It’s never easy finding a reliable source of positive alpha. In a Darwinian sense, that’s as it should be. If we all snagged good numbers, who’d be left to pocket the bad ones?

For a long time, a search for alpha among exchange traded funds always returned the ticker symbol TTFS. Originally launched in 2011 as the AdvisorShares TrimTabs Float Shrink ETF (TTFS), the actively managed TTFS portfolio sought to outdo the Russell 3000 by trading on three trends— decreasing share floats (read: buybacks), increasing cash flows and shrinking debt ratios.

TTFS plied the alpha waters well under the AdvisorShares banner until mid-2016 when the sub-advisor, TrimTabs Asset Management, was dumped in favor of Wilshire Funds Management and rebranded as the AdvisorShares Wilshire Buyback ETF. The fund’s ticker symbol was retained and, as a result, so was its sterling track record. That record includes an annualized alpha of 0.63 over its lifetime.

So what was the reason for the switch? Well, nobody’s really talking about that but there’s one tell: At the switchover, the ETF’s management fee dropped by 10 basis points.

On the surface, TTFS seems to be following the same mandate under Wilshire as it did under TrimTabs. But if you dig a little bit deeper, you’ll see TTFS is losing its luster. It turns out that TrimTabs had the magic alpha touch. Wilshire doesn’t.

We know that because the TrimTabs folks went out and recreated their TrimTabs Float Shrink ETF under their own banner. Now named the TrimTabs All Cap US Free-Cash-Flow ETF (BATS: TTAC), the fund recently celebrated its one-year anniversary, still too young for its track record to be publicly analyzed in depth by the likes of Morningstar but not for us.

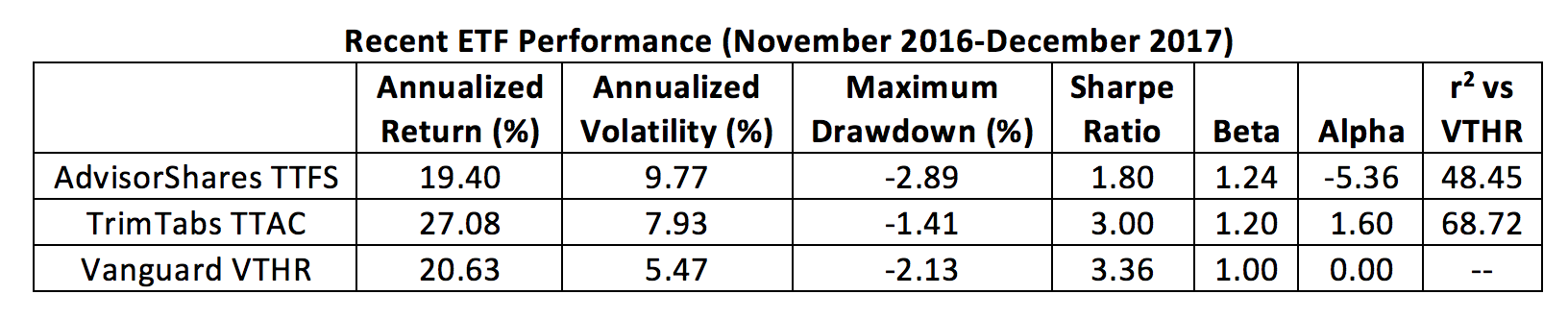

When we compared TTAC’s recent performance to TTFS and to the Vanguard Russell 3000 ETF (Nasdaq: VTHR) benchmark portfolio, we tracked down the real alpha producer.

Growth of $10,000

TTAC’s pièce de résistance is the production of positive alpha while being more closely correlated to the benchmark than TTFS. That means TrimTab’s bets are more efficient. TrimTabs doesn’t have to take broad excursions from the benchmark strategem to find outsized returns.

TTFS has a value tilt with more than half of its portfolio weight given over to mid-cap stocks. The AdvisorShares portfolio’s largest exposure is to financial services. TTAC, on the other hand, leans on the small stock premium, giving its greatest weight to the technology sector.

Most important for investors, though, is the cost to hold the ETF. Now that the TrimTabs portfolio is self-managed, it’s offered at a 59 basis point expense ratio. That’s not a bad price for alpha. In fact, that seems to be real value for the money.

Brad Zigler is WealthManagement’s Alternative Investments Editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange’s (now NYSE Arca) option market and the iShares complex of exchange traded funds.