Some hedge fund investors had cause for cheer when the August performance numbers were put up. The Dow Jones Credit Suisse Core Hedge Fund Index posted a 0.56 percent return for the month. Okay, a gain is a gain, to be sure, and worthy of a “huzzah.” But the hedgies’ returns look rather meager in comparison to the S&P 500’s 1.97 percent contemporaneous return.

Dig a little deeper into the hedge fund universe, however, and you’ll see why alternative investors were sporting summer smiles. Among the hedge fund subsets, the best performance was turned in by long/short equity portfolios. In August, these funds rose 1.66 percent.

“So what?” I hear you say. “That performance still falls short of the S&P’s.” You’re right, of course. But let’s dig even deeper. Not all of these funds are alike. A certain kind of long/short portfolio provoked all those grins. To understand the distinction, though, we first must appreciate the funds’ commonality. Just what are long/short funds anyway?

Long/Short Equity Explained

Stating the obvious, long/short equity is a bipolar strategy. Executing the strategy entails holding a long stock portfolio which is partially or fully offset by a portfolio of short equities. The fund’s short side serves as a hedge against market declines on the long side or as an alpha generator in its own right, adding value as the selected stocks underperform the market or decline in price. Those funds using short exposure solely to offset market risk are characterized as “hedged equity” or “market neutral” portfolios. To the extent the market effect can be held in check, the portfolio’s return isolates the manager’s talent for picking stocks.

Depending upon their mandates, some long/short equity managers may be able to vary their net portfolio exposure as market conditions warrant. These portfolios often carry a net long bias, i.e., a commitment on the long side that exceeds the short side. Consequently, these exhibit some directional exposure to the equity market, better known as beta.

Adjusting a portfolio’s beta creates value—either positive or negative—on top of any produced by the managers’ stock-picking skills. Funds advertised as following an “equitized strategy” typically overlay a permanent stock index futures position on their portfolios to maintain full equity market exposure.

Exchange Traded Products (ETPs)

Hedge funds aren’t the only way to gain exposure to long/short equity, though. Investors can now choose from an array of exchange traded products focused on long/short

equity strategies.

There are nearly a dozen ETPs with track records, including:

CSMN - Credit Suisse Market Neutral Equity Exchange Traded Notes are senior, unsecured debt securities, issued by the A-rated Swiss bank’s Nassau branch, which track the performance of HOLT’s HS Market Neutral Index.

The index is comprised of long and short portfolios—each approximately 75 stocks wide—selected from a universe of the largest capitalized North American, European and Japanese equities. The target stocks are ranked and paired, with top-tier shares placed into the long portfolio and the lowest-ranked issues lumped on the short side.

RALS - The index underlining the ProShares RAFI Long/Short ETF allocates equal dollar amounts to both long and short equity positions, based on a comparison of Research Affiliates Fundamental Index weightings with traditional market capitalization weightings. Long positions are taken in those stocks with larger RAFI weights relative to their capitalizations, while short sales are undertaken in those stocks with smaller comparative RAFI weights.

CHEP - The QuantShares U.S. Market Neutral Value Fund attempts to replicate the performance of the Dow Jones U.S. Thematic Market Neutral Value Total Return Index, a benchmark that is equal-weighted as well as being dollar and sector neutral. Undervalued stocks—that is, issues with below-average price-to-earnings, price-to-book and cash flow-to-price valuations—receive higher rankings while overvalued stocks earn lower rankings. Higher-ranked issues are bought while those with lower ranks are sold short.

SIZ - A stablemate of CHEP, the QuantShares U.S. Market Neutral Size Fund plays on the difference in performance of companies with relatively high market capitalizations versus those with low values. The fund’s underlying index, the Dow Jones U.S. Thematic Market Neutral Total Return Size Index, is equal-weighted, dollar neutral and sector neutral. The index methodology mandates placement of securities exhibiting below-average market capitalizations in its long portfolio, while stocks manifesting above-average market capitalizations are sold within the short portfolio.

QLT - The Dow Jones U.S. Thematic Market Neutral Quality Total Return Index is tracked by the QuantShares U.S. Market Neutral Quality Fund. Shares of companies with higher returns on equity and lower debt-to-equity ratios are deemed to be higher in quality and worthy of purchase, while below-average issues (representing companies with lower ROEs and higher D/E ratios) are sold short.

MOM - Momentum, measured by total return, is the determinant of the QuantShares U.S. Market Neutral Momentum Fund. Under the diktat of the Dow Jones U.S. Thematic Market Neutral Momentum Total Return Index, stocks with higher total returns over the past year receive higher rankings; stocks with lower total returns earn a lower ranking. Those issues earning above-average rankings are bought while lower-ranked shares are shorted.

NOMO - The mirror image of MOM, the QuantShares U.S. Market Neutral Anti-Momentum Fund, buys stocks with lower recent total returns and sells those issues that have appreciated at an above-average rate. The fund’s underlying benchmark, the Dow Jones U.S. Thematic Market Neutral Anti-Momentum Total Return Index, like its opposite, is equal-weighted as well as dollar and sector neutral.

BTAH - Rounding out the QuantShares suite of market neutral products are a pair of complementary beta-based funds. The QuantShares U.S. Market Neutral High Beta Fund attempts to replicate the Dow Jones U.S. Thematic Market Neutral Beta Total Return Index which assigns high beta—more volatile—stocks to the long portfolio and low beta issues to the short side.

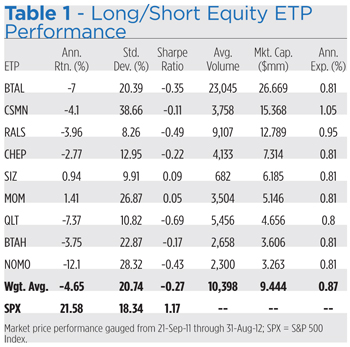

Table 1 ranks these ETPs by size and compares their recent performance to the S&P 500 (SPX). The top performer—the QuantShares MOM fund—posted an annualized return just north of 1 percent with a standard deviation near 27 percent. The fund’s above-market volatility, however, yields a second-best Sharpe ratio, below that of the capitalization-based SIZ portfolio.

Table 1 ranks these ETPs by size and compares their recent performance to the S&P 500 (SPX). The top performer—the QuantShares MOM fund—posted an annualized return just north of 1 percent with a standard deviation near 27 percent. The fund’s above-market volatility, however, yields a second-best Sharpe ratio, below that of the capitalization-based SIZ portfolio.

Not surprisingly, the worst performance was turned by the anti-momentum NOMO fund.

Despite earning a weighted average 1.04 percent return in August, these nine products grossly underperformed a buy-and-hold long position in large-cap stocks over the past year. Collectively, they’ve put up a beta of -0.15, meaning they’ve modestly zigged when the S&P 500 zagged. For that, they registered -0.01 on the alpha meter.

With the foregoing in mind, you might think that beta —positive beta, that is—was a font for profit over the past several months. You’d be right. To appreciate that more fully, you have to look at the two long/short equity products we’ve not yet examined. Both follow a “130/30” strategy, which is to say their long exposure is levered to 130 percent of market cap, facilitated by a short exposure of 30 percent.

The underpinnings of the strategy can be illustrated with a simple example. Suppose a manager makes an investment of $1 million in undervalued stocks from a basket, such as the S&P 500 index, while shorting $300,000 in basket shares he deems overvalued. Proceeds from the short sale are then used to purchase an additional $300,000 of the basket’s undervalued issues. Thus, the manager ends up with $1.3 million invested in long positions and $300,000 in short positions. The manager’s leverage factor in this instance is 1.6—$1.6 million in total commitments are capitalized with $1 million.

Clearly, this portfolio is lopsided. It inherently exhibits a long bias, yet strives to maintain a 1.00 beta coefficient. The target market exposure nets to 100 percent (130 percent long + 30 percent short = 100 percent net long). This is, in fact, the raison d’être for these products—alpha harvesting at no more than the cost of market risk.

Proponents of the 130/30 strategy contend that long-only—especially index-hugging—portfolios leave a lot of alpha untapped. A manager, for example, may rank—from overvalued to undervalued—all the stocks in an investable universe, such as the S&P 500, but if he can’t sell short, a lot of that information is just tossed aside. Managers saddled with a long-only constraint are forced to seek value solely from market outperformers. That’s a pretty hard slog because, historically, more stocks have lagged the S&P 500 than have beaten it. A long-only mandate effectively turns off an alpha spigot.

Portfolio managers who can’t significantly underweight the weakest stocks, at best, can only shun ownership. About 80 percent of the stocks in the S&P 500 represent very small—a half-percent or less—weightings in the index. That leaves a long-only manager discretion to underweight such issues by as much as, but no more than, a half-percent. Relaxing a long-only constraint allows the manager to meaningfully increase commitments to a negative view, e.g., to a 1 percent or 2 percent underweight or more.

This short-enhanced approach underlies two exchange-traded products:

CSM - The ProShares Credit Suisse 130/30 ETF attempts to replicate the performance of its benchmark—the Credit Suisse 130/30 Large Cap Index—which holds 130 percent long and 30 percent short exposure in a stock universe quite similar to the S&P 500.

JFT - An exchange traded note, the KEYnotes First Trust Enhanced 130/30 Large Cap ETN, tracks a broader index. The First Trust Enhanced 130/30 Large Cap Index ranks a 2,500-stock universe for inclusion in the 130/30 portfolio. The notes, maturing in 2023, are issued by JPMorgan Chase, an A+ credit.

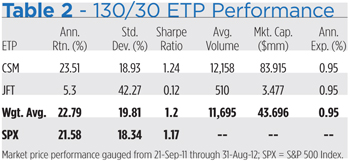

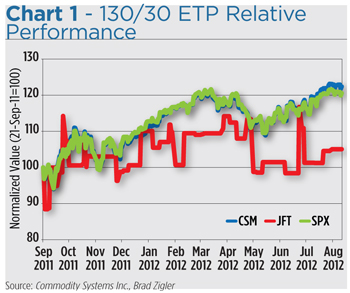

The recent performance of these ETPs is depicted in Table 2, further illustrated in Chart 1.

In August, the 130/30 ETPs bested the S&P 500 with a weighted average gain of 2.96 percent. Over the past year, the ETPs edged the blue-chip benchmark with only a modest uptick in volatility. More telling is the collective beta for the 130/30 products—0.96—pretty much equal to that of the S&P 500. In sum, these two ETPs earned a weighted average alpha of 0.02. That’s a positive value, mind you, as opposed to the negative 0.01 posted by the other exchange-traded products.

Still, the individual performance characteristics of CSM and JFT seem disparate. That’s in large part due to their differing benchmarks. CSM’s investment universe is virtually congruent with the S&P 500. JFT’s is much broader and includes more small, risky stocks. The relative illiquidity of the exchange traded note as well as concerns about the creditworthiness of its issuer are also reflected in its market price.

Still, the individual performance characteristics of CSM and JFT seem disparate. That’s in large part due to their differing benchmarks. CSM’s investment universe is virtually congruent with the S&P 500. JFT’s is much broader and includes more small, risky stocks. The relative illiquidity of the exchange traded note as well as concerns about the creditworthiness of its issuer are also reflected in its market price.

Is Beta Better?

One thing is certain, though. The equity market’s recent uptrend has made beta a good friend to long-biased investors. For those seeking a clearly defined—and benchmarked—market exposure with an alpha kicker and are willing to absorb a modest amount of active risk, a 130/30 play seems to make sense. At least for now.

Keep in mind that 130/30 is more structure than strategy. A proprietary stock selection methodology must still be relied upon to pick the right stocks—short and long—to earn alpha. Relaxation of the long-only constraint simply makes it possible for more of the manager’s or index creator’s ideas to find expression in the portfolio, for better or worse. The adage “garbage in, garbage out” holds true for asset management just as it does for computer programming.

To determine if these products are appropriate for inclusion in an investment portfolio, keep the benchmarks in mind. Most 130/30 plays are staged in the large-cap space since big stocks are typically the most liquid and easiest to borrow. Not surprisingly, these funds are mostly benchmarked to the S&P 500. That said, 130/30 products are most appropriate as part of, or replacements for, large-cap exposure.

So, is beta an investor’s best friend forever? Nothing in the investment realm lasts forever. But to the extent one feels confident in the longevity of the large-cap uptrend, beta makes for a pretty good traveling companion.