The passing of Daniel Kahneman, an Israeli-American author and psychologist, got me thinking. Like me, Kahneman had deep ties to my hometown of Chicago. While we never met, I admired his Nobel Prize-winning work in behavioral economics and his explanation of the important role of psychology in financial decision making. For instance, he pioneered work that included the “regret minimization strategy,” which helped investors devise a portfolio based on how much they felt they could risk and still sleep at night. He also quantified “loss aversion,” noting that people feel the sting of an investment loss more significantly than the joy of a gain. He also quantified that making more money doesn’t necessarily make you happier. Depending on where you live, Kahneman found that earning more than $70,000 to $90,000 a year won’t make you happier as long as you’re meeting basic living expenses.

One of the things that my business partner, Craig Stone, and I talk about all the time is the qualitative side of planning. That’s very different from the quantitative side, where most advisors like to spend their time. We’ve found very little cohesion between what the family wants and what gets put on paper. I can’t tell you how often an attorney or CPA calls me at the last minute and says: “Randy. I’ve got a client with this problem. What’s the solution?”

It’s like walking into a doctor’s office and saying: “Doc. I don’t have time to do tests or X-rays. Just write me a prescription.”

In those situations, I tell the advisor I’m happy to help, but it’s tough to recommend a solution until I understand who your client is, how they’re wired and their goals for themselves and their loved ones. It’s about taking time to have meaningful discussions with clients and asking questions that no one else is willing to ask. Sometimes, you must challenge clients and push back to arrive at the best possible solution. To do that, you need a blend of math, legal and psychology skills. Our profession is full of people who are excellent at math and legal issues but not as accomplished in understanding human emotion and psychology.

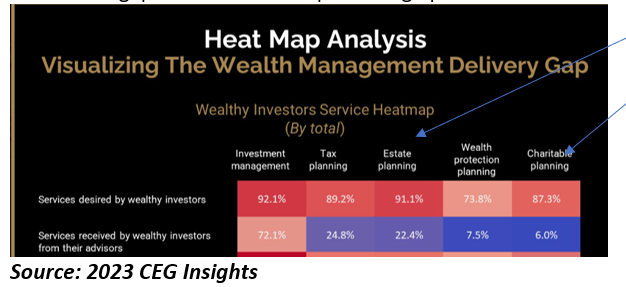

And that’s why there’s such a big gap between what successful clients want and the services they say they’re receiving from their advisors. For instance, in a 2023 survey of over 1,100 wealthy investors and financial advisors by CEG Insights (see chart below), 91% of wealthy investors sought estate-planning services. Still, only 22% said they were receiving those services from their advisors – a gap of nearly 70 percentage points! Further, 87% of wealthy investors said they sought charitable planning services from their advisors, but only 6% received those services– a gap of more than 80 percentage points!

What gets taught in every financial course and certification program these days is the technical/analytical structure of planning. Not much time is spent on understanding the human mind. And that’s a big problem because planning entirely from a math and legal perspective means there’s always a definitive answer to every question or issue. Everything balances out. You’re allowed to do this. You are not allowed to do that. There’s not a lot of gray area here. But that’s what real life is all about.

So, advisors must develop empathy, deep listening skills and good question formulation. Many think those skills are innate, but I’ve found you can learn to develop those “soft skills.” The challenge is that most legal and financial practitioners determine how those intangibles fit into their business model. They can’t figure out how to get paid for that type of expertise. But the modern advisor needs to approach each client as a person, not as a case. You need to know their values and motivations because what we’re trying to accomplish must last for multiple generations. We want to do it right the first time; we don’t want to keep doing it repeatedly.

Another problem with advisor training is that new professionals aren’t learning how to show their vulnerability. They don’t like to admit to clients that they don’t always know the answer. But sometimes, you must be brutally honest about what you’re good at (and most knowledgeable about) and what you’re not. The leaders of the pack are those who know what they’re best and leverage those skills while they hire the best people they can find to fill in their knowledge and expertise gaps.

If a client trusts you with intimate details about their estate planning and legacy giving, “faking it till you make it” isn’t going to fly. They have too much money, and multiple generations of their family depend on you to help them make the right decisions. Put your ego aside and get the training you need, or find a skilled professional to assist you. It’s as if we’ve lost an entire generation of estate and gift planners thanks to the 2017 Tax Cuts & Jobs Act that raised the exemption limit to the stratosphere (until 2026). Soon we’ll be playing catchup in a very big and painful way.

Randy A. Fox, CFP, AEP is the founder of Two Hawks Consulting LLC. He is a nationally known wealth strategist, philanthropic estate planner, educator and speaker.