Panicking in the face of a pandemic (or any dramatic event) is a terrible way to manage a stock portfolio, and it doesn’t work well with your clients’ life insurance coverage either.

The most important thing to remember when it comes to life insurance coverage is that a claim will be paid even if the cause of death is the reason for the pandemic—in this case, COVID-19. To the best of our knowledge, there are no insurance carriers that exclude coverage due to pandemics.

With that said, however, if your clients have been worrying about their coverage, you can review with them certain issues now (and periodically). Points you can help them evaluate might include whether the coverage is adequate (or too much) or whether they might have issues paying premiums, etc.

Ten Steps

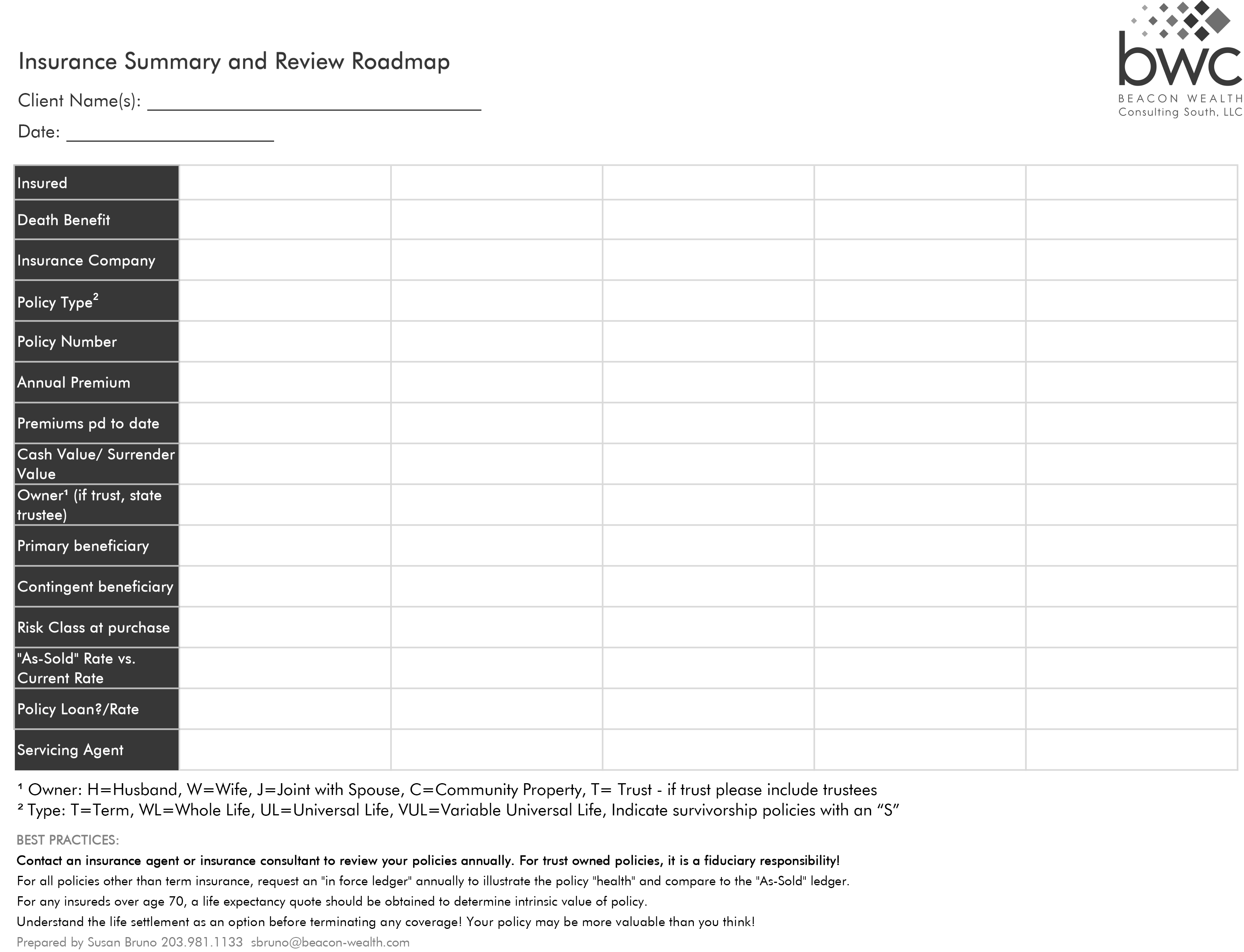

- Use the “Roadmap” below, which is a fillable spreadsheet that will help you summarize the key elements of your client’s life insurance coverage.

- Find a copy of all life insurance policies. Your client should save the original policies in a secure fireproof place (for example, a safe deposit box) and electronic copies on his home computer or cloud-based server like Dropbox.

- Can’t find the policy? Your client should find the most recent premium notice and call the agent, the insurance company or his current insurance advisor if his policy search comes up empty. He should get a new copy of his policy and save it physically and electronically.

- If your client has a group policy with his employer, he should locate his benefit statement and record all relevant account information and his HR/benefit manager’s contact information.

- After you and your client complete as much as you can on the Roadmap, consider whether the coverage amounts and beneficiary designations are still appropriate for your client’s family needs. When considering coverage amounts to protect survivors, consider the fluctuations and uncertainties of the stock market and whether your client faces a risk of unemployment or business decline. Your client might wish to supplement what he has (his savings may be worth less than anticipated). If your client is worried about estate tax, consider that the massive bailouts may result in significant estate tax increases. So, don’t cut back if under new rules your client might need coverage.

- If your client is applying now for life insurance, he should fully and accurately answer all medical questions, especially questions that are related to any issues associated with or similar to the COVID-19 virus. It’s quite likely that anyone experiencing any of the symptoms, or who’s tested positive for the virus, will have their underwriting decision postponed until such time as they’ve fully recovered and are no longer exhibiting symptoms or have tested negative for the virus. This postponement period may vary but is typically 90 days from date of recovery. As the pandemic unfolds, insurance carriers will take additional steps to protect themselves from underwriting risks created by the virus. Your client might have to attest that neither he nor any household member has within the past 30 days traveled or resided outside of the United States or by cruise ship, or has come into close contact with anyone known to have tested positive for COVID-19.

- Before lapsing a life insurance policy, make sure your client confirms that he’s healthy enough to buy new insurance should the need arise. If there are health issues and coverage is still required, review any term insurance in your client’s portfolio and determine what are the conversion privileges. Finally, if your client is sure that he wants to cancel coverage, he should ask his insurance advisor about the secondary market to see if he can get cash for his policy. This is called a “life settlement” and can possibly provide your client and his family with immediate cash depending primarily on his age and current health.

- Your client should set up a time to review his completed spreadsheet with his insurance consultant. Don’t worry if he can’t answer all the fields. For permanent coverage, make sure the agent provides in-force illustrations that can project out future expenses and performance. The agent should be happy to discuss and, if not, then your client should find a new agent! With the help of the agent, your client should complete the spreadsheet and save it with his policies (see above) and provide it to key people (for example, the trustee of his insurance trust and key advisors), along with location of policy.

- Encourage your client’s parents and adult children to do the same.

- Repeat each year!