Hillary Clinton has once again thrust the debate over the dangers of shareholder activism and short-term thinking in financial markets into the national spotlight. As part of her bid to win the presidency, she proposed a number of measures to address what she calls “quarterly capitalism,” a short-term perspective in the markets which she says reduces investment in R&D and productivity measures and hinders long-term growth. In particular, she questioned the role of “hit-and-run” activist investors who press companies to increase their dividends and share buybacks, and said she would call for a full review of regulations over shareholder activism.

“Large public companies now return eight or nine out of every 10 dollars they earn directly back to shareholders, either in the form of dividends or stock buybacks, which can temporarily boost share prices,” she said in a campaign speech at NYU. “Last year, the total reached a record $900 billion. That doesn’t leave much money to build a new factory or a research lab, or to train workers, or to give them a raise.”

With that, Clinton, joined a chorus of high-profile figures who have called into question how companies should use their capital.

However, to really understand the issue we must first recognize there are substantially only four ways companies can deploy their cash: direct re-investment in the organic growth of their business, accretive growth through acquisitions, debt repayments, and returning cash to shareowners through stock buybacks and/or dividends.

Sadly, the polemics about the best and worst practices in capital allocation often tend toward simplistic extremes that miss the central point: It doesn’t necessarily matter whether companies return capital to investors or keep it under the control of insiders, since investors will naturally gravitate toward reinvesting that capital efficiently. But it matters greatly whether and how companies can produce rates of return on invested capital (ROIC) in excess of their cost of capital. In other words, what’s important is whether companies are producing returns that exceed the cost of the funds they get from investors.

On this point, everyone can agree. It is neither philosophical nor ideological. It simply examines corporate allocations of capital through the only appropriate criterion: what generates the greatest value. This is an essential measure of shareholder-friendly corporate governance. However, by this measure, our research shows that many companies are consistently using investor capital to destroy shareholder value.

To cut through the noise around this issue, Reality Shares conducted an analysis of the S&P 500 and NASDAQ-100 to determine which companies are doing exactly that. First, we examined the returns for the companies in the indexes, excluding the financial sector, to gauge how effectively companies are investing their shareowners’ capital. Then, we compared these returns with these companies’ weighted average cost of capital (WACC), a gauge of how much companies must pay investors for their equity and debt capital. The results show which companies are generating returns in excess of their cost of capital— in other words, whether they are creating shareholder value or destroying it. We used five-year average figures to capture a longer-term view.

An Analysis

As an initial screen, we examined whether the universe of S&P stocks generated returns that exceed a common cost of capital benchmark. While the cost of capital is different for every company, we compared each company’s returns against a modest 5 percent WACC target to evaluate the number of companies that would better serve their investors through the return of cash to shareowners, rather than reinvesting it in their businesses.

Reality Shares’ research shows that a significant number of companies in both the S&P 500 and NASDAQ-100 indexes have ROIC values of 5 percent or less over the past five years. Among the S&P 500, excluding financials, 132 of the 414 companies (32 percent) have a ROIC below 5 percent, while 17 of the 107 NASDAQ-100 companies (16 percent) over that time period also do not exceed a minimum 5 percent ROIC threshold. In fact, in the S&P 500, 29 companies have posted a negative average ROIC over the past five years. Sub-5 percent, including negative, ROIC is concentrated in certain industries, including, such as utilities and energy in the S&P 500 and consumer discretionary companies in the NASDAQ-100.

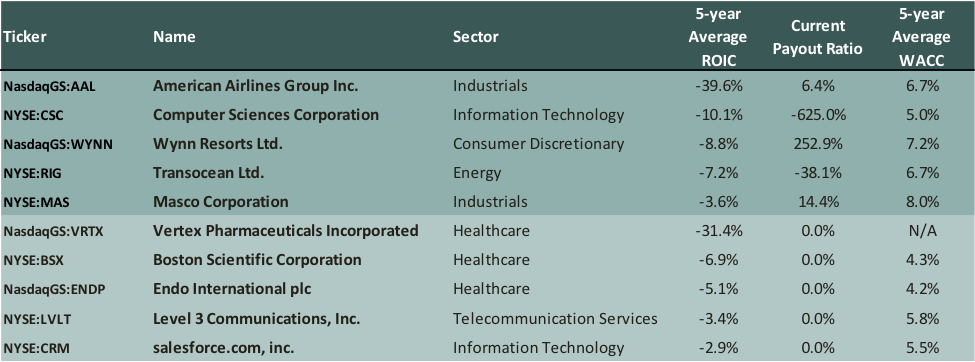

In addition, we analyzed all of the companies in the S&P 500 and NASDAQ-100 to find the firms with the lowest ROIC relative to their WACC. The chart below shows the five worst-performing companies that currently pay a dividend, and the five worst-performing companies that do not currently pay a dividend. All of the firms are generating a negative ROIC.

Three Viable Options

Companies lacking attractive, organic capital investment opportunities only have three viable options to deploy their free cash: grow through acquisitions, pay down debt, or return capital to shareowners. With both interest rates and credit spreads at historic lows, paying down debt is probably not an attractive option for most companies at this time. Likewise, with many leading investment firms, and even Federal Reserve Chair Janet Yellen, raising concerns about the lofty valuations in the equity markets, buybacks and acquisitions are relatively less attractive ways to spend shareholder dollars at this time, especially in light of research showing execution risks in both buybacks and acquisitions.

That leaves dividends as an attractive option for management teams that find themselves with insufficient options for deploying investor capital at an attractive rate of return. Rather than reinvesting internally and generating sub-par returns that destroy shareowner value, management teams can return cash to investors so they can reinvest it in other higher-returning opportunities. In addition, we believe that dividend programs benefit all shareowners by focusing management discipline on capital investment and cash management decisions.

While short-term thinking is indeed a risk whenever the markets and corporate America intersect, it’s important to recognize the context behind every company’s cash management decisions. In many cases, returning money to shareowners is the best way to stimulate growth and investment by enabling capital to flow where it can be most efficiently deployed. We believe that dividends are the most effective vehicle in those situations, because they put real cash into the hands of investors to invest in other companies.

Eric Ervin is CEO of Reality Shares. This article represents the opinion of Eric Ervin and may not represent the view of Reality Shares.

{kind=link}