Assessing the suitability of a buyer for your wealth management practice and negotiating the terms of the transaction are merely a seller’s early steps in “monetizing” the value of the business. In this series of articles, I’ll be examining how buyers and sellers can work together to minimize client attrition during these often-difficult transitions.

Sellers typically enjoy high levels of client trust going into a merger, so it seems reasonable to assume that it would be the seller who initially is best able to assuage client concerns and skepticism as they begin the new advisory relationship. But there is only so much that a seller can do to facilitate trust building in an unfamiliar entity. Buyers also need to play a significant proactive role in developing client trust through a courtship process that will may span the entirety of the transaction payout period.

More specifically, it is the buyer’s assigned individual wealth manager(s) who become the principal agents for trust development. And those agents need to present the image of being the client’s advocate when areas of potential disagreement arise vis a vis firm policies. It’s a tall order, but that is what it may take to win over a skeptical client.

If the transition proceeds in a satisfactory manner, and portfolio performance meets with client satisfaction, then at some point each client should begin to gain increasing trust in the buyer’s staff for assistance with all types of requests and needs.

In a recent CFA Institute study, investors ranked the following as the top reasons for leaving their current advisor:

- Underperformance – 42%

- Fees too high - 38%

- Data/confidentiality breach – 35%

- Lack of communication responsiveness - 34%

The most important function of the seller during his payout period is to discern ways to build client trust in the buyer. But trust must be earned and that takes time, typically measured in years. Skeptical clients will eventually reach their own conclusions regarding the trustworthiness of their new portfolio or wealth manager and achieve their own comfort level with the differences in portfolio management and communication style.

It takes time to settle into these new relationships while the clock is ticking down on the expiration date of the transaction payout period. Sellers are advised to periodically “take the pulse” of former clients to learn about developing dissatisfactions. Some clients won’t tell you about their dissatisfactions; they’ll simply move their assets. We all have a natural tendency towards some degree of paranoia when it comes to our wealth.

I used the word “skeptical” in the preceding paragraph to define the prevailing client attitude because, as previously noted, investors who follow their advisor to a new firm were not looking for this new relationship. They were presumably happy and comfortable where they were with their soon-to-be retired advisor. Thus, these clients begin their new manager relationships with a substantially different and apprehensive mindset compared to other investors who might actively be seeking a new relationship, happily reaching their own decision about becoming a client of another firm.

Frequent, personalized communication updates from the seller regarding transition progress is essential. Similarly, I suggest that the buyer initiate personalized communication activities as well to present itself in a positive way to the acquired clients. The buyer should recognize that it is in the midst of an ongoing courting exercise that will last throughout the entirety of the transaction payout period.

In my situation, senior members of the buyer’s firm traveled with my associate and me on several client visits during the first two years of our merger. Clients were also invited on a regular basis to visit our offices for white-glove treatment whenever they happened to be in town. Finding reasons to shine a spotlight on the buyer is also helpful, including reporting activities of staff members who participate in community affairs. We are in the people-helping-people business and humanizing the firm at the employee level is comforting to clients.

Portfolio Performance Anxiety

One of the ways skepticism and lack of trust reveals itself is in the intensity and nervousness with which clients monitor portfolio performance in the early years of the transition period. No two portfolio managers coming from different backgrounds and different investment philosophies can be expected to handle in the same manner the myriad investment decisions that arise on an ongoing basis. During the period of portfolio transition, performance numbers can be quite difficult to interpret and may bear little resemblance to the benchmark indices of either the buyer or the seller. Who takes responsibility for client short-term performance results during the months and quarters of the transition period?

I have previously suggested that sellers assume responsibility for transitioning client portfolios during the merger payout period, creating a clear path to performance ownership. To the extent the buyer manages client portfolios during the seller’s payout period, then fluctuations in the seller’s income will be a direct function of the buyer’s portfolio management successes and failures. Difficult conversations with clients may follow if the buyer underperforms portfolio benchmarks in this timeframe. The seller is left in the uncomfortable position of having to explain and defend buyer investment decisions while attempting to maintain client loyalty to the transition.

Buyer-controlled portfolio decision-making creates a higher degree of transition risk to the seller for which some counterbalancing benefit should be structured into the merger agreement. Perhaps the buyer should be held financially accountable to the seller in some manner for underperformance relative to appropriate benchmarks.

Getting Lost in the Shuffle

Appearances matter to clients. I frequently faced clients’ concerns regarding their relevance in the buyer’s organization. Before the sale of your firm, your clients were accustomed to dealing with you in your capacity as President, or some other high-ranking, C-level decision-making position. Perhaps they were a relatively big fish in your pond. It’s not reassuring to clients if in the buyer’s firm you don’t even make it onto the organization chart. Client egos can be bruised if they feel diminished in importance by virtue of the merger and it may influence their decision to remain or leave during your payout period. It’s my suggestion, therefore, that the seller seek to obtain a meaningful title and a position of authority on the acquiror’s organization chart. Who will answer to whom? What does the chain of command look like? How do lines of authority flow? The less important you and your clients are to the buyer’s organization, the more rapidly you may wish to receive your contingent payout.

On a similar theme, what resources and decision-making authority will you command during the transition period? Will you be given the authority to manage each client’s portfolio transition as you deem appropriate? Can you set your own travel and entertainment schedule as you deem appropriate? These issues matter in the clients’ eyes as they will take comfort in knowing that their former advisor now in the new firm will be able to speak authoritatively on their behalf.

As the transition period begins to wind down, will you be encouraged or discouraged by the buyer to continue speaking to your former clients regarding wealth management issues? It would be a worthwhile mental exercise for a seller to think about what client-related activities he will perform during each succeeding year of transition payout. From the seller’s perspective, continuing to be involved in client trust building activities may strengthen the client’s resolve to remain with the new firm. From the buyer’s perspective however, the view might be that the seller’s continued presence in the client’s affairs as the payout period winds down serves to inhibit the bond of trust being developed with the acquiring firm’s client representative(s).

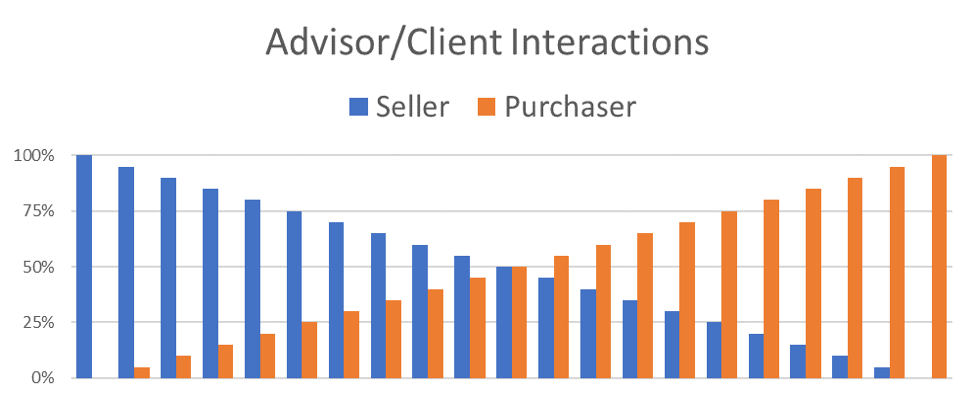

Both parties to the merger should consider creating a written timeline for seller responsibilities and activities in accordance with the concept illustrated in the graph above. Perhaps the plan could be customized for each client so that all parties are on the same page regarding the plan’s execution.

In the next and last article of this series, I’ll tackle some of the final considerations of which potential sellers should be aware, as well as what to do in the disaster scenario of being forced to disengage from the merger.

Any comments and/or questions regarding the article can be directed to [email protected].

Roger Sheffield, CFA, has been a portfolio manager and investment counselor since 1975. He has owned and operated his own RIA firm for most of this period and ultimately sold that firm to another RIA in 2017, at which time his firm’s assets under management were approaching $100 million.