During the past decade, ETFs have spread relentlessly, appealing to pensions, retail investors and financial advisors. But lately, a new group has begun buying: actively managed mutual funds. According to Morningstar, hundreds of mutual funds now own passive ETFs.

More than 100 mutual funds hold SDPR S&P 500 (SPY), while more than 70 portfolios use iShares iBoxx High Yield Corporate (HYG). Mutual funds with ETF stakes include Columbia Dividend Income (LBSAX), Monetta (MONTX) and Vanguard Windsor II (VWNFX). ETF provider SPDR says that 21 of the 25 largest fund companies hold at least some ETFs.

At first glance, it might seem unlikely that mutual funds would embrace index-hugging ETFs. After all, active funds seek to justify their fees by trying to top benchmarks. To accomplish the goal, portfolio managers have long picked stocks and bonds—not shuffled cash into index funds. Should shareholders be annoyed if their funds hold ETFs? Not necessarily, says Paul Baiocchi, an ETF analyst for IndexUniverse.com. “ETFs can be cost-effective tools that help managers to carry out their mandates,” says Baiocchi.

Mutual funds use ETFs in a variety of ways. The most common is as a parking place for spare cash. Say a large growth fund suddenly has an inflow of cash from shareholders, and the portfolio manager can’t decide what stocks to buy. He could simply hold the cash, but that could be a drag on returns if the market rises. Instead, the manager could buy a large-growth ETF that would climb in a bull market.

ETFs are also becoming popular with asset allocation funds, which aim to emphasize the best investment categories. Say a fund decides to allocate 5 percent of assets to emerging markets bonds. The manager could bid for individual securities, but it could be simpler to buy an ETF. A growing number of asset allocation funds now put most of their holdings in ETFs. That approach makes it easy to put a precise percentage of a portfolio into an asset class.

A wide-ranging asset allocator is Stadion Core Advantage (ETFRX). The Stadion portfolio managers shift their holdings, keeping up to 100 percent of assets in equity ETFs when the outlook is positive. During hard times, the equity allocation can drop to 50 percent, with the rest in fixed income. The aim is to participate in rallies and avoid the worst losses in downturns. The strategy worked in 2008 when the fund had its minimum equity position and outdid the S&P 500 by 14 percentage points.

The Stadion portfolio managers are trend followers, investing in ETFs that are rising. During the first quarter of this year, health and finance stocks were rallying, so the fund had 9 percent of assets in Health Care Select Sector SPDR (XLV) and 8 percent in Financial Select Sector SDPR (XLF). Because of the upward trend, the fund had 93 percent of assets in stocks.

The managers turn especially bullish during periods when investors seem inclined to hold riskier assets. “We want to be invested when small-cap stocks are outperforming large caps and emerging markets are outperforming developed markets,” says portfolio manager Will McGough.

Until a decade ago, the Stadion managers invested in groups of actively managed mutual funds, but they shifted to ETFs because of the low costs of ownership and trading. The managers prefer holding big ETFs that are easy to trade. Recent holdings include such popular choices as iShares Russell 1000 Value (IWD) and SPDR Dow Jones Industrial Average (DIA).

Another fund that uses ETFs is Northern Global Tactical Asset Allocation (BBALX). The fund typically has 60 percent of its assets in stocks and other risky holdings and 40 percent in safe assets such as high-quality bonds. Lately, the portfolio managers have been overweighting emerging markets and shifting away from Europe and Japan. A holding is FlexShares Morningstar Emerging Markets (TLTE). For protection against inflation, the fund holds FlexShares iBoxx 5-year Target Duration TIPS Index (TDTF).

ETFs Inside Target-Date Funds

ETFs Inside Target-Date Funds

ETFs are proving to be a natural fit for target-date funds, which are designed for people who will retire around a certain date, such as 2020 or 2030. The target funds invest in diversified baskets of stock and bond funds. As clients approach their retirement dates, the portfolios automatically become more conservative, shifting from stocks to bonds. Target-date families from big providers—such as Fidelity and T. Rowe Price—traditionally have invested in actively managed funds. Now a growing number of companies are relying on ETFs for their low expense ratios.

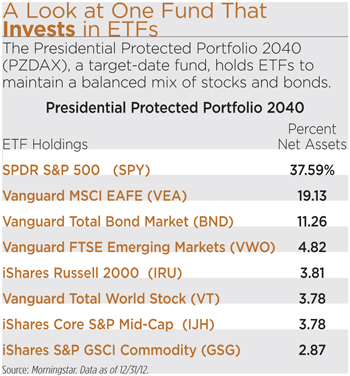

Lincoln Financial Group’s Presidential Protected series of target-date funds relies almost exclusively on ETFs. Presidential Protected Profile 2040 (PZDAX) has 76 percent of assets in stocks, including 37 percent in SPDR S&P 500 and 19 percent in Vanguard MSCI EAFE (VEA). Daniel Hayes, Lincoln’s vice president of funds management, says that ETFs are easy to trade. That is an important consideration for the target-date funds because the portfolio managers must constantly rebalance holdings, selling winners and buying out-of-favor assets.

To appreciate why Lincoln favors trading with ETFs, consider a target-date fund that invests in a portfolio of stock and bond mutual funds. Say a stock fund skyrockets. To maintain a balanced allocation, the target fund must now place an order to sell shares of the winning stock fund. That forces the portfolio manager of the stock fund to sell some holdings. The trading could generate capital gains tax bills and brokerage expenses that will be shouldered by the target fund and other shareholders who remain in the stock fund.

In contrast, trading an ETF does not typically generate such costs. When the target fund seeks to rebalance, it goes to the stock exchange and sells ETF shares to another investor. The remaining shareholders in the ETF do not face tax bills or expenses as a result of the trade. “You can move in and out of ETFs cleanly—without affecting other shareholders,” says Hayes.