The economics of oil are changing. At long last, there’s a bid under the price of West Texas Intermediate (WTI), the U.S. benchmark crude grade. You can see that in the double bottom scribed at the $26 level earlier this year. Since the last test of support in February, WTI’s risen to toy with a $40 print.

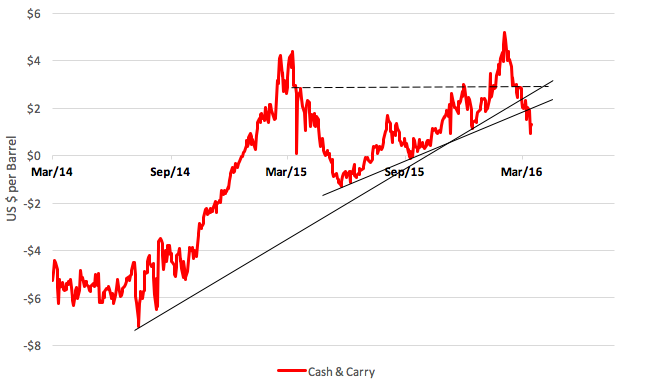

Odds favor the upside here. Why? Well, for one thing, the margins on so-called “cash-and-carry” operations—money makers for big oil traders lo these many months—are plummeting. The play entails the purchase and storage of spot oil cargoes and selling futures contracts to lock in sale prices.

A trader who bought, for example, 10,000 barrels of crude a month ago for $32 a pop could have contracted to offload the cargo in May for $36 a barrel by simultaneously selling 10 Nymex WTI futures. Our trader would be obliged to pay storage fees for the three-month holding period as well as any financing costs, but would be insulated from any intervening oil price risk. Once the crude is delivered and the carrying costs netted out, our trader would have made a tidy 10 percent profit. Lather, rinse and repeat, and you can see that a couple or four operations in a year can add up to some terrific per-annum returns.

Those happy days may be over if the chart below plays out.

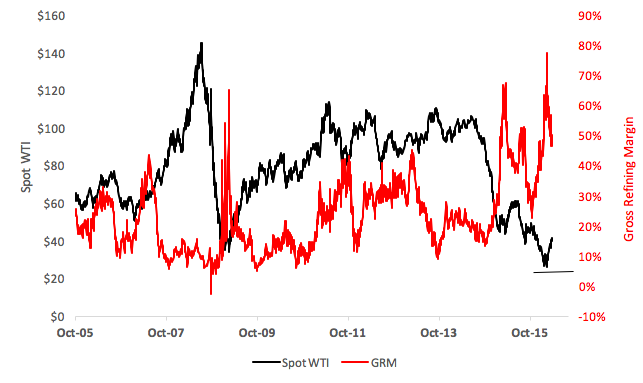

The bottoming in WTI prices has also been accompanied by an increase in short-term financing rates and shrinkage in gross refining margins (GRMs). GRMs represent the profit available to refiners for selling distillates such as gasoline and diesel fuel after paying for crude oil inputs. Precipitous changes in crude prices tend to be inversely related to shifts in GRMs. Generally, when crude prices jump, profit margins fall; GRMs spike higher when oil prices tumble.

The current buoyancy in oil prices seems to have some legs. There’s seasonality at work, which bodes well for ETFs such as the United States Oil Fund (NYSE Arca: USO) and its sibling, the United States 12 Month Oil Fund (NYSE Arca: USL). Both track WTI futures prices but in slightly different ways.

Odds are better than even for the contango-resistant USL fund to finish April above its current $16.50 level. Near-term technicals point to a $19 objective. A $23 target is painted by the longer-term chart, a level not seen since the summer of 2015.

All told, this season’s mantra for oil punters seems to be “Buy for July.”

Brad Zigler is REP./WealthManagement’s Alternative Investments Editor. Previously, he was the head of marketing, research and education for the Pacific Exchange’s (now NYSE Arca) option market and the iShares complex of exchange traded funds.