Wednesday’s broad equity selloff was roundly attributed to news out of Washington. Certainly the political vortex swirling about the White House stoked fears, but there’s been an anxious undercurrent in our sea of stocks for months. Our last Market’s Measure column highlighted two indicators that signaled a nagging erosion in investor’s appetite for risk, despite the market’s rise to record highs.

So now what? Is the bull market at long last dead?

Let’s not get ahead of ourselves. Wednesday’s action was a cyclical pullback. There have been plenty of backsteps taken during the bull’s current run — some big, some small. This slip has the makings for something on the bigger side. Take a look at the chart below.

As this is written, the S&P 500 is churning at the 2,370 level. If the April lows at 2,340 are breached, a downside objective at 2,280 comes into sight. That’s a 5 percent decline from the double top at the 2,400 level. That drop would wipe out three months’ work on the upside but wouldn’t represent the death of the bull market.

And if the April lows don’t hold? There’s major support at the December 2016 lows around 2,190 - 2,195. A skid to that level would be pretty scary, but it still wouldn’t signal the start of a bear market.

Markets are commonly believed to turn bearish after a 20 percent drop within a two-month period.

By that metric, the S&P 500 would need to sink to 1,920 by mid-summer to start growling.

Possible? Sure. Probable? At this point, not really. The long-term uptrend is still intact and still points to an objective at 2,524 or so.

Without a doubt, this bull market, at 97 months, is old. Though creaky, it’s not the oldest bull we’ve seen in the post-war era. That credit goes to the 113-month upsurge between the fall of 1990 and the spring of 2000. And we all know what happened to that market, right? The dot-bomb ultimately exploded, preceded by a great deal of volatility.

We’re seeing volatility returning to the current market after scraping bottom for months. It’s a safe bet that volatility will be a market feature in the future. After all, no bull market has lived to see its tenth birthday.

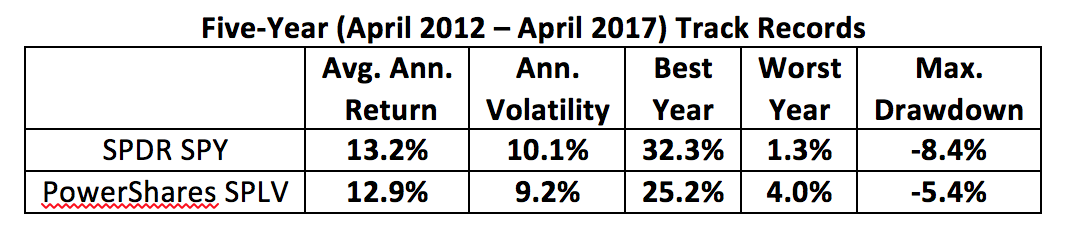

Looking forward, investors seeking to maintain equity exposure may be driven to low volatility plays like the PowerShares S&P 500 Low Volatility ETF (NYSE Arca: SPLV), a portfolio that tracks 100 of the S&P 500’s least volatile issues.

And why not? On Tuesday, SPLV suffered a modest 0.5 percent loss, compared to the 1.9 percent hit taken by the SPDR S&P 500 ETF (NYSE Arca: SPY). In the long run, taking the low-vol approach doesn’t cost much in returns and goes a long way in saving investors from stress.

Brad Zigler is WealthManagement's Alternative Investments Editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.