By Nir Kaissar

(Bloomberg Gadfly) --Vanguard got everything it ever wanted. Now what?

That’s the question Tim Buckley will inherit when he becomes the fourth chief executive officer of the Vanguard Group in January.

During the nine-year tenure of the outgoing CEO, Bill McNabb, Vanguard’s assets under management more than tripled to $4.4 trillion, making Vanguard the second-largest money manager in the world. Vanguard gathered a record $305 billion in assets last year and is on pace to break it this year.

I think it’s safe to say that 40 years after Vanguard founder John Bogle set out to convince investors that low-cost indexing is better, Vanguard has won the argument.

While Vanguard’s conquest of the money-management business may seem inevitable, it’s a mistake to extrapolate its recent success into the future. As Christopher Wallace once cautioned: more money, more problems. And Buckley will deal with challenges that none of his three predecessors faced.

The first is that Vanguard’s investors are likely to be humbled in the coming years. Vanguard is synonymous with passive investing -- its S&P 500 index fund is still its largest mutual fund. The firm also has a U.S. home bias in its DNA. Bogle believes that investors should keep all of their money in the U.S. Vanguard recently reduced its U.S. stock allocation for client portfolios to 60 percent from 70 percent, but the U.S. bias remains.

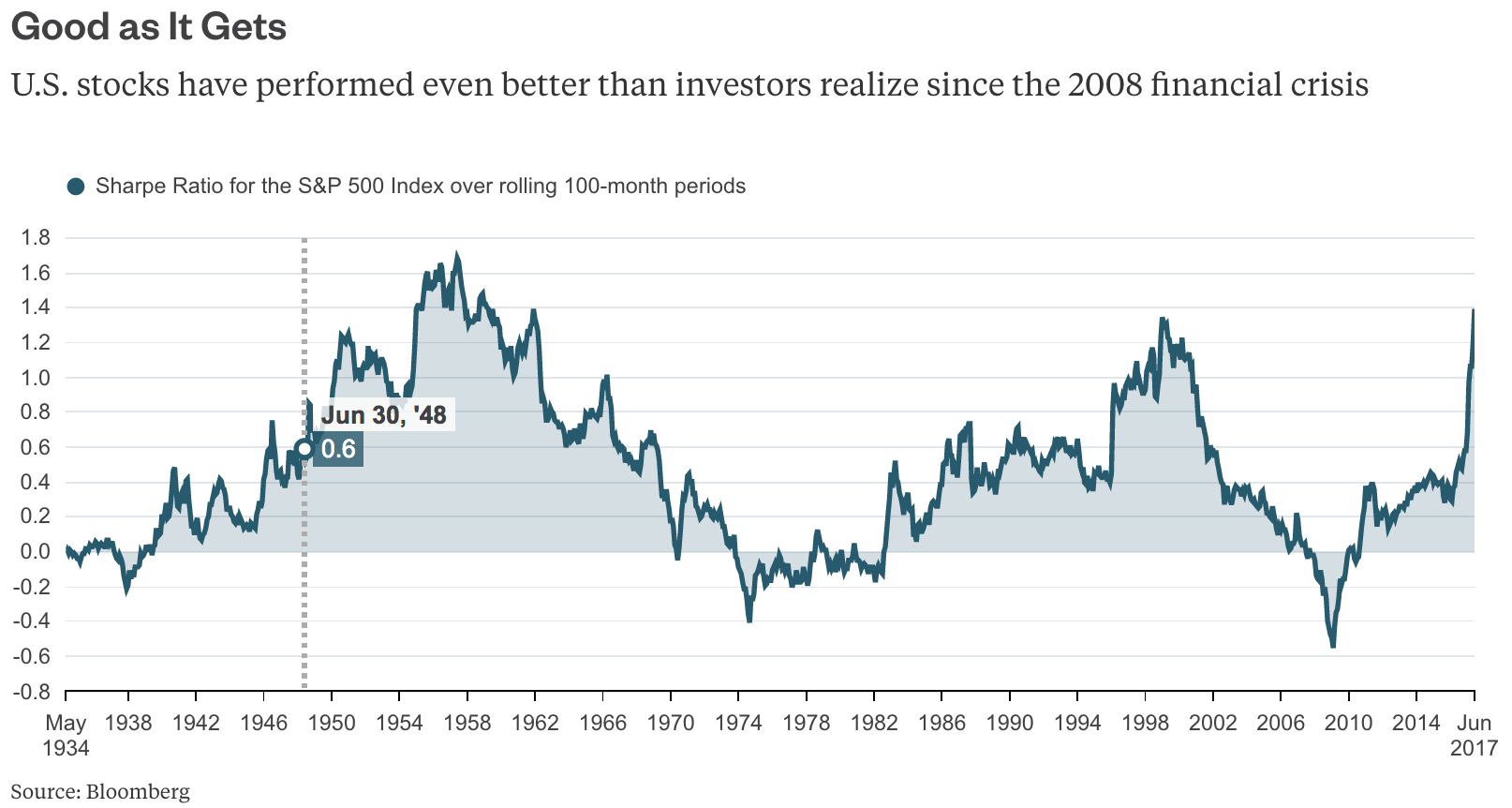

Investing passively in U.S. stocks has been a gold mine in recent years -- more so than investors realize. The S&P 500 returned 17.9 percent annually since the financial crisis receded in March 2009 through June, including dividends, with a standard deviation of 12.8 percent. That translates into a Sharpe Ratio of 1.4 over those 100 months. (The Sharpe Ratio gauges risk-adjusted returns, with a higher ratio indicating that investors are more adequately compensated for volatility.)

A Sharpe Ratio that high is rare. Since 1926, the S&P 500 has notched a Sharpe Ratio that high or higher over a 100-month period 37 times, or just 3.7 percent of the time. All of them came during a four-year stretch from 1955 to 1959.

It’s an achievement that eluded even the greatest stock pickers. During Peter Lynch’s celebrated run as manager of Fidelity’s Magellan Fund from May 1977 to May 1990, he clinched a Sharpe Ratio that high only two times -- 1.47 and 1.41 during the 100 months that ended in February and March 1987, respectively. And during the 15 consecutive years that Bill Miller beat the S&P 500 from 1991 to 2005, he did it just once -- 1.5 during the period that ended in April 1999.

So it’s highly unlikely that Vanguard investors will reap similar rewards from their stock portfolios going forward.

The second challenge is that Vanguard is no longer the lone purveyor of low-cost mutual funds and ETFs. To its credit, Vanguard persuaded investors that broadly diversified funds should cost only a handful of basis points. But as a result, fund providers are now falling over one another to give investors what they want. Even traditional active managers are cutting fees. Vanguard is quickly losing its edge.

A third challenge will be managing Vanguard’s unprecedented growth. Vanguard gathered a staggering $2 billion a day in the first quarter of this year. It has more than 20 million investors, including me. As Bloomberg News reported last week, Vanguard is facing “a rise in customer complaints such as accounting errors and longer wait times on phone calls.” No one should take for granted that Vanguard will be able to handle its surging popularity.

Buckley knows all this as well as anyone. He has already acknowledged that investors “enjoyed a long stretch of positive returns since the global financial crisis” and that they should “be ready to navigate some rough waters ahead.” And he understands what that could mean for Vanguard. Namely, “When returns are low, it is always tempting to chase the promise of return from some new approach.”

Vanguard is the best thing that ever happened to investors. There’s no going back from the passive, low-cost approach to investing that Vanguard popularized. But whether it remains, well, the vanguard of that approach will depend in large part on the success of Buckley’s coming reign.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Gadfly columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

To contact the author of this story: Nir Kaissar in Washington at [email protected] To contact the editor responsible for this story: Daniel Niemi at [email protected]