Not long ago if an advisor was a big enough producer, his or her regulatory and credit history didn’t matter as much. As long as infractions were not criminal, he or she could still find a place to do business—if they kept producing. Likewise, if a broker with a spotless record left a firm that ran afoul of regulators, or had more than its fair share of brokers who had, there was no implied guilt by association. They too could find a place to hang their licenses.

“Those days are gone,” says Ryan Shanks, CEO and founder of Finetooth Consulting and co-founder of JoinAFirm.com. “It doesn’t matter if you come in and you think you’re with a great firm and you’re doing $5, $6, $7, $8 million in revenue. If there’s liability, firms are not going to touch it. That is a significant change from the way it used to be in the business.”

“In a lot of instances, there are firms that don’t want anyone with even one strike,” Shanks says.

At least when it comes to the world of independent broker/dealers, the Financial Industry Regulatory Authority—the industry-funded regulator—is cracking down. Its stated 2014 priority is to focus its regulatory firepower on “high-risk” brokers, and it may investigate firms’ hiring and due diligence processes.

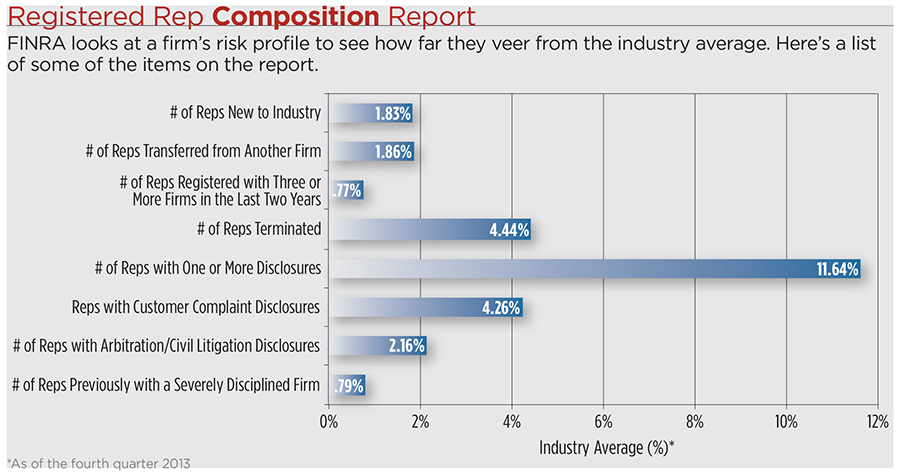

![]() According to industry observers, including those who have witnessed the change in emphasis firsthand, FINRA is looking more closely at risk monitoring and rep composition reports to help spot trends, like the number of reps with one or more disclosures; customer complaints or arbitration disputes; the number of terminated reps; or even the number of reps who have been with three or more firms in the last two years.

According to industry observers, including those who have witnessed the change in emphasis firsthand, FINRA is looking more closely at risk monitoring and rep composition reports to help spot trends, like the number of reps with one or more disclosures; customer complaints or arbitration disputes; the number of terminated reps; or even the number of reps who have been with three or more firms in the last two years.

The result is some reps are finding it harder to find a b/d that will work with them—often even if they have done nothing wrong.

“Because the regulatory environment has been getting tighter at the firm level and at the representative level—and in some instances that is good for the business—you have to be a little bit more concerned about the types of reps and advisors you bring on, strictly because the regulators are taking a harder look at the types of personnel that are providing investment advice,” says Tom Heffernan, vice president of marketing at independent b/d MoneyBlock.

Risk Monitoring

Jonathan Henschen, president of recruiting firm Henschen & Associates, says he’s hearing from some b/ds that FINRA is using the rep composition report now in audits, encouraging firms to get their averages down in certain categories if it’s above the industry average. (See table.) FINRA did not respond to requests for comment.

“There’s a few Midwest states where I’ll hear broker/dealers say, ‘FINRA is telling us don’t bring on any more reps with credit issues or former bankruptcies, and if we do, they told us we’re going to make your life more difficult,’” Henschen says. “It’s like, ‘I’m taking you to the woodshed’ time.”

Paul Tolley, chief compliance officer of Commonwealth Financial Network, says FINRA didn’t use the rep composition report when they audited his firm, but he does see the regulator is focusing more on brokers’ records and those of the firms they came from, and in his eyes, it’s a welcome change. For one, taking a more systematic approach means the regulator can complete an exam in less time. FINRA examiners spent less than two weeks at Commonwealth’s home office during this year’s audit, versus six to eight weeks for past audits. But the regulator more than doubled its branch office visits.

“[Examiners] are undoubtedly—from the information they’ve been getting from risk assessments—coming in better informed about where to focus,” says Don Runkle, director of consulting services at Edgerton & Weaver. “It wouldn’t surprise me at all if some firms have found that FINRA has really cracked down on them in a certain area and therefore they’re not going to hire that kind of advisor anymore. Whether or not it’s specifically the risk assessment or FINRA ramping up what it does in general, you never know.”

But a rep doesn’t always deserve to be lumped in with bad brokers. An advisor may have one too many marks on their book or jumped from firm to firm for good reason.

“You look at the disclosures, and maybe one or two of them there was a fine paid for whatever, and three of them were ‘no action taken,’ or it was discharged because it was frivolous,” Henschen says. “The fact that you have marks, you got to take it in context.”

This year, FINRA said it would put a new focus on brokers who leave firms that have been severely disciplined, even if it was not the fault of the individual rep. At the end of 2013, that included about 5,200 advisors, according to the Rep Composition Report. Many firms now keep a list of problematic b/ds, and won’t touch advisors coming out of them, Henschen adds.

“If you’re at a bad broker/dealer and you got a clean record, why should that haunt you?” Henschen asks. “Your record is your responsibility.”

“Because there’s been some additional consolidation, some of the smaller broker/dealers have ceased doing business, we have to look into the details as to what happened at those firms—whether it was strictly an economics issue or whether it was a regulatory issue,” MoneyBlock’s Heffernan says. Not that the two are exclusive, of course. Regulatory issues, or the costs of complying with them, can lead to economic issues.

Out of the Business?

As firms become more selective in the advisors they bring on, it will get more difficult for those with checkered pasts to find a home because it may move the needle on a firm’s risk composition grid.

“In most of these reports, for smaller firms, the percentage weighting is going to bang around a lot more, because an individual rep or a multi-rep advisor office that has a number of marks will heavily weigh on the overall firm’s imprint, versus a larger firm that may be able to absorb that book of business,” Heffernan says.

Smaller broker/dealers used to bring on reps with more dirty laundry than they would care for, to build scale and establish themselves in the marketplace. “But the number of firms that are friendly to reps with that type of model is going the way of the dinosaur,” Henschen says.

Some of those firms have simply gone out of business. In the last 12 months, 248 b/ds have closed up shop, according to Fishbowl Strategies.

“When it comes to newer people [to the industry] there is far less patience for that type of thing now,” says Ron Edde, co-founder, president and CEO of Millennium Career Advisors. “You got a minimum book, and you got a CRD flag—a lot of those people are just saying, ‘to hell with it. I couldn’t get an offer.’”

“Without a doubt, there will be some folks that unfortunately have to find something else to do with their time in order to make a living,” Shanks says.

In 2013 and 2014, 3,264 advisors left the independent broker/dealer channel, according to data by Meridian-IQ.

“What you’ve seen over the last five to 10 years is a number of advisors disconnect from the broker/dealer, take the fee-based business with them, set up an RIA,” Shanks says. “And they’ve had the assumption that ‘I’m going to get away from regulation.’ The reality is the regulation’s catching up.”

The Securities and Exchange Commission has made it a priority to examine previously unexamined RIAs, and to get more resources to make that happen.

But Runkle says it’s not rogue advisors who are going to the RIA side to skirt the rules.

“What I’ve actually seen is some high, high quality advisors step out of the FINRA world, mainly because of the burden of the regulation, not because it’s keeping them from doing the business they want to do,” Runkle says.

{kind=link}

{kind=link}