A typical financial plan may land in front of a client with a thud, consisting of reams of paper on which is printed complicated charts and spreadsheets. United Capital Financial Partners has just launched what it hopes will be a different kind of financial plan that incorporates all of the firm’s tools—including the Money Mind Analyzer and Honest Conversations questions—into one sleek-looking, infographic-rich document for the client. The UC Guidebook is delivered in both bound hard copy or digital ebooks, and is updated frequently.

“It gives us a way to have planning be not an event, but a process that is dynamic, that is continuous,” said Paul Bennett, managing director at United Capital’s Great Falls, Va. office.

Bennett, who manages about $350 million in assets, has given out about 100 Guidebooks to his clients so far. To him, the Guidebook is different from other financial plans in that it ties a client’s values and priorities to his recommendations.

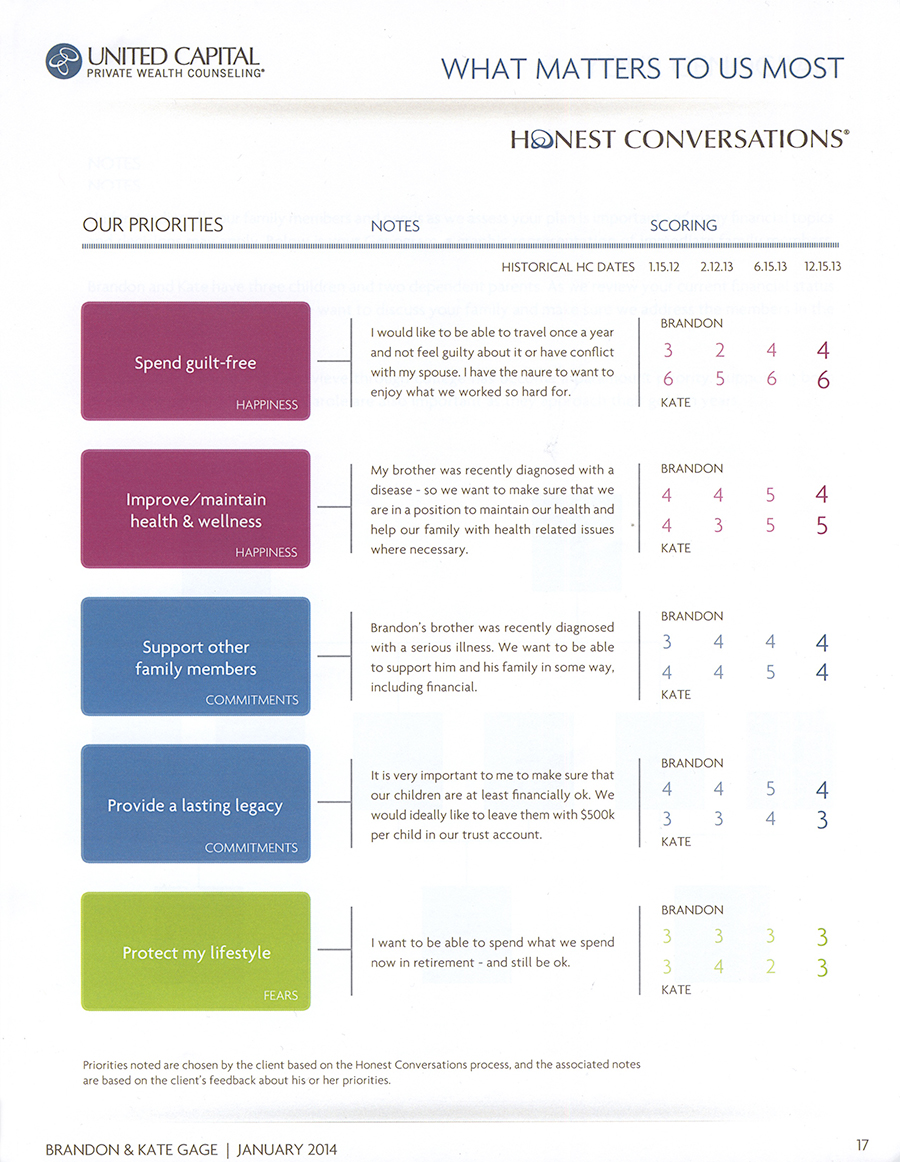

The first part of the Guidebook takes a client through the results of the Money Mind exercise, an online game that helps clients determine how they make financial decisions. The next portion reveals the results of a client’s "Honest Conversations" process, which uses a set of cards with value statements to help draw out clients’ feelings about money and financial decisions. The cards that the client prioritizes are then used to build a priority action list.

For example, if a client’s top priority was to protect their lifestyle, Bennett might make it a priority action to review their health insurance status, implement storage of financial documents or increase the frequency of a budget review cycle.

“It’s not a phonebook-size financial plan,” Bennett said. “And it’s something that they have a lot of input on, so it’s experiential.”

Each client is assigned a “funding score,” a measurement of how funded a client is to achieve their specific goals over a period of time. It’s based on a number of factors, such as financial spending goals, estimated sources of cash flows into the plan, savings, and timing, among other things. It doesn’t solely rely on rates on return.

“Rates of return are important, but those are really byproducts of the plan and the risk management, in my opinion,” Bennett said.

Bennett said he has at least one client looking to retire each month, and the Guidebook and funding score provides a clearer picture of whether that's possible, or what that retirement will look like.

“What it’s enabled the clients that are retiring to do is get much more comfortable with that concept because it’s a huge decision for these folks,” he said.

The Guidebook also includes a genogram—a graphic representation of a client’s family tree.

“We very often work multi-generationally with clients, so this kind of puts it all on paper to say who’s where in the overall family tree,” Bennett said.

Other features in the Guidebook include a portfolio snapshot, as well as recurring actions, the client’s actions and the advisor actions needed to move forward with the plan.

Bennett said many of clients like the way the information is presented in the Guidebook, with clear, easy to digest graphics and short descriptions of each section. And the entire plan is based on the firm’s interactive tools that help clients determine their goals and priorities.

“[Clients] are driving a lot of what they’re seeing on the screen and ultimately in the guidebook because of the interactions that the guidebook elicits,” Bennett said.

{kind=link}