The market is on a tear, up 17% so far this year. Such strong short-term performance is reason for caution in the short-term … And we may be in for some pullbacks in the market in the near future. However, the medium and long-term outlook for the US economy and stock market is excellent as I explained in my April 26th letter to investors, most of which I share below.

Perma bears are not seeing the big picture. Now is not the time to predict the economic apocalypse or “Aftershocks”. Investors need to beware those selling doom and gloom.

The argument made by nearly every economist I know is the same: “the inflation caused when quantitative easing ends will ruin the US economy for years…whenever the Fed’s massive purchasing of treasury and mortgage bonds stops, the prices of those bonds will collapse.” The Fed’s purchases are artificial demand for those bond markets to keep prices up and rates low. Without that Fed support, rates will rise and there will be nothing to stop them. Who can replace the $7+ trillion in bond purchases the Fed is making?

Next come predictions that inflation will skyrocket as the extended loose money policies come home to roost. Worse yet, the Fed, having exhausted its ammunition during QE1, QE2, QE3, etc, can do nothing to stop either inflation or rising interest rates. It is a monetary policy nightmare that results from the excessive intQerest-rate manipulation by the Fed over the past several years.

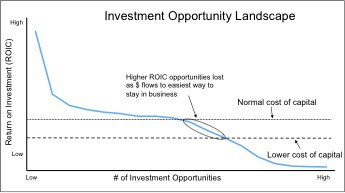

Meanwhile, the economy suffers large-scale capital misallocation as a result of a lack of the fiscal discipline that would naturally emerge if rates were not artificially depressed. I explain why that misallocation occurs in my article November 2010 article on How Artificially Low Interest Rates Harm Long-Term Growth.” This concept is illustrated in Figure 1 below. Lower rates lead to more investment in lower-return on invested capital (ROIC) business, which, in turn, produce less cash flow for the economy at large. This process compounds over time and continue to lower growth potential the longer the easy money policies persist. This idea is not new as Austrian economist F. A. Hayek first developed this idea in the 1920’s and 30’s. Slower GDP growth and an anemic job market support this theory.

Figure 1: Impact of Lowering Interest Rates/Cost of Capital

Source: New Constructs, LLC.

Perma bears also assert that the Fed’s bond buying is creating a stock market bubble as investors are forced to take undue risk to get the returns they have come to expect. As soon as bond rates go back up, large amounts of money will leave the start market for the high-yielding bonds. This shift in funds will pop the market bubble.

How could the stock market do anything but sink in the face of that future?

My answer:

I believe the US economy is undergoing a restructuring where we, as a society, are becoming radically more productive. I think that we are entering a new economic paradigm of productivity in both our corporate and labor markets. In this new paradigm, we achieve enough gains in productivity to offset the inflationary forces of QE.

As a result, I expect corporate profits to continue to rise and equity markets to be strong. Any corrections will be relatively small and short-lived – barring any major terrorist events or natural disasters.

My thesis begins with an update to Figure 1. The underlying logic of Figure 1 is so strong that it deserves an update if I am to argue against its accuracy.

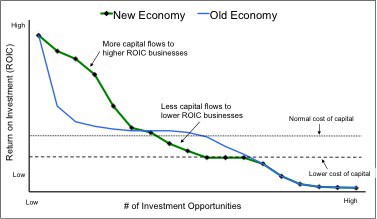

Figure 2 presents a new paradigm for capital and labor allocation in our economy. I believe that changes are afoot that are leading to a greater flow of human and financial capital into higher ROIC business while less goes to the lower ROIC business. This shift means major gains in productivity across our society as well as a widening of our country’s competitive advantages over the rest of the world.

Below I explain why I believe this new paradigm offers a more accurate reflection (than Figure 1) of what is happening in the United States.

Exhibit 2: A New Paradigm for Capital Allocation and Economic Growth

Source: New Constructs, LLC.

First, I think slow GDP and employment growth are good not bad. Think tortoise versus the hare.

- Slow rebound in GDP means businesses are allocating capital more efficiently. It also means capital is not being redeployed into the same businesses from which it was most recently taken. Usually, the first businesses to die in tough times are the worst, ie lowest ROIC. Too often after recent recessions, capital is redeployed into the businesses from which it was most recently taken and GDP is able to bounce back quickly. I do not think that is happening this time. Slow growth and slower rates of corporate investment (corporate cash balances are near all times highs) suggest businesses are being more deliberate and careful about how they spend money. Being slow and careful to spend is smart capital allocation, which lays the groundwork for higher ROICs and productivity gains in the future.

Oracle Corporation (ORCL) is a great example of a company that has grown more deliberate and more efficient with its use of capital in recent years. From 2004 to 2008, Oracle significantly increased its capital stock, increasing invested capital from $530 million to $28.4 billion. In return for that massive capital increase, ORCL barely even doubled its net operating profit after tax (NOPAT) over that same time frame, driving down ROIC from almost 400% to 23.5%. Now, that 400% ROIC was obviously unsustainable, and decreasing returns were always going to accompany the new investment required for Oracle to grow. However, the rapid rate of growth in investment and decline in returns suggests that Oracle, spurred on by the free-spending corporate culture of the mid-2000’s, was neither careful nor efficient with its capital during this time period.

Since 2008, the metrics on Oracle tell a very different story. With just 30% growth in invested capital over the past four years, Oracle has nearly doubled its NOPAT. Oracle’s ROIC is up to 32% and has risen every year since 2008. Accumulated asset write-downs totaling barely 1% of net assets attests to the minimal amount of capital Oracle wastes. If one looks only at profits, the past four years look very similar to the preceding four. However, a closer look reveals that the growth of 2004-2008 was driven by a massive capital spending, while the growth from 2008-2012 has been driven by increasing efficiency.

- The labor force is retooling its skills to focus more on new economy/digital skills. My view on the labor allocation mirrors that of capital allocation above. The jobs that were lost in the recession have not been immediately refilled because many never created value. Do we really need as many investment bankers or mortgage brokers as we had in 2007-8? Unable to go back to their old jobs, old economy workers have to (1) stay unemployed, (2) start their own business or (3) acquire skills needed to succeed in the new economy. Do not mistake the slower growth in jobs with a problem in our economy. It is a good thing that people are gaining new skills. Unfortunately, re-training takes time. However, the process of learning new skills is, in itself, rewarding because it is something we need to do more often now than in the past.

Federal Reserve Chairman Ben Bernanke made the same point in a recent speech to Bard college graduates:

“During your working lives, you will have to reinvent yourselves many times. Success and satisfaction will not come from mastering a fixed body of knowledge but from constant adaptation and creativity in a rapidly changing world.”

- High corporate profits with low job market participation means that people and businesses are facing the competitive realities that they need to move on to new occupations. Ideally, we want both profits and job market participation to be high. However, the reality of our current situation is that putting off or slowing the natural forces of creative destruction (i.e. protectionism) in the past created a backlog of workers that needed to upgrade their skills in order to keep up with the evolution of our economy. That we are working through that backlog instead of increasing it is major shift in the right direction. Fortunately, corporate profits are high so that skilled workers can get paid. We need more workers with digital or new economy skills them in the workforce.

Second, changes in our society position the U.S. for world-leading future economic growth.

- Advanced technological infrastructure is a springboard for growth. The United States offers the most advanced and stable society and infrastructure for starting and growing businesses in the world. This technological infrastructure manifests in the form of prevalent broadband access, cheap computing power, cheap memory, cheap computers, cheap software, etc – all the things that one needs to create new businesses based on new technologies. All of these tools are getting better and cheaper faster. The riches to be won from creating new tools or businesses that leverage them has inspired a large and growing portion of our work force to create more and more new and disruptive technologies. As innovation continues to accelerate, this portion of our economy will grow from the primary source of growth to the largest part of our economy. The Fed Chairman also echoed this sentiment in his speech at Bard College:

“Both humanity’s capacity to innovate and the incentives to innovate are greater today than at any other time in history.”

-

New economy productivity gains are big and getting bigger. All the talk during the late 1990s about the big impact of technology on our economy is slowly but surely coming true. New technologies are emerging at an accelerating pace, and most of them provide major advances in productivity. Already, we can see technology making improvements in just about every sector: supply chain management, logistics, shopping, vehicle repair, etc. Most of the manufacturing business that is coming back to the US from overseas is based on robotics, i.e. disruptive technologies. These businesses are growing in the United States because they can execute manufacturing processes with unrivalled productivity. Robots are the cheapest form of labor. That we are the best at making robots gives us a low-cost labor advantage versus the rest of the world. And that advantage directly improves our productivity.

-

Despite all of our problems, the US is the single best place to start and run a business. True, things are not perfect here. But we still offer the lowest cost of capital and the best environment for developing disruptive technologies. Paradigm-shifting companies like Apple (AAPL), Facebook (FB), SalesForce.com (CRM), NetFlix (NFLX) and many more are born and raised in the United States because this country is absolutely the best place to start, fund and employ the talented people needed to run those types of businesses. The US has arguably the best employee talent pool in the world along with the lowest cost of capital (WACC). Add the best technological infrastructure and you have the best place to do business.

-

The demand for new economy workers (like programmers) has remained tight even throughout the great recession as unemployment rates for new economy workers have remained low. Why do you think firms like Google (GOOG), Apple (AAPL) and Facebook (FB) compete so hard for workers and offer so many perks? Note that those businesses are among the highest ROIC businesses in the world. There are already more high ROIC businesses in the US than any other country. I expect the US to continue grow its lead in high ROIC businesses over the rest of the world.

- Retraining our labor force is painful but it gives us a competitive advantage. New economy skills are likely to be in higher ROIC businesses that leverage the best technological infrastructure of any major country in the world. In essence, we are restructuring our labor pool to focus on more high ROIC businesses. I think the restructuring of labor pool means the US is leading the world in adapting to driving force of technological innovation.

With one of the most sophisticated and malleable work forces in the world, we will have the people needed to continue to create and run the most profitable and innovative companies in the world. As a result, our economy will build on its lead over the rest of the world when it comes to innovation, technology and productivity growth.

My thesis about the US economy does not mean that stock market will skyrocket. Rather, it justifies much of the strength we have seen despite the apocalyptic prognostications of so many economists.

Picking stocks will only get tougher as this market is more discriminate about allocating value only to companies whose ROIC and profit growth deserve it.

I recommend investors do their diligence on stocks, study all the fine print in footnotes and make informed decisions. Momentum investing strategies are too crowded to be effective any longer. Investors need to get back to the business of investing and stop speculating. That means hard work. But those that do it should reap outsized rewards.

Sam McBride contributed to this report.

Disclosure: David Trainer owns ORCL. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.