By Amy Grossman

You’ve heard the news: the market for initial public offerings (IPOs) is heating up. And your conversations with affected clients should be, too. Whether your clients are executives, employees or early investors in a company going public, an IPO may create substantial wealth, potentially large tax liabilities and numerous financial decisions for them.

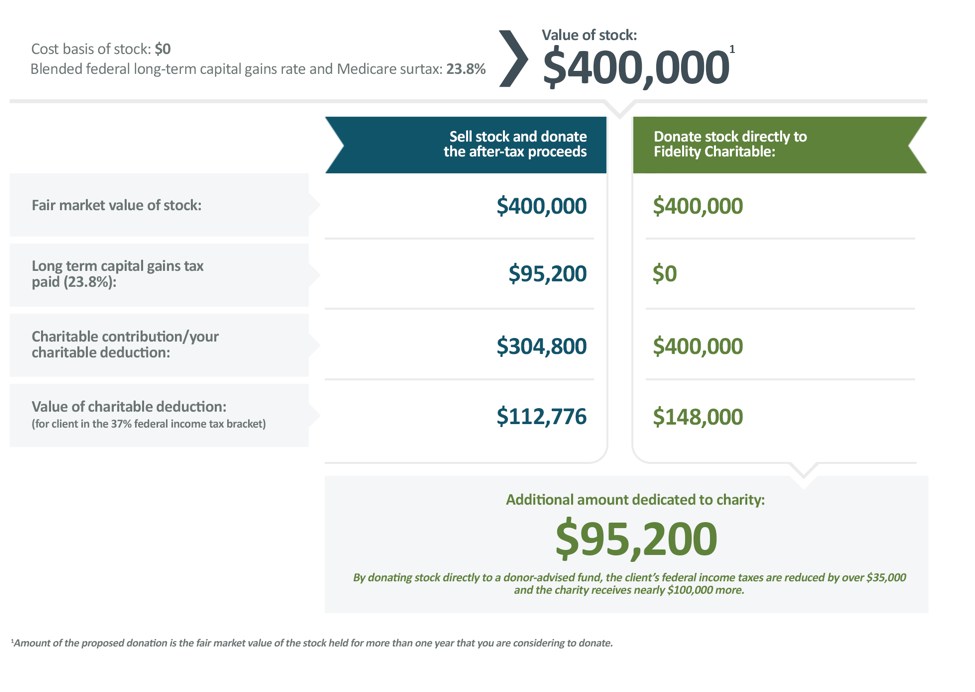

If your clients are charitably-inclined, this high income year is the perfect opportunity to consider creating a philanthropic legacy. By donating a portion of the shares from the IPO directly to charity–rather than selling the stock and donating after-tax proceeds–your clients can potentially avoid capital gains tax and realize a fair market value tax deduction, all while giving more to the charities they support. Consider this example:

You can see that donating interests in companies which will be going through an IPO may provide significant tax benefits for your clients, as well as enable them to set aside charitable dollars to support causes they are passionate about. When exploring this option, there are five things to keep in mind:

1. Holding Period

To achieve the most favorable tax treatment, you’ll want to confirm the following:

- Have the shares been held for more than a year before the contribution?

- Have the shares appreciated in value from the time of the initial investment(s)?

If both answers are “yes,” your clients are in a good position. If not, the donation does not qualify for long-term capital gains treatment and will not carry the same tax advantages. This is particularly true if they have just exercised stock options or received vested Restricted Stock Units.

2. Underwriters’ Lock-up

It is common practice for the underwriters to impose a 90 to 180 day lock-up on the shares after the IPO. That said, it may be possible to make charitable transfers or other gifts of company stock during the lock-up, provided the charity agrees to hold the stock until lock-up expiration. Whether or not the transfer is permitted will generally be determined by the issuer’s counsel.

In cases where gifts can be made during a lock-up period, since the shares are subject to a restriction that prevents them from being freely traded, your clients will generally need a qualified appraisal to determine the fair market value to substantiate their tax deduction. After the lock-up period expires, the charity controls the sale process, although in some cases it may be possible to structure a coordinated selling strategy, as long as it adheres to the charity’s program guidelines.

3. Affiliate Status

Confirm whether or not your client is considered an “affiliate” of the issuing company. Generally, this term applies to directors, executive officers, or greater than 10% shareholders. The term also applies to anyone deemed to be an “alter ego” of the affiliate (such as relatives living in the home or trusts controlled by the affiliate). Issuer’s counsel will need to provide direction on affiliate status and the process will likely require additional steps and time.

4. Company Trading Policy

Even if your client is not deemed an affiliate, the company may still impose trading restrictions on key employees, or even all employees, as well as outside investors. The concern is that employees may have inside information that they could use to trade improperly. In addition, companies will create “black-out periods” where employees are generally not permitted to transact in the stock, correspondingly giving rise to “open windows” during which they can.

While employees are prohibited from buying or selling during a “black out period,” it may yet be possible to gift stock to charity. As is the case with the lock-up, the decision will be determined by issuer’s counsel and the charity may be required to adhere to the trading policy, in which case an independent appraisal may be required.

5. Holistic Wealth Planning

Every client is unique and, therefore, it becomes especially important for you to explore the individual situation and any potential tax issues inherent in the gift. When done correctly, charitable giving can help optimize the impact of the IPO on your client’s financial situation and manage the tax burden associated with an especially high income year.

While the tax benefits can be substantial, there are nuances to keep in mind when recommending charitable gifting strategies. Working with experts experienced in navigating these issues can support your professional guidance on donating company stock pre- or post-IPO.

When considering a client’s holistic wealth plan, philanthropy is always worth discussing. Not only does it deepen client relationships, it reinforces the breadth of your wealth management expertise and differentiates your practice.

Amy Grossman, J.D. is Vice President of the Complex Asset Group at Fidelity Charitable.