (TCJA) on the U.S. economy. Some would argue the extensive changes in federal income tax laws brought forward by that legislation have been a much needed elixir that’s stimulated the economy and raised all boats. Others point to indications that the bulk of the tax cuts went to higher income individuals and have only served to increase deficits and national debt while accelerating the rate of concentration of wealth in the United States.

The effect of the TCJA on charitable giving by individuals in the United States also has been a topic of conjecture since the bill was enacted. Predictions of gloom and doom because of increased standard deductions and lower effective tax rates driving up the after-tax cost of giving were countered by supply side arguments that economic growth and more disposable income would naturally spur increases in philanthropic activity.

Fortunately for nonprofits and those who advise philanthropically inclined individuals, we’re now beginning to learn more about the actual impact of tax reform on giving, thanks to hard data recently released by the Internal Revenue Service. Each year, the IRS engages in “rolling disclosure” as it publishes periodic data summarizing the number of tax returns that have been filed by a particular date.

These reports include details regarding the amount of income and deductions reported by adjusted gross income (AGI) range. The IRS released data in July that reflects the content of returns for the 2018 tax year that had been filed by July 25, 2019.

As of the same initial 30-week filing period in 2018 for the 2017 tax year, some 92% of all returns eventually completed for the 2017 year had been filed. Only in the highest income ranges in which 6-month extensions are more common did the percentages of returns filed in the first 30 weeks of the year dip, with only 48% of returns eventually reporting AGI of $1 million or more having been filed at that juncture in 2017.1

The recent data by no means tells the entire story of tax reform and charitable giving, but it certainly affords a glimpse of what will undoubtedly be a changing landscape for philanthropic planning in coming years.

Fewer Itemizers a Reality

One of the primary concerns among nonprofits and those who analyze trends in philanthropy was that doubling the standard deduction and capping state and local tax deductions and certain other deductible items would greatly reduce the number of donors who would be able to deduct the amount of their charitable gifts and be forced to make their gifts from after-tax dollars.

Applying the concept of price elasticity of demand, some predicted that the impact of widespread non-deductibility of charitable gifts would result in a decline in giving due to increased after-tax cost.

For example, an individual who makes a tax-deductible gift of $10,000 must only earn $10,000 to make that gift because the income used to make the gift isn’t taxed. The “cost” of the gift in terms of income required to make it is therefore $10,000. On the other hand, if the amount of that gift isn’t excluded from taxable income, an individual in a 37% marginal tax bracket must earn $15,873 before imposition of tax to make the same $10,000 gift.

That amounts to a 58.7% increase in the amount of income required to keep gift levels even. It was predicted this increase in cost in terms of income required to make a gift would lead to a reduction in giving to some extent depending on the price elasticity of demand for gifts to a particular charity.

So, what do the estimated 92% of 2018 tax returns that have been filed thus far tell us about the number of people who are continuing to itemize tax deductions in general, and charitable deductions in particular, and changes in how much they’re giving on average?

Assessing the Impact

Based on the number of itemizers for the 2018 federal income tax reported on so far, the percentage of taxpayers who itemize deductions of any type has, as predicted, dropped dramatically from 30% to 10%.2

The number of those claiming charitable deductions on their tax returns has dropped from 24% to 9%. The amount of gifts itemized declined dramatically from $160 billion to $102 billion, a decrease of 36%.3

As a result of this new reality, the phrase “your tax-deductible contribution” now applies to just 13.5 million households out of an adult population of roughly 250 million.

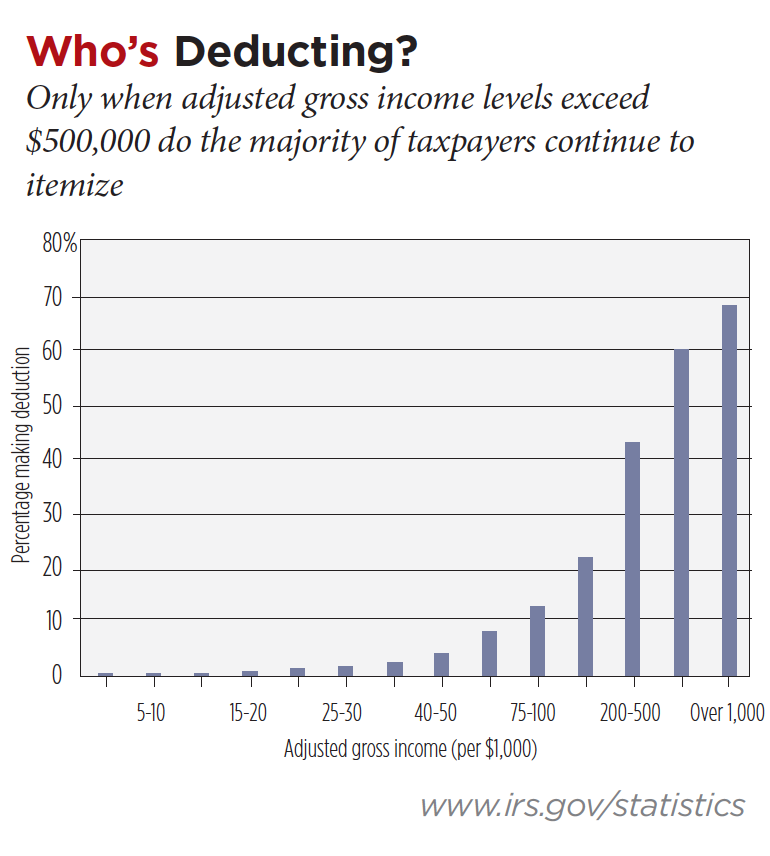

“Who’s Deducting?” p. 10, shows how those who experienced income tax savings as a result of their charitable gifts reported so far for 2018 returns were distributed based on the amount of their AGI.

Note that deductibility of charitable gifts increases dramatically with the amount of a donor’s AGI. Only when AGI levels exceed $500,000 do the majority of taxpayers continue to itemize their charitable deductions.

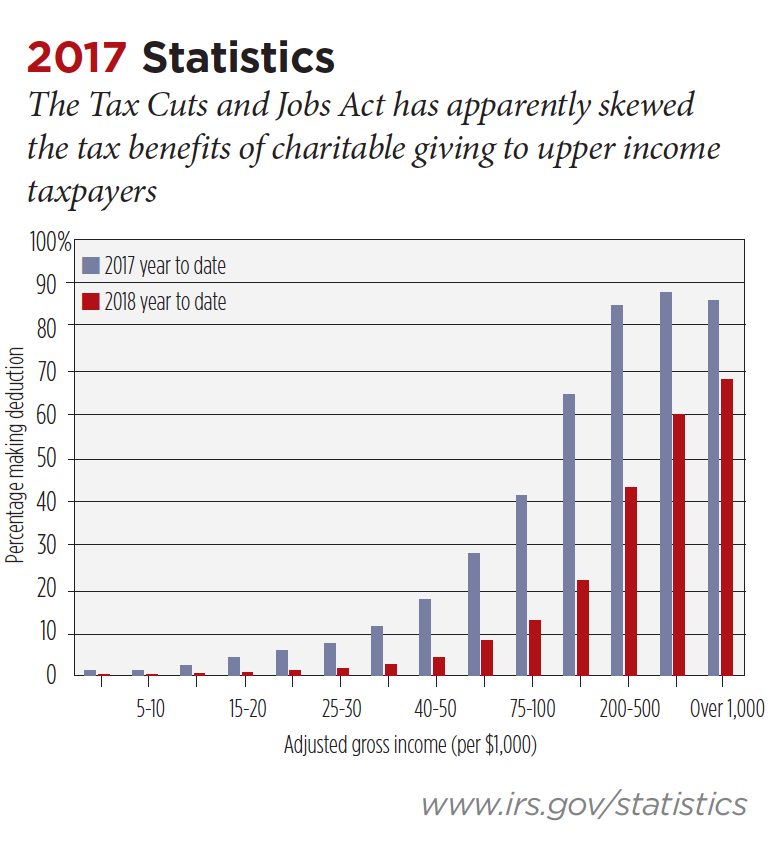

A comparison of the same statistics for 2017 dramatically illustrates how the TCJA has apparently skewed the tax benefits of charitable giving to upper income taxpayers. See “2017 Statistics,” this page.

Before the enactment of the TCJA, the majority of taxpayers with income of $100,000 or more were able to deduct their charitable gifts, and that number approached 90% when incomes topped $200,000.4

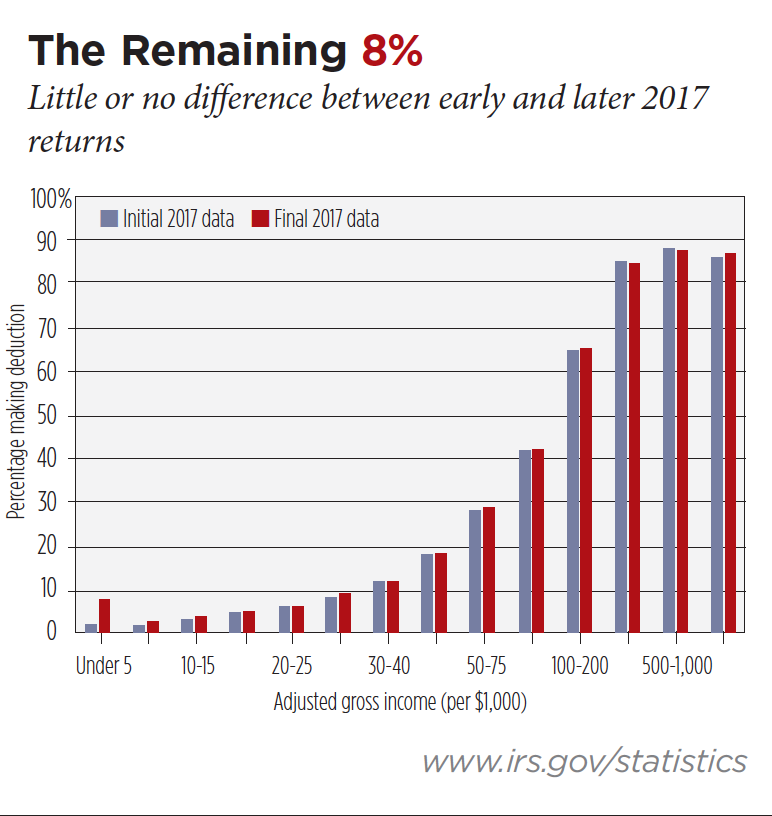

One might naturally wonder whether the remaining 8% of yet unfiled returns might significantly change these statistics, if at all. A comparison of the 92% of 2017 returns filed by the end of July with the data released after the filing year for 2017 was completed shows little or no difference between the percentages of those taking charitable deductions in the early filed returns versus the total number eventually filed. See “The Remaining 8%,” p. 12.5

The principal takeaway based on early indications is that tax planning aspects of charitable giving are now primarily the concern of higher income taxpayers and those who advise them.

Increased Size of Gifts

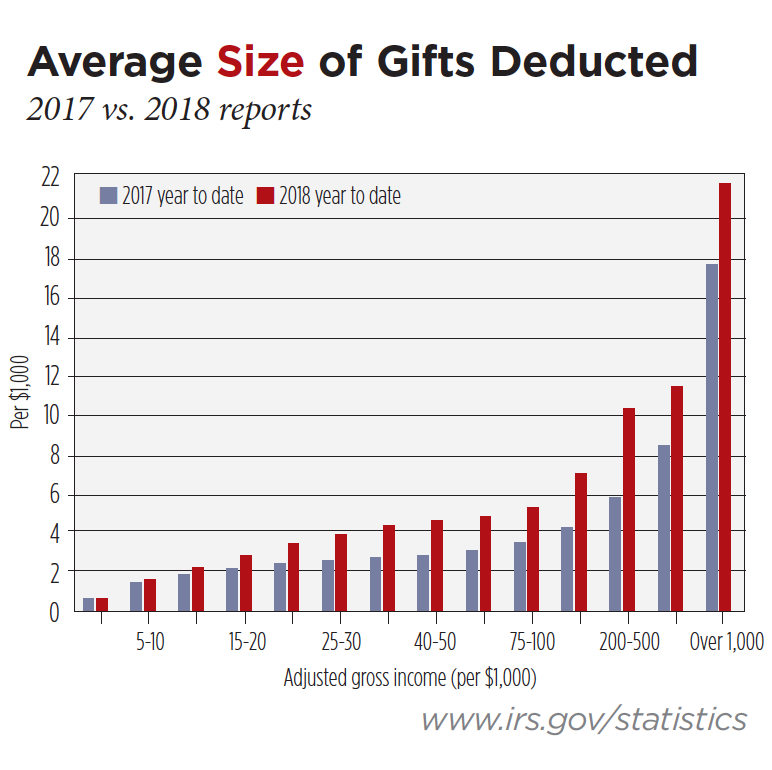

Insofar as the average size of gifts that are still being deducted is concerned, the early reports indicate that the amount of these gifts is increasing. “Average Size of Gifts Deducted,” p. 12, compares the average size gift deducted according to early 2018 gift reports with the average size gift deducted at the comparable reporting stage in 2017.6

Interestingly, those who continued to itemize gifts increased the average amount of those gifts in every AGI category. The $1 million-and-up AGI category is excluded from this chart as the majority of returns in that category won’t be filed until after the Oct. 15 extension date.

A few explanations for the increase in average gift size initially come to mind. First, many of those who continue to itemize are able to do so because of relatively higher levels of donative intent that drive them to give more than average in the first place.

Another possible explanation is that a number of taxpayers may have bunched their deductions in part by making larger gifts in 2018, and they won’t be expected to repeat those gifts in 2019.

This bunching may have been accomplished by making larger than normal gifts directly to one or more charities or through larger gifts to donor-advised funds (DAFs). The latter possibility was certainly supported by the unprecedented amount of contributions to DAFs in 2018.

In the case of larger DAF gifts, charities may not feel the impact of bunching, as the point of this strategy was to “level” giving over one or more years. On the other hand, charities that were the beneficiaries of more “direct” bunching in 2018 may find more bare cupboards in 2019. Again, time will tell when we begin to discern and learn from patterns of deductions for 2019 and beyond.

Tax Policy Implications

From a tax policy standpoint, we’re certain to see an increase in the number and volume of debates regarding charitable giving. The battle lines are now being drawn for the next round of tax reform, and many anticipate we’ll see this continue in the wake of next year’s elections. The recent IRS data will be mined for arguments for and against expansion or restriction of future tax benefits related to charitable gifts.

On one side, there are those who would justify continuation of greater tax benefits for higher income individuals who make larger gifts by arguing these individuals who voluntarily shoulder a greater burden by investing more of their income in societal needs shouldn’t also have to pay tax on those dollars before making their donations.

Others will argue that an individual who gives 1% of a $100,000 income, or $1,000, should enjoy the same tax subsidy as someone who gives 10% of a $1 million income, or $100,000. Under that argument, the individual who gives more also experiences the same relative loss of income if his deduction is allowed but experiences much more cost in terms of increased income required to make his gifts if the charitable tax deduction is actually or effectively eliminated—as it was for many taxpayers by the TCJA.

One of the most widely promoted solutions to this conundrum is to allow all taxpayers to exclude charitable gifts from their AGI above the line and thus require that no taxpayers make gifts from after-tax dollars. Various legislative proposals to accomplish this result are already in front of Congress.

In the Meantime

Regardless of how future tax policy shakes out, what are the takeaways for planners from what we’ve learned so far about the impact of the TCJA on charitable giving?

First, when advising a client on charitable giving tax planning strategies, it’s important to determine at the outset of discussions whether that client can still benefit from the tax savings possibilities that result from giving.

In the past, an advisor to high-net-worth clients could assume nearly all were itemizers, and it wasn’t necessary to spend time exploring that issue in any real depth. But, as the numbers reported above reveal, there may now be as many as 30% of even the highest income individuals who no longer itemize tax deductions due to a number of circumstances, and proposals predicated on income tax savings may increasingly fall on deaf ears.

Second, be attuned to helping those who no longer itemize deductions restore their ability to actually deduct charitable gifts once more or achieve the same results by other means.

The most straightforward means of helping donors regain their itemizer status, at least in some years, is through the bunching of gifts and certain other deductions as described above.

Another possibility is to make a gift that exceeds their standard deduction for the year of the gift and is of a magnitude that carryforward provisions will provide enough in the way of charitable deductions in up to five future years to assure itemizer status.

It’s also possible to help clients achieve the same result as reporting income and fully deducting it by avoiding inclusion of amounts directed to charity in the first place.

Examples of this strategy include taking advantage of the ability for those older than age 70½ to give up to $100,000 directly from an individual retirement account to charity without reporting the amount donated in this manner. This is an example of how Congress has, in effect, allowed an above-the-line deduction for older donors who have more funds in their IRAs than they need for living expenses to divert a portion of these accounts to charitable use on a tax-free basis.

Other examples include carving out an irrevocable annual gift amount for direct charitable use from retained charitable remainder trust (CRT) income without the client reporting and deducting the income.

Charitable lead trusts may also be established as a way to direct income to charity on a tax-free basis for a period of time when it’s no longer possible for the donor to itemize the donated amounts. This may be a solution for higher income individuals who no longer itemize their deductions or are chronically restricted by AGI limits on the amount they can deduct.

Finally, the recently reported itemizing statistics may also underscore the fact that cash may no longer be king when it comes to charitable giving.

Keep in mind that when appreciated securities, real estate or other property is donated to charity, there’s no capital gains realized, and the full value of the property can be deducted and devoted to charitable purposes. The donor also must not pay tax on income equal to the value of the property being donated. While this may be obvious to many financial advisors, don’t assume donors/clients understand this reality.

For example, assume a 68-year-old couple with total income of $350,000 and an AGI of $300,000 would like to make a gift of $15,000 to a building campaign. Their home is paid for, and their state and local taxes are capped at $10,000.

They’re not happy to learn that they can no longer itemize this $15,000 charitable gift because their total deductions don’t exceed their standard deduction of $26,000. This means that in their 32% tax bracket, it will require $22,058 in pre-tax income to net the $15,000 they wish to give.

Their financial advisor recommends that they instead donate $15,000 worth of stock for which they paid $7,500 several years ago. If they sold the stock, they would owe capital gains tax of $1,125, and their net proceeds wouldn’t be sufficient to fulfill their $15,000 pledge.

If they instead gave the stock to the charity, they still wouldn’t be able to benefit from a tax deduction, but they wouldn’t owe any capital gains tax on the value of the donated stock and don’t have to earn 47% more than the amount of the gift that would be the case if they gave cash.

Finally, their spendable income isn’t affected by the amount of the gift, and they could use the cash they didn’t donate to repurchase the same stock if desired and enjoy a new, higher cost basis.

The best advice for many clients may be, “If you have any stock or other appropriate asset that has increased in value since you owned it, it may be smarter from a tax planning perspective to give that asset and preserve your after-tax cash for other purposes.”

Interplay With Estate Tax Changes

The TCJA also made dramatic changes in federal estate and gift tax laws. In a move that mirrored somewhat the doubling of the standard deduction, Congress also doubled the amount that’s exempt from federal tax gifts of assets during lifetime or at death.

As a result, only an estimated one-tenth of 1% of Americans will be subject to these taxes at the federal level. This means very few of the estates of millions of Americans who now plan to leave a portion of their estates for charitable purposes will see any tax savings as a result of their generosity.

It may make sense for those of advanced years who are no longer itemizing their charitable gifts to “accelerate” all or a portion of planned estate gifts by making those gifts during their lifetime. For example, a $100,000 gift shifted to annual gifts sufficient to meet or exceed one’s standard deduction could make it possible to then deduct the amount of the gift and possibly other expenses and, in effect, experience an income tax deduction for the “bequest.”

Higher wealth individuals may wish to expand on this concept by using appreciated, low yielding assets to fund a CRT or other life income gift and, in so doing, bypass capital gains tax, increase their income and generate a large income tax deduction that could boost them into itemizer status for the year of the gift and possibly one or more future years and help shelter their increased income from the trust from additional taxes for a period of time.

Stay Tuned

Stay tuned for further updates from the IRS on how 2018 tax return data shakes out after the remaining 8% of mostly high income taxpayers’ returns are filed. Few surprises should be forthcoming.

Suffice it to say that from this point on, charitable income and estate planning will depend on the interplay of many more factors than in the past and require greater attention to the what, when and how of completing charitable gifts that may be motivated by charitable intent and maximized by prudent planning.

Endnotes

1. “Filing Season Statistics, Mid-July Filing Statistics by AGI,” 2019, www.irs.gov/statistics.

2. “Filing Season Statistics, Mid-July Filing Statistics by AGI,” 2018, www.irs.gov/statistics.

3. Ibid.; compare with note 1.

4. Ibid.

5. Ibid.

6. “IRS Tax Statistics of Income Final Report for 2017 Tax Year,” www.irs.gov/statistics.