There’s been a whole lot of noise made about strategic or smart beta in the past few years. Strategic beta represents a sort of middle ground between passive and active investing, and it seems a perfect niche for exchange traded funds. Usually, strategic beta ETFs employ a transparent, if mechanistic, methodology designed to exploit some factor or inefficiency. Their goal, like actively managed portfolios, is to outperform the benchmark, but at a much lower cost than active products.

The simplest way to obtain some excess return is to strategically reweight the market benchmark. Let’s take a look at a couple of riffs on the venerable S&P 500 Index.

The best-known version of an ETF tracking the index itself is the SPDR S&P 500 ETF (NYSE Arca: SPY). SPY’s the grand-daddy of all ETFs and hews closely to its underlying index. Its 500-stock portfolio is weighted by capitalization and costs just 9 basis points (0.09 percent) a year.

Other ETFs contain the same 500 stocks as SPY, but weight them differently. The Guggenheim S&P 500 Equal Weight ETF (NYSE Arca: RSP), as its name implies, assigns equal weight to each issue, giving full voice to the smaller companies in the index. Holding RSP will cost you 20 bps a year. For 39 bps, the Oppenheimer Large Cap Revenue ETF (NYSE Amex: RWL) takes the S&P 500 and reweights each stock by its company’s revenue.

You’d expect these alternative weighting schemes to yield different performance characteristics. And you’d be right. But the differences seem fairly subtle, at least on the surface.

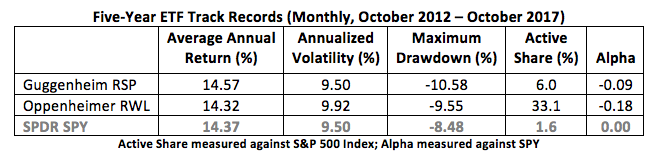

When considering these alternative weighted portfolios, one has to ask if the differential results justify their higher costs. Looking back over the past five years, you’d be hard pressed to say yes.

Five-Year ETF Track Records (Daily, October 2012 – October 2017)

What’s evident from the daily chart of normalized closing prices is that alternatively weighted versions of the S&P 500 portfolio outperformed the capitalization-weighted index fund. Drawdowns, however, tended to be deeper for the alternative funds. That extra volatility drags RSP’s and RWL’s Sharpe ratio below SPY’s. That’s reflected in the alternative funds’ negative alpha coefficients, though expense ratios also figure into that number.

What’s most notable from the table are the differences in the funds’ active shares. Active share measures the difference in a fund’s holdings versus the benchmark. Since all the S&P funds hold the same stocks as the index, any active share must be attributable to the overweights or underweights relative to the benchmark.

Fully 94 percent of RSP’s holdings are identical to the S&P 500, while only two thirds of the RWL mirrors the index. Clearly, RSP gets more bang out of its reweighting than RWL.

To see how, you need to do some factor-diving.

Over the past five years, SPY’s returns have been driven primarily by momentum. That’s mostly an artifact of its capitalization weighting scheme. RSP, on the other hand, is a low-momentum play because each of its issues is equal-weighted regardless of its popularity. The sometimes-dramatic reweighting of RSP’s components also makes its portfolio more volatile than the benchmark.

Like RSP, RWC is a low-momentum portfolio, but instead of being driven by volatility, the Oppenheimer ETF is powered by value. Given the fund’s revenue weighting scheme, this should not come as a surprise.

So, which of the two—RSP or RWL—is the better riff on the S&P 500 Index? Well, if we take each fund’s excess average annual return (earned over SPY’s) and divide it by its expense ratio, we can readily determine each portfolio’s cost efficiency. RSP, with a factor of 1.00 (20 bps divided by 20 bps), plainly comes out on top. RWL’s factor is -0.13.

Will RSP continue to outperform in the future? One can’t say with certainty, but RSP’s lower-cost structure gives it a decided edge.

Brad Zigler is WealthManagement’s Alternative Investments Editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange’s (now NYSE Arca) option market and the iShares complex of exchange traded funds.