Retirement confidence is rebounding after a seven-year decline, with 18 percent of workers now very confident in their financial security in retirement, up from 13 percent in 2013, according to a new survey the Employee Benefit Research Institute and Greenwald & Associates. But the improvement in confidence was seen only among those with a formal retirement plan, and reported worker savings remain low.

“Many of the clear warning signs about Americans’ lack of preparation for retirement have not changed,” said Jack VanDerhei, EBRI research director. “In aggregate, workers were no more likely to have done a retirement needs calculation, to have saved in retirement, or to report savings amounts significantly larger than that captured in the 2013 RCS.”

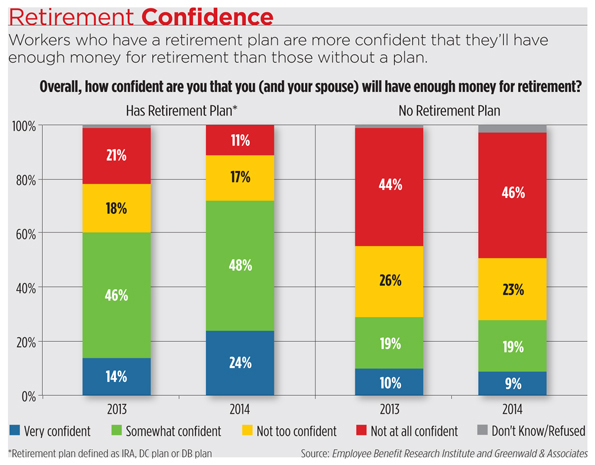

Nearly half of workers without a retirement plan were not at all confident in their financial security in retirement, compared to 11 percent for those who participated in a plan, according to the 2014 Retirement Confidence Survey (RCS). (See chart, below.)

In addition, 35 percent of workers have not saved any money for retirement, while only 57 percent are actively saving for retirement, said Mathew Greenwald, president of market research firm Greenwald & Associates. Thirty-six percent of workers said the total value of their savings and investments—not including the value of their home and defined benefit plan—is less than $1,000 this year, up from 29 percent in the 2013 survey. But when you just look at those without a formal retirement plan, 73 percent have saved less than $1,000.

“Retirement savings remain disturbingly low,” Greenwald said. “And for some segments of the population, savings have actually gone down as the sluggish recovery continues to exact a toll on many.”

Debt is also a concern, with 20 percent of workers saying they have a major problem with debt. Thirty-eight percent indicate they have a minor problem with debt.

So why, then, are people more confident about retirement? One likely reason is the rising stock market and property values last year, and the extent that those carry over into retirement savings accounts balances, which EBRI tracks.

“Many of these individuals who were more confident in the 2014 fielding than their peers would’ve been in 2013 were acting that way because they had seen such an incredible, positive increase in their 401(k) balances,” VanDerhei said.

Many workers are not aware of, or taking advantage of, ways to assess whether or not they’re on track to have enough to live comfortably in retirement, Greenwald said. Instead, they’re more focused on spending now.

“It appears that people make some assumptions about how financial secure they will be in the future based on how well the economy is performing now,” he added. “With economic conditions being somewhat cyclical, this obviously is not a good way of making these judgments or predictions of the future.”

Only 44 percent of workers said they or their spouse have tried to calculate how much money they’ll need to save for retirement. People who have done the calculation tend to save more, the report said.

The biggest shift in the 24 years EBRI has conducted the Retirement Confidence Survey has been the number of workers who plan to work later in life, Greenwald said. In 1991, 84 percent of workers indicated they plan to retire by age 65, versus only 9 percent who planned to work until at least age 70. In 2014, 50 percent plan on retiring by age 65, with 22 percent planning to work until they reach 70.

The fact that people plan on working longer could also be contributing to retirement confidence, but Greenwald believes that’s risky.

“It’s easy to say, ‘I’ll do something in 10 years or 15 or 20 years,’ than taking the action today,” he said.

“Part of it is wishful thinking, in a way, that somehow things will get better.”