A majority of advisors say Wells Fargo’s cross-selling policies do not hurt their business, but is that set to change as regulators ramp up their scrutiny?

The Wall Street Journal reported the Office of the Comptroller of the Currency and the San Francisco Federal Reserve are investigating whether the bank pushed employees too hard to cross-sell products and ignored questionable behavior.

Wells Fargo has a reputation for cross-selling clients on services offered by different divisions, such as credit cards, wealth management and mortgages, according to Reuters. In fact, Wells Fargo Advisors launched a high-net-worth partnership referral program in 2010 that was fully rolled out to advisors in late 2012. According to a May 2014 report, the group of 500 advisors holds about 10 percent of the 13,000 target households with more than $5 million in assets, yielding $4.1 billion in client balances.

The firm later lowered the threshold for the referral program between brokers and bankers to households of $2.5 million, down from initial $5 million. Last quarter, the Wealth and Investment Management division (which includes the firm’s brokerage operations) reported average loans were $61.1 billion, up 14 percent from 2014. Overall, Wells advisors are cross-selling 10.52 products per Wells bank customer.

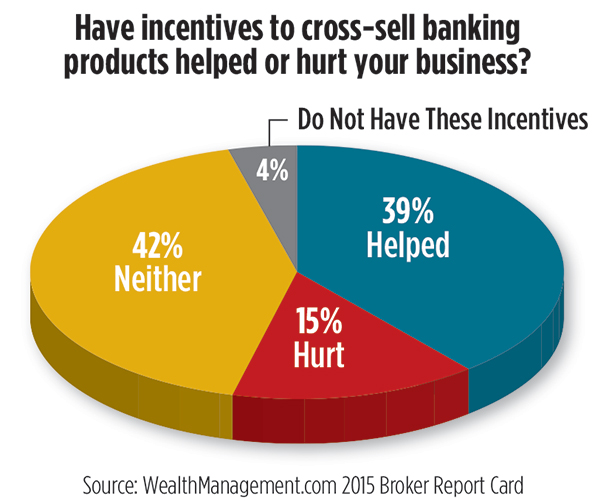

In WealthManagement.com’s 2015 Broker Report Card survey, 39 percent of Wells Fargo advisors said cross-selling banking products helped their business. That's up from the 30 percent that reported the practice helped their business in 2014.

In WealthManagement.com’s 2015 Broker Report Card survey, 39 percent of Wells Fargo advisors said cross-selling banking products helped their business. That's up from the 30 percent that reported the practice helped their business in 2014.

“I like the Wells Fargo Advisors brand, products, services and the ability to provide almost any investment or lending solution a client might need or desire. I believe Mary Mack understands the changing face of the industry and will position us in a positive way,” one advisor wrote.

About 96 percent of approximately 500 Wells Fargo advisors surveyed reported having incentives to cross-sell banking products, the highest concentration out of all six of the national brokerage firms (along with Edward Jones, Merrill Lynch, Morgan Stanley, UBS Wealth Management Americas and Raymond James & Associates) included.

When asked last year about how Wells Fargo addresses advisor concerns about handing off their clients to private bankers, Mary Mack told WealthManagement.com that the firm isn’t asking anybody to hand off a client.

“Instead, you’re bringing somebody in as a member of your team. You’re still the quarterback of that team, the financial coach for your client, but you bring somebody into your team to add to a relationship, as opposed to turn over a relationship,” she said last November.

But not all advisors are convinced. About 15 percent of advisors said the cross-selling practices hurt their business. And Wells Fargo advisors rated their firm the lowest out of the firms surveyed when asked about their freedom from pressure to sell propriety products.

“The management allows competition from all divisions of Wells Fargo. Our deferred comp is predicated upon how many loans we do for the mortgage division,” one advisor wrote.

“As advisors we pushed to make loans, which is not a real function of an investment advisors role,” another said.