The world seems to be changing at lightning speed, but sometimes I’m surprised by how little things change. Let’s go back a dozen years to 2012. In the National Football League, the 2012 Baltimore Ravens and San Francisco 49ers led their respective conferences and headed into the playoffs as odds-on favorites to meet in the Super Bowl. Democrats controlled the White House, but the incumbent wasn’t too popular. The Fed was active on the rate front. The economy and stock market were rebounding strongly from a once-in-a-generation crisis. Sound familiar?

My book The Great Wealth Erosion was also published in 2012. At the time, I was shocked by the degree to which investors were lagging the stock market indexes that they (and their advisors) were supposed to be tracking. At the time, Dalbar research showed that over the previous 20 years, equity investors as a group lagged the unmanaged S&P 500 index by 4.6% a year on average. Fast forward to today and the performance gap has narrowed only slightly to 3.1%. With all the advances in technology, AI and supercomputing, why are active investors finding it so hard to keep pace with the unmanaged, do-nothing approach?

As was the case in 2012, there are four critical factors driving this underperformance and thus erosion of wealth. You owe it to your clients to prevent these hidden factors from decimating their wealth:

- Market Volatility

- Portfolio Construction

- Expenses and Fees

- Taxes

As the old saying goes: “The more things change the more things stay the same.” Let’s look at these four factors more closely.

1. Volatility. Markets go up and markets go down. This is the immutable law of markets. Anyone who invests in securities must accept this reality. An investor must be willing to endure the randomness of market movements and not bail out every time a sudden drop comes along. As many of you know, the biggest gains in the stock market tend to come shortly after a significant downturn. But your clients won’t be there to capture those gains if you let them bail out at the first sign of trouble. But there are ways to control the amount of volatility inherent in every portfolio. The two most important questions to ask are: (a) “How much risk is your client buying?” and (b) “Are they buying the right kind of risk?” Once you can answer that question for each client, you can move on to portfolio construction.

2. Portfolio Construction. There are two important questions to ask when it comes to portfolio construction. First, are there proven, consistent ways to build a portfolio that will deliver long-term rates of return reflective of your client’s risk tolerance? Second, which strategy is better for diversification: Owning 15 or 20 stocks, an array of mutual funds and ETFs with 200 to 500 stocks or owning the entire market? Let’s look to the father of modern portfolio theory, Harry Markowitz, who received a Nobel Prize for proving that diversification is the key to managing risk. He showed that a well allocated portfolio will safeguard your client against unforeseen economic events and will benefit from technological advancements. His research showed broad diversification protects a portfolio from the ever-present pace of change and that the right portfolio construction enables you to diversify your clients properly and to capture higher returns once the market recovers from its inevitable declines.

3. Fees and Expenses. John Bogel built his empire at Vanguard by significantly lowering the fees investors had to pay for mutual funds and ETFs. And the industry followed. So, if you see your clients paying 2x to 3x more than necessary to achieve the same returns, would you still recommend those investments or funds? Of course not.

Remember the 4.6% spread between the market and the average investor discussed above? Research shows about 3% of that 4.6% spread could be attributed to poor allocation and paying excess fees and trading costs. The remaining 1.6% was due to improper portfolio management and irrational investor behavior. A dozen years later that disparity largely remains. As was the case 12 years ago, there are disclosed costs and undisclosed costs. The disclosed costs are described in the fund prospectus for things like management fees, advertising and administration. It’s the undisclosed fees that truly affect the bottom line and so often erode your clients’ returns.

These fees have to do with commissions and the bid-ask spread. They are directly related to portfolio turnover, especially in down years. Sure, investors cannot control these expenses, but you can select funds that minimize turnover. These fees are related to the type of investment vehicle you select to spread your clients’ risk. Choose wisely!

4. Taxation and Turnover. Obviously, if your client’s money is in a qualified plan, an IRA or 401k, then taxes on accumulation are not an issue. The government will get its pound of flesh when your client starts taking distributions. Taxes are postponed until the account is liquidated or distributions are being made. But there are limitations placed on how much an investor can allocate to a qualified plan. Many investors have other money to invest. This non-qualified money is subject to taxation on the annual growth. This is where turnover becomes so important.

Portfolios with high turnover—such as with actively managed funds—usually face high taxes and heavy expenses on top of high management fees. So now you’re not only facing the current tax cost, but the compounding effect of the cost on your clients’ portfolios. Assume a client earns 10% for the year. If turnover is 100%, then it’s likely that 100% of any gain is recognized for tax purposes that year. The gains are taxed at ordinary income tax rates—40% for many of your clients—because these sales did not qualify for long-term capital gains rates. This means your client only netted 60% to 75% of the recognized growth that year. But the next year, if their net portfolio grows an additional 10%, what happens? They don’t get 10% on the taxes they paid. That money has been extracted from the portfolio. Your client only gets the 10% on the remaining 60%. When this happens year after year, their portfolio is dramatically impacted by the tax effect.

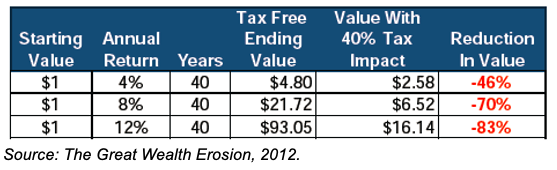

The table below shows the impact taxes can have on your returns.

Consider how a portfolio in which only a small fraction of the gain is recognized would be impacted. If only 20% of the gain from the previous example is taxable, that means 80% of the gain would still be in the portfolio and would benefit from any additional growth the following year. You might be scratching your head and wondering why one portfolio would be subject to taxes on 100% of the growth while another would only be subject to taxation on 20%. The answer is turnover.

According to Morningstar, the average turnover rate for mutual funds can often exceed 100%. That means 100% of any gains each year are likely subject to the ordinary income tax rate. Since the positions were held for less than one year, they do not qualify for the 20% long term capital gains tax rate. Bottom line: Taxes are extremely hazardous to your client’s wealth.

The four factors described above: (1) volatility, (2) proper portfolio construction, (3) fees and expenses coupled with turnover and (4) taxes can reduce your clients’ portfolios by as much as 5% annually. Here’s why. If they earn 10% on their non-qualified portfolio, but 5% is lost due to the four wealth eroders, it takes more than twice as long to accomplish the same ultimate result. That 50% reduction will have a dramatically negative impact on the portfolio.

Conclusion

Most professional advisors and brokers do not deliberately mismanage or ignore the four factors. I know this might seem like money management 101 to you. But evidence from Dalbar, Morningstar and others suggests many advisors are either ignorant of the role these four wealth eroders play or just choose to ignore them. As we’ve seen throughout the NFL season, the teams still alive in the playoffs are the ones not afraid to go back to basic blocking and tackling. It is always the fundamentals that win the day.

Dr. Guy Baker, CFP, CEPA, MBA is the founder of Wealth Teams Alliance (Irvine, CA).