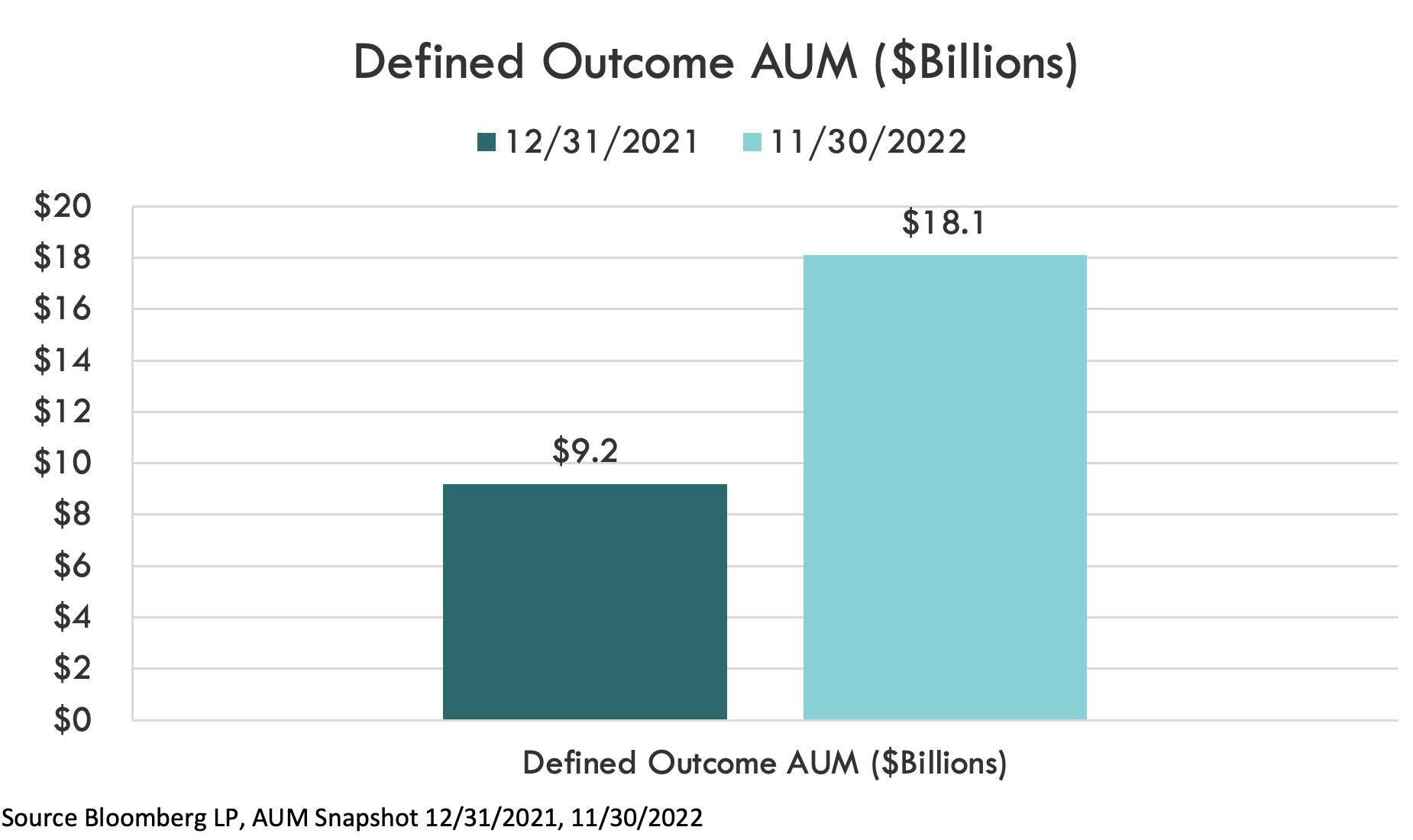

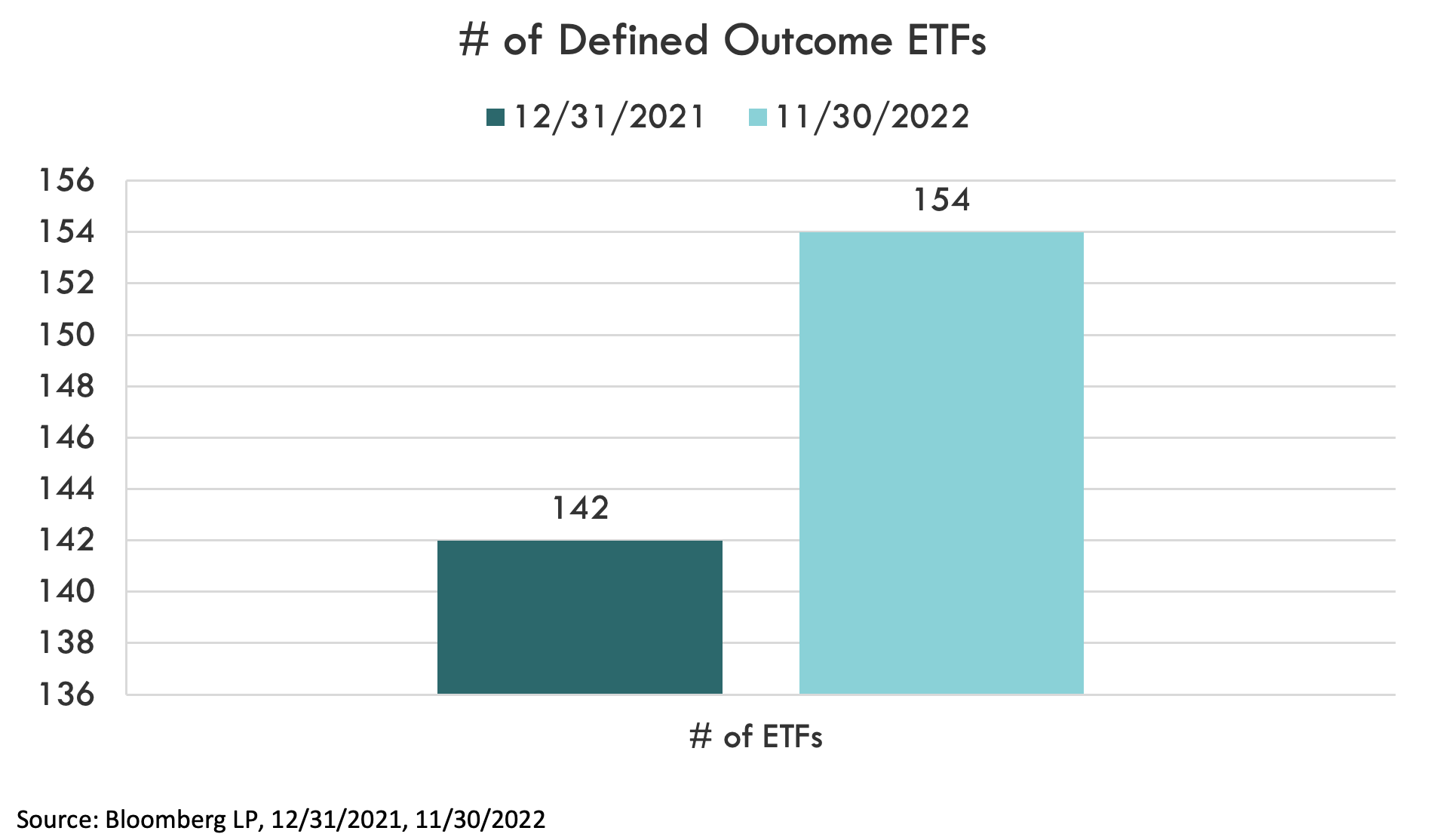

In a year when stocks and bonds both suffered deep drawdowns, one of the top investing trends of 2022 was the rapid growth of Defined Outcome” ETFs and their adoption by financial advisors. With over $9 billion in net flows through November to the roughly 150 ETFs from five fund sponsors, assets in the category nearly doubled to $18 billion. While access to the ETFs remains limited at a number of major national broker/dealers, use among registered investment advisors (RIAs) has been robust and jumped in 2022.

What Are Defined Outcome ETFs?

Defined Outcome ETFs seek to provide investors with known ranges of future investment returns prior to investing. These options-based, forward-looking investment strategies provide investors with exposure to a benchmark with a known range of upside growth potential and downside, including risk mitigation features such as a “buffer,” or a floor against loss, over a predefined period of time called the “outcome period.” Defined Outcome ETFs reset either annually or quarterly and can be held indefinitely. They are similar to legacy structured products, but the ETF wrapper provides tax-efficiency, transparency and liquidity while negating the credit risk structured products can carry.

There are a few flavors of these funds. Defined Outcome ETFs encompass Buffer ETFs, Accelerated ETFs, and Floor ETFs. Buffer ETFs, which seek to provide the upside performance of broad, liquid benchmarks (e.g., SPY, QQQ, IWM, EFA, EEM, TLT) up to a predetermined cap, with built-in buffers against loss. Strategies that absorb losses with a buffer were the first to list in 2018 and comprise the majority of the funds, assets and flows in the category.

Buffering 2022’s Bear Market Losses

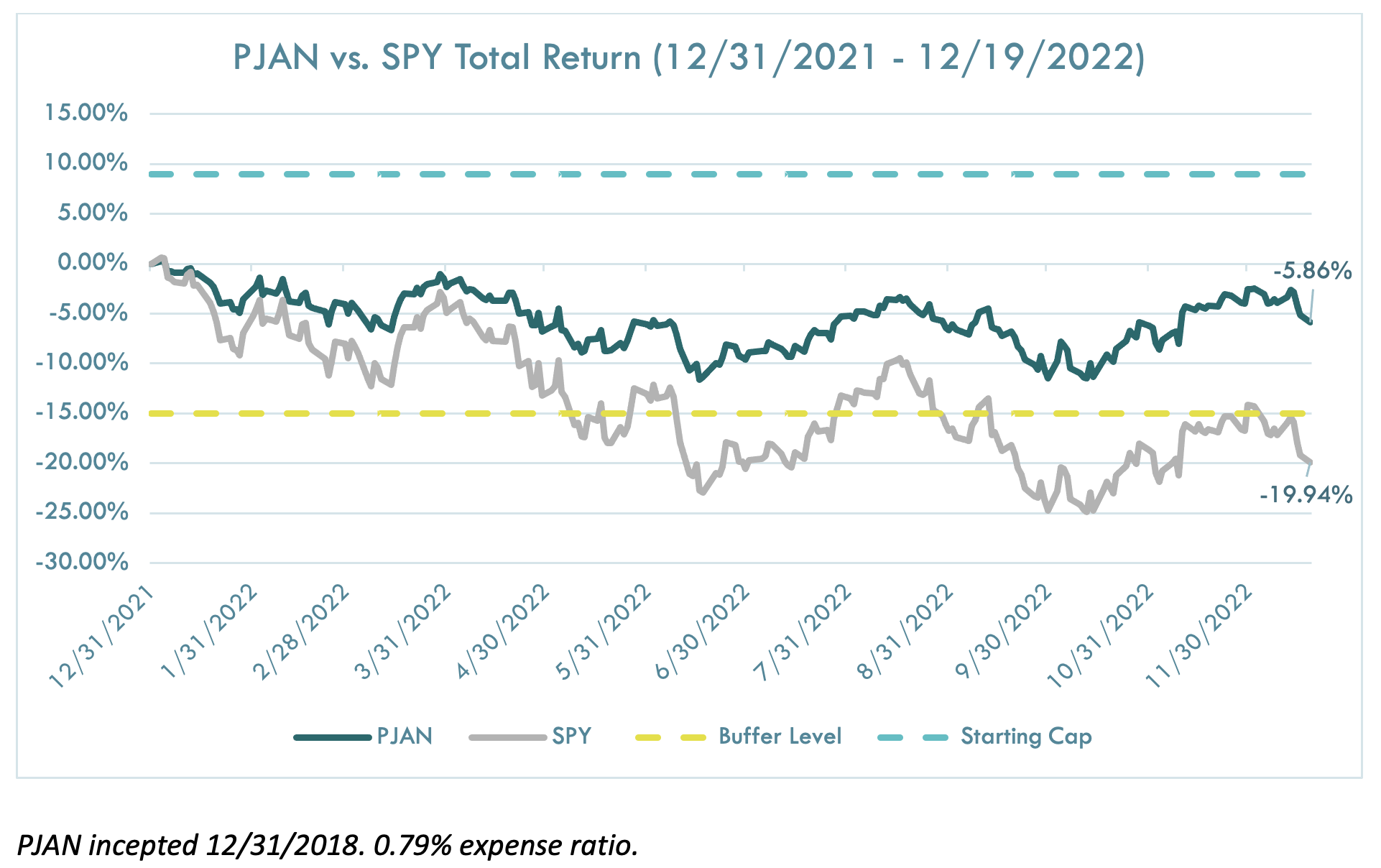

And–as 2022 showed–the attention advisors have paid to Buffer ETFs has been worthwhile. One of the largest Buffer ETFs is my firm’s US Equity Power Buffer ETF (Ticker: PJAN), which seeks to buffer the first 15% of losses in SPY over a 12-month period, gross of fees. How did it do this year? Through Monday, December 19, with less than two weeks in the fund’s outcome period remaining, SPY was down -19.94% while PJAN was down less than -6%. In fact, with most benchmarks trading significantly in the red year to date, the series of the Buffer ETFs that reset for January have shielded against market losses in their reference asset with less volatility along the way, a situation similar to the July series.

Advisor Usage of Defined Outcome ETFs

With so many potential applications, various payoff structures and benchmark exposures across more than 150 ETFs trading today, how are financial advisors using Defined Outcome ETFs? While it is common to hear from advisors that they are looking to reduce risk in client’s equity portfolios by knowing they will be buffered against a set amount of loss over a specific period of time, or that they want to maintain a lower risk profile strategy that doesn’t expose clients to interest rate risk like bond funds do, we thought a look at the data could be helpful. So, our Portfolio Solutions team reviewed their consultative work with more than 350 RIAs and 50 broker/dealers over the course of 2022 to uncover key use cases, trends and insights.

A Dedicated Buffer Sleeve

Ease of implementation is atop the list of benefits that the ETF structure brings to defined outcome investors.

Before these ETFs existed, advisors would typically either need to purchase structured products or buy and sell individual options to customize similar strategies. The ETF wrapper opens up the ability for advisors to more easily hold defined outcome strategies inside a wrap account.

According to estimates from Innovator’s Portfolio Solutions team, nearly 70% of portfolio allocations were made by taking a 10% to 30% pro rata allocation from advisors’ current models or client accounts. That range means advisors are seeing Defined Outcome ETFs as a significant component of client portfolios. The core nature of the ETFs’ exposures mean that advisors can substitute portions of their top portfolio allocations with these Defined Outcome ETFs to form a dedicated sleeve within their clients’ portfolios.

Of those SMA allocations, roughly 20% of advisors requested that their portfolio be optimized to minimize risk given a desired return target. Indeed, the ability to target a certain risk level relative to the market–one that is more aligned with a client’s risk tolerance, for instance–is another advantage that many advisors benefited from in 2022.

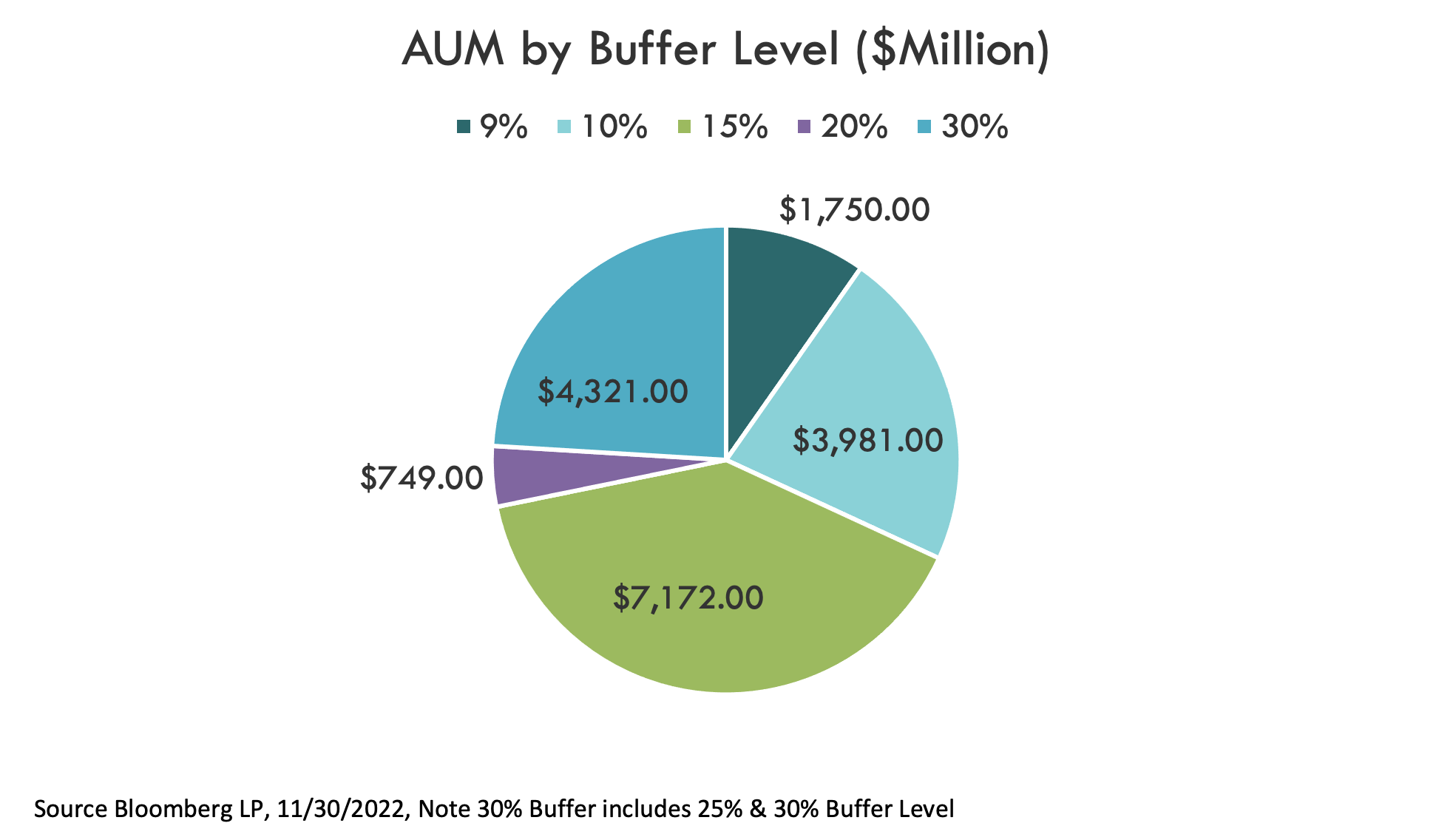

15% Buffer Was the Sweet Spot

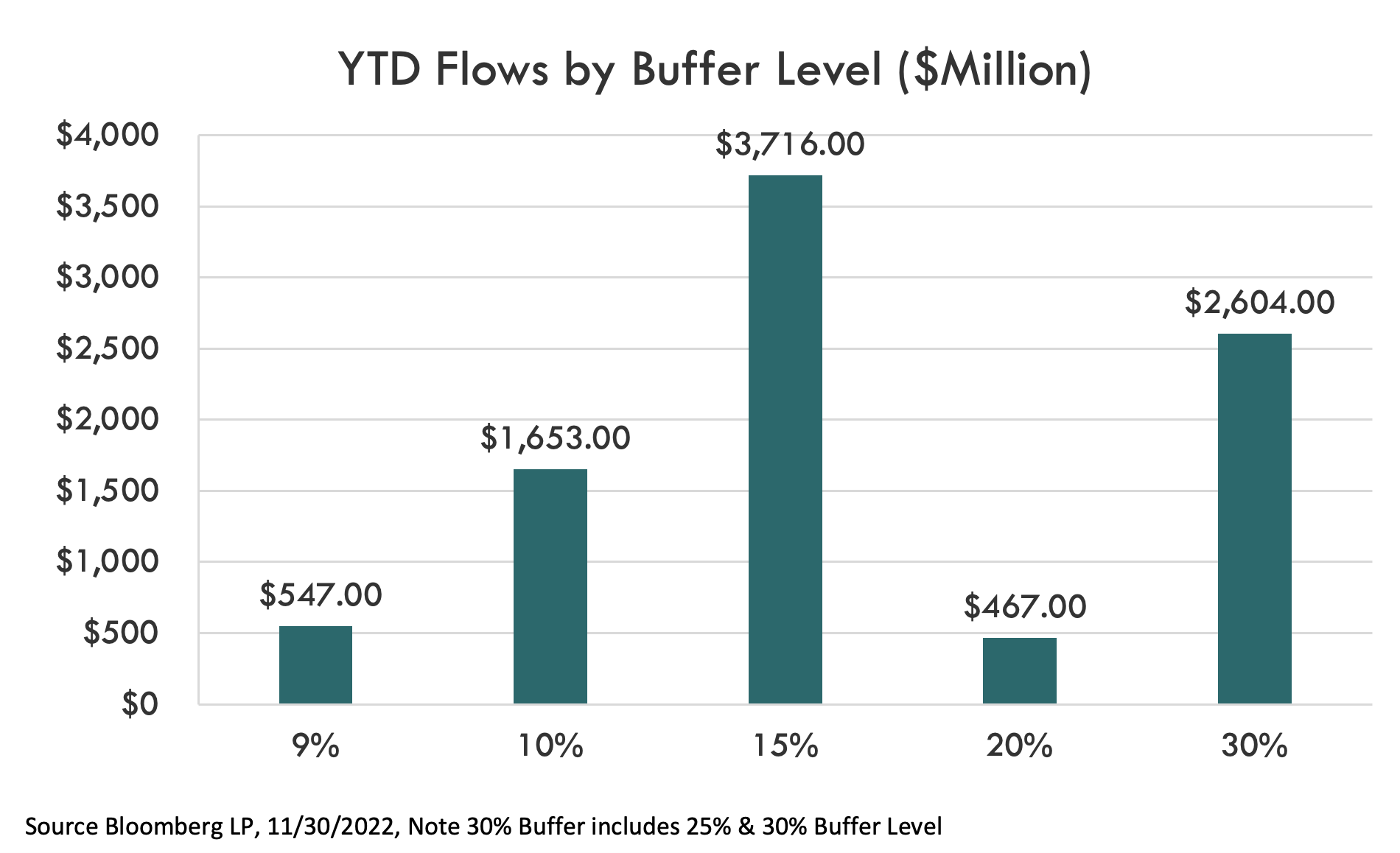

$3.7B, or 41% of all 2022 Defined Outcome ETF industry net inflows, went into strategies that buffer against the first 15% of losses in a given reference asset. One potential reason for the outsized flows is that the 15% Buffer consistently saw trades funded from both the equity and the fixed income side of an advisor’s book. Our Portfolio Solutions team estimates that 75% of all advisor requests included an allocation to Innovator’s 15% Power Buffer Series, with funding split evenly between current equity and fixed income allocations. Other Buffer levels saw more concentrated applications; the 9% buffer allocations were primarily funded from advisors’ equity allocations, while the 30% annual “Ultra Buffer” allocations and the 20% quarterly buffer strategy were mainly funded from advisors’ bond allocations.

Using a Conservative Buffer Strategy to Equitize Cash, Bonds and Liquidity Buckets

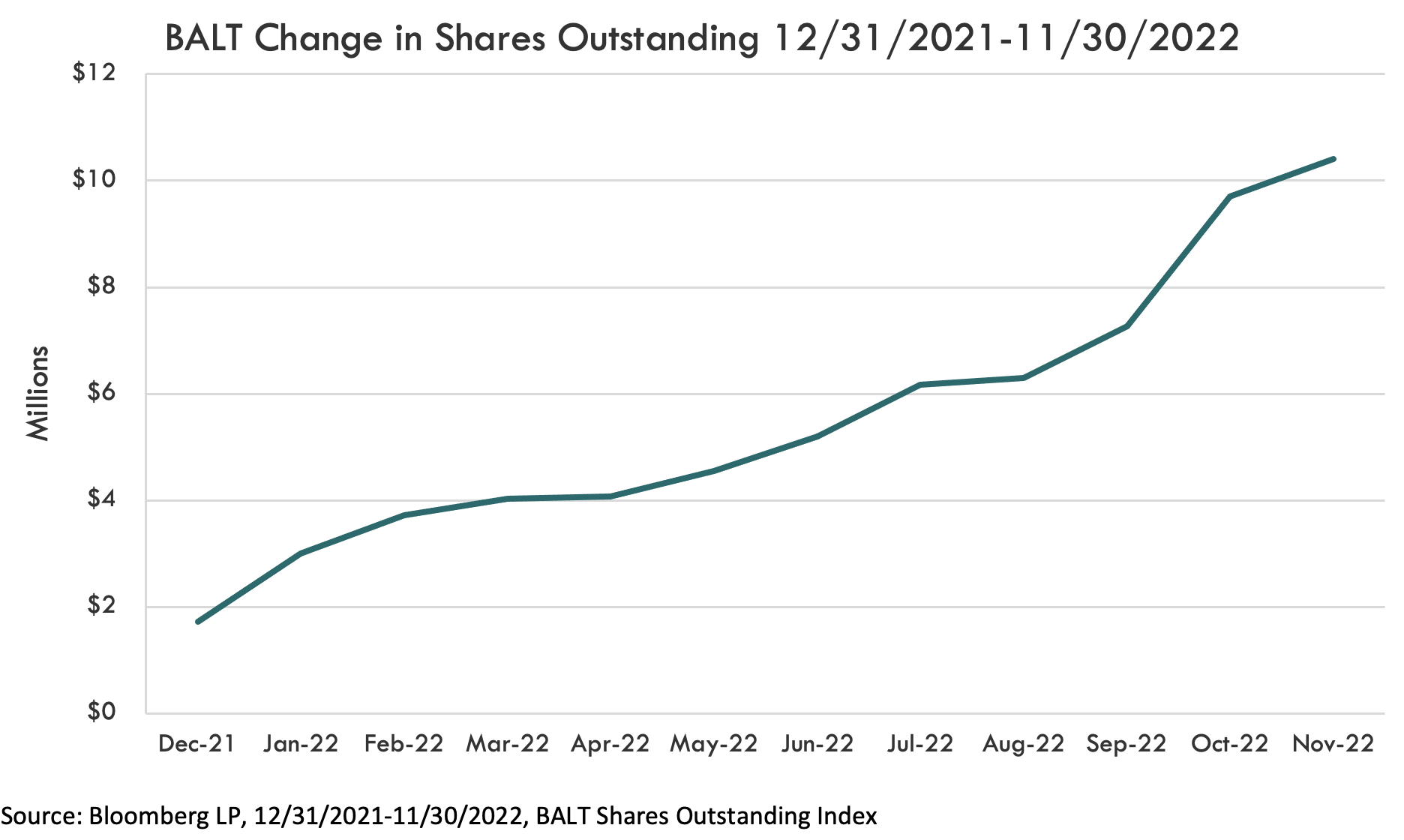

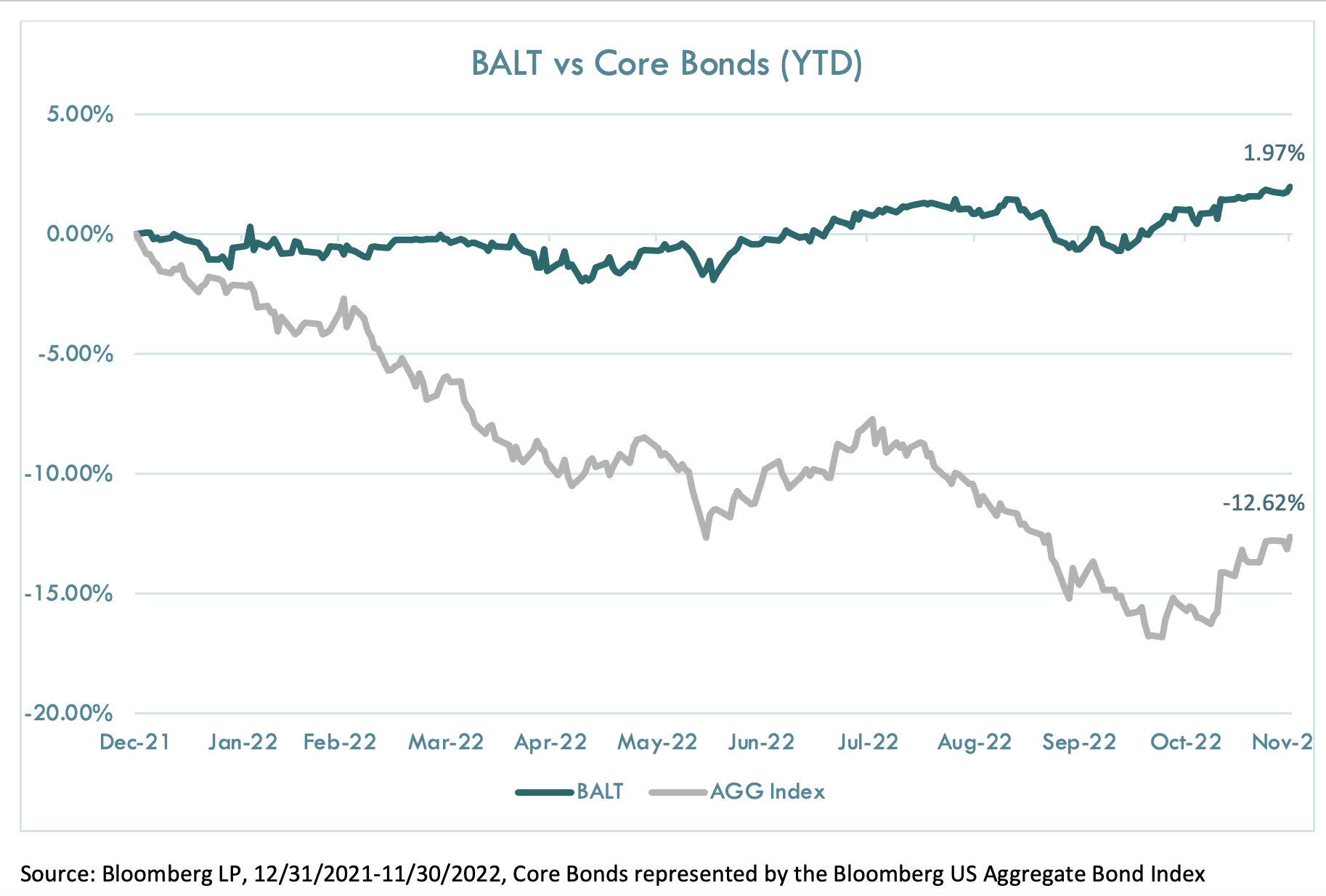

A defined outcome strategy with a very conservative risk profile that seeks to buffer quarterly losses in SPY while providing a measure of U.S. equity upside, grew rapidly in 2022. Shares outstanding in the Innovator Defined Wealth Shield ETF (Ticker: BALT), increased 503% through the end of November. Advisors frequently used BALT to complement or replace core bond positions, given the defensive nature of the 20% quarterly buffer. Other advisors used BALT to help clients get excess cash off the sidelines and into the equity market. Both strategies proved advantageous; with U.S. Large-Cap equities down -13% and the Bloomberg US Aggregate Bond Index losing nearly -12.5%, BALT produced a positive total return of 2% through the end of November.

Buffered-Only Models and Client Prospecting

A smaller percentage of firms chose to build out stand-alone Defined Outcome ETF models (< 5% of Portfolio Solutions cases). The clients that did, however, tended to be larger RIAs with average AUM over $2B. Many of these large RIAs were looking to compete for structured note business that otherwise would leave the firm. Others were simply looking for a more conservative portfolio that could narrow the range of potential outcomes for clients and prospects and potentially better align with clients’ risk tolerance levels.

Additionally, a large number of advisors also sought to position Defined Outcome ETF strategies as a competitive advantage to working with their practice in instances where a prospect had not yet signed on to the firm, but were displeased with their current portfolio’s performance or felt their portfolio was excessively risky. While data was not specifically captured on this side, there were many such anecdotes in 2022 as the dual drawdowns in equities and bonds challenged many traditional portfolios.

What Trends Will Emerge in 2023?

With many of the economic and market-related challenges largely unresolved heading into the new year (e.g., inflation, the path of rates, earnings), we believe uncertainty is extremely high. As such, volatility could remain elevated with markets choppy, and many of the Defined Outcome ETF trends witnessed in 2022, such as the popularity of Buffer ETFs, will continue into 2023. With about 10,000 Americans hitting retirement age each day currently, too many savers have just been hit by a textbook example of sequence of returns risk, and advisors who viewed bonds as portfolio ballasts are looking for alternatives.

Should market risks and volatility begin to dissipate, we anticipate growth of Accelerated ETFs, which seek to provide a multiple of the return of a given market, to a cap, to pick up. Regardless, as thousands of wealth management firms have discovered, implementing Defined Outcome ETFs into an advisory practice can not only blunt the impact of drawdowns, it can aid client discussions about return expectations and risk tolerance levels. The differentiation and personalization that demonstrates should continue to benefit advisors no matter the market climate.

Tim Urbanowicz, CFA, is head of research and investment strategy at Wheaton, Ill.–based Innovator ETFs, the pioneer of Defined Outcome ETFs.