Quick. Who was your first customer? If you’re like many in the financial services industry, it was likely someone in or close to your family.

“Work your warm market” is the mantra for newly minted financial advisors. And what market is warmer than family? They are the most accessible and usually have an interest in supporting your success. They may feel that, as family, you will be more trustworthy and treat their investments with a heightened sense of care and protection. Or maybe they just didn’t know how to say no to you.

And therein lie two problems with having kin as customers. While soliciting family members and getting their referrals is a proven way for new advisors to get their foot in the door, the practice is fraught with peril. They may resent being solicited. Even if they say yes, they can be difficult to manage and create considerable difficulties for advisors, both professionally and personally.

That said, Peter Blatt, founder of Blatt Financial Group and Blatt Legal, both in Palm Beach Gardens, Fla., believes that with safeguards in place, it can work for the benefit of all. “Family member clients are a double-edged sword,” Blatt acknowledges. “They can be your best cheerleaders and steer a lot of referrals your way, but unless you have firm rules in place and stick to them, doing business with family members will create real difficulties.”

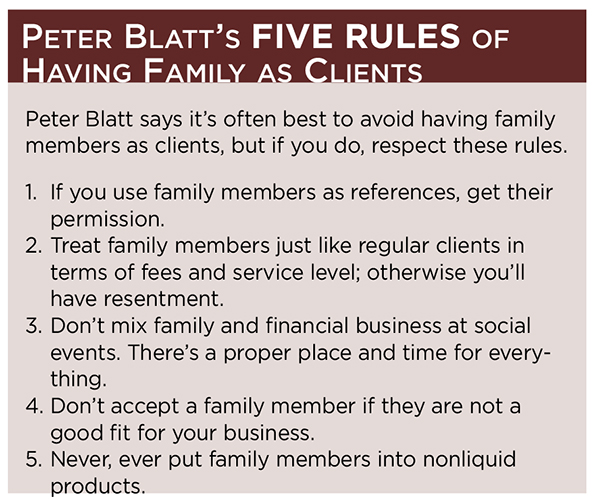

Blatt started managing his parents’ portfolio after a retail broker lost 40 percent of his father’s portfolio. When his father, a retired New York City businessman, and mother divorced in 2008, Blatt continued managing his mother’s money. To make these relationships work both professionally and personally, Blatt evolved five rules for managing family members who are clients.

Treat Them Exactly The Same

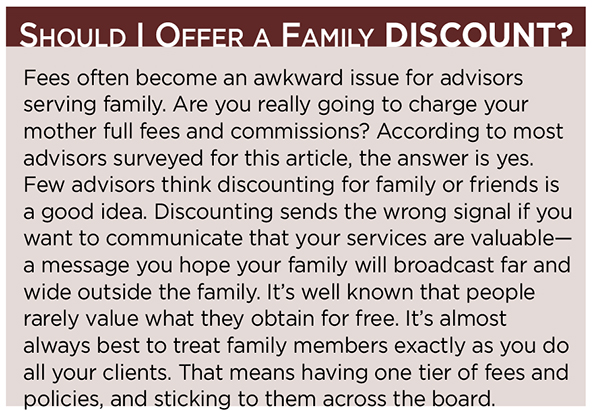

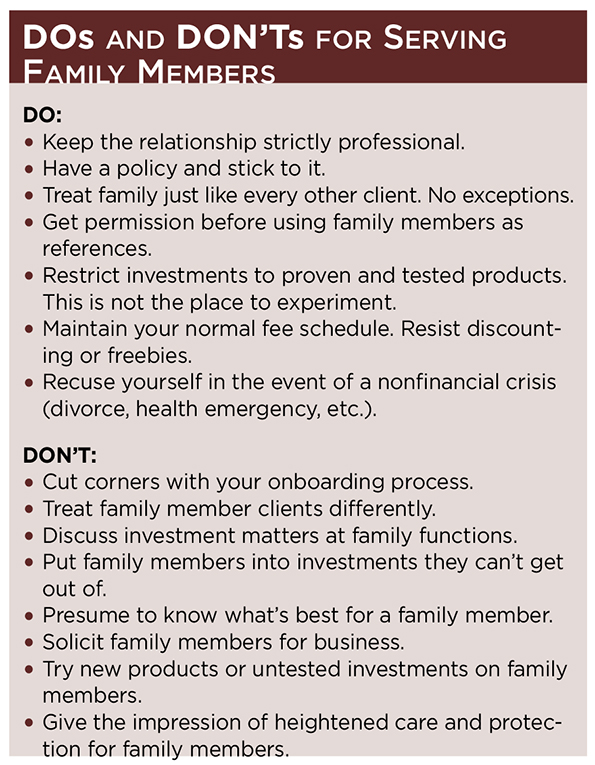

Success boils down to treating family member clients exactly as you treat all other clients, according to Blatt. That means having regular formal review sessions, ideally at the advisor’s office, not in the family member’s home and never at social occasions. Family members should receive exactly the same reports, emails and blogs as all other clients. They should receive invitations to all client and educational events. The key is to avoid creating the reality or perception of two classes of clients. There is no surer way to alienate nonfamily clients than to give the impression that they take a back seat to family members.

Even advisors who willingly take on family members as clients should be selective. That means having a written onboarding process and then sticking to it. That sometimes means declining to enlist a family member who asks to be a client. Blatt had to tell one of his siblings that her investment goals and risk preferences were simply not a good fit for the value proposition that Blatt’s firm held. He offered the family member a referral to an advisor who he thought was a better fit.

“Family members can be an advisor’s biggest champions,” agrees Kirk Jewell, President and Founder of Global Financial Services in Detroit, Mich. “My stepmother, for one, has been one of my greatest sources for ongoing referrals.”

Jewell benefits from one tremendous tactical advantage that accrues to all FAs who have family as clients. When anyone asks if the advisor would put his own mother or father into that product, Jewell can truthfully claim, “Why, yes, in fact, my own parents are in the same products I’m recommending for you.”

Many members of Jewell’s family have been clients over the 17 years he’s been in business. In the beginning, some family members admitted to helping Jewell because he was just starting out. Others opened small accounts to test the waters. But over the years, Jewell did whatever he could to transform loyalty or obligation into earned admiration and value. “I worked very hard to serve them well because family members are such a good source of referrals,” he says.

Best Practices

Jewell identifies a handful of best practices for advisors who manage family members’ money. First, he says, establish good agreements and set expectations up front. That means setting goals and defining success. Sloppy assumptions terminate many client relationships, but when it comes to family, the damage can extend beyond the professional.

“There have to be very clear ground rules about confidentiality and talking business,” Jewell says. “One of my rules is no talking about business at family events. At our initial fact-finder meeting to define the scope of relationship, I present a document for family members to sign. Then I send a summary letter to cement the agreements.” Without this level of formality, it’s easy for family members to forget and ask awkward investment-related questions at family functions.

Finally, Jewell says, advisors working with family members should challenge the assumption that they understand their financial situation. Familiarity can be blinding. “The reality is you never know the whole situation,” he says. “There were too many times I thought I had a good picture of a family member’s circumstances, only to be totally surprised,” he adds. Best practices call for treating the family member like any new client. Gather all the information and assume nothing.

Advisors know that there are unique tradeoffs to accepting family members and close friends as clients. The benefits include access to assets and a continuing source of referrals, but rarely include peace of mind. The challenges include tensions around professionalism, boundaries and confidentiality. Whether or not to accept family members as clients is a calculation that every advisor must confront.