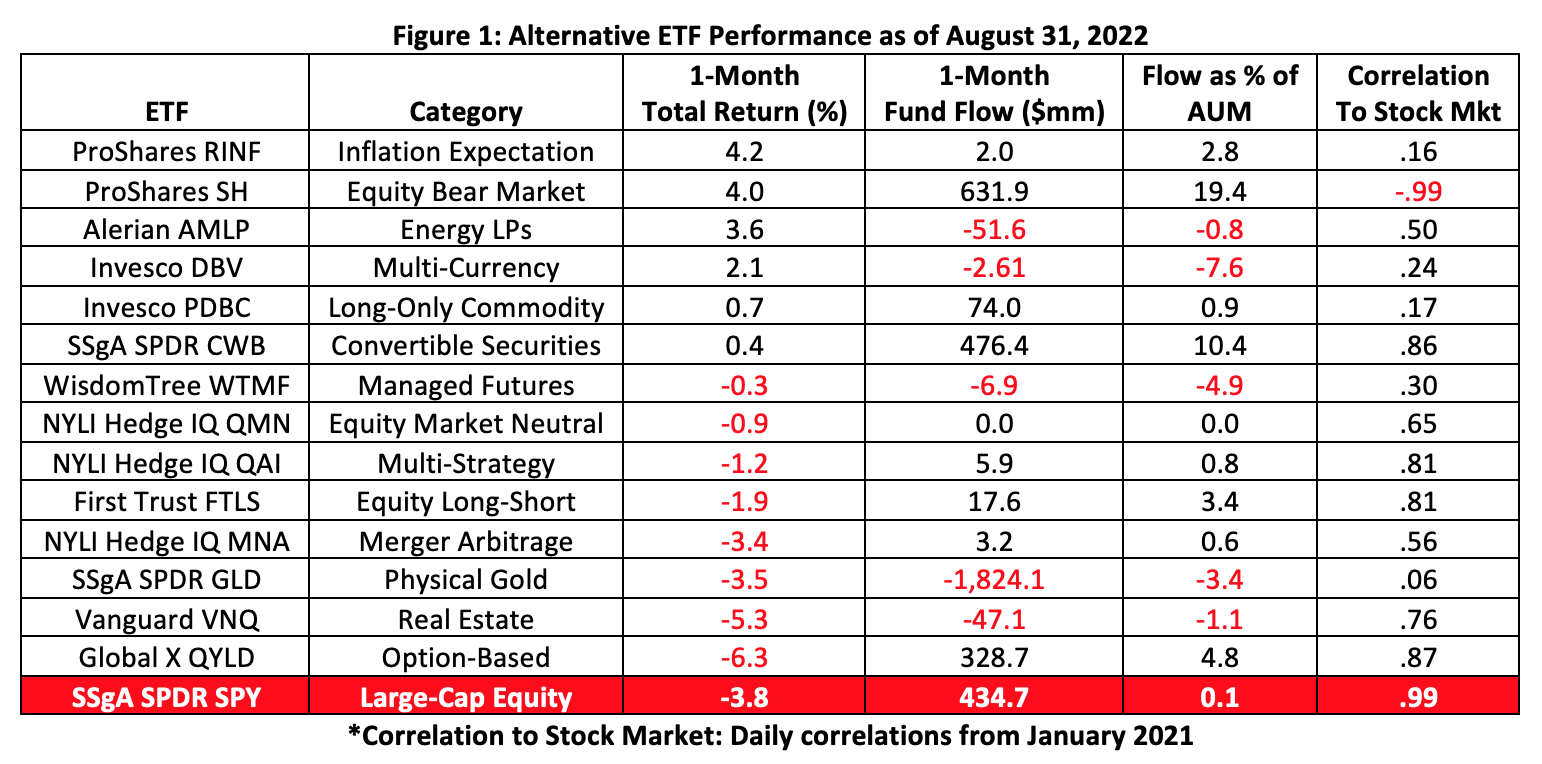

Last month wasn’t great for the stock market. For alternative ETFs, results were mixed. Of the 14 category benchmark funds we follow, nearly half cranked out gains in August. The average gain was 2.5% while losers clocked in with a mean 2.9% loss.

At the top of the table was a rebounding ProShares Inflation Expectations ETF (RINF).

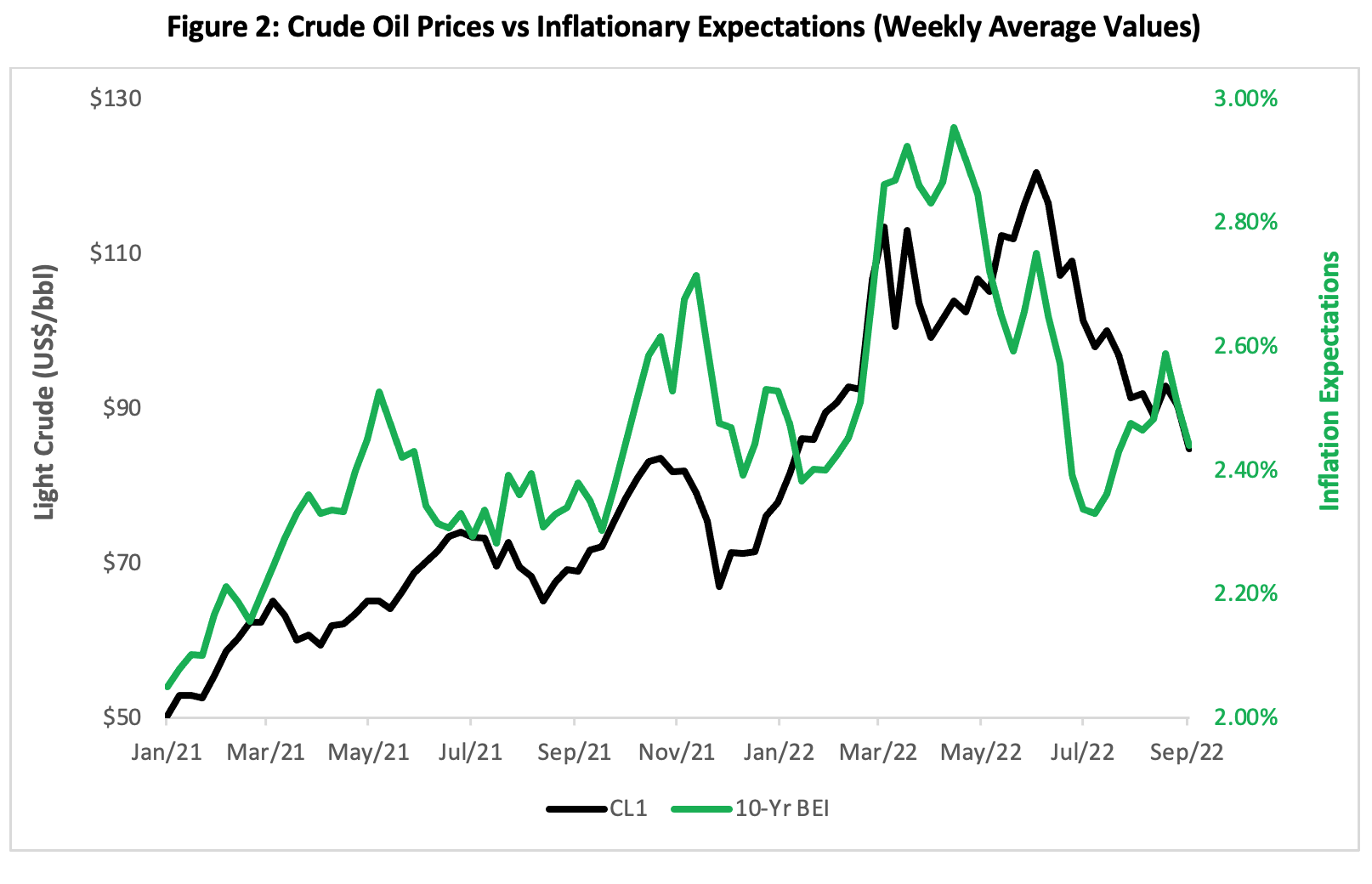

No surprise in that, really. Inflation talk has been rampant, though there are signs of price moderation, especially in the energy sector. Witness the correlation between the 10-year breakeven inflation (BEI) rate--a proxy for inflation expectations--and the front-month light crude oil (CL1) contract in Figure 2.

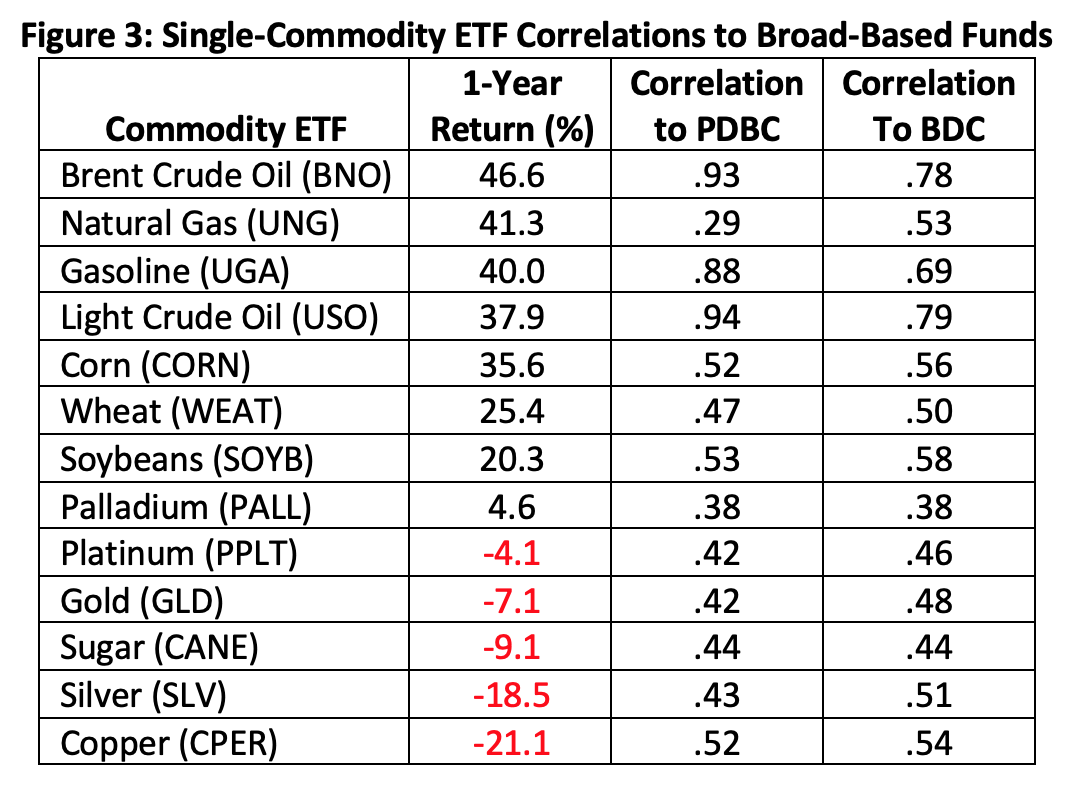

It’s apparent that a lot of inflation expectations are driven by energy prices and perhaps more modestly, by the costs of basic foodstuffs. Evidence of this can be seen in the daily correlations of single-commodity ETFs to the past year’s best performing broad-based futures funds.

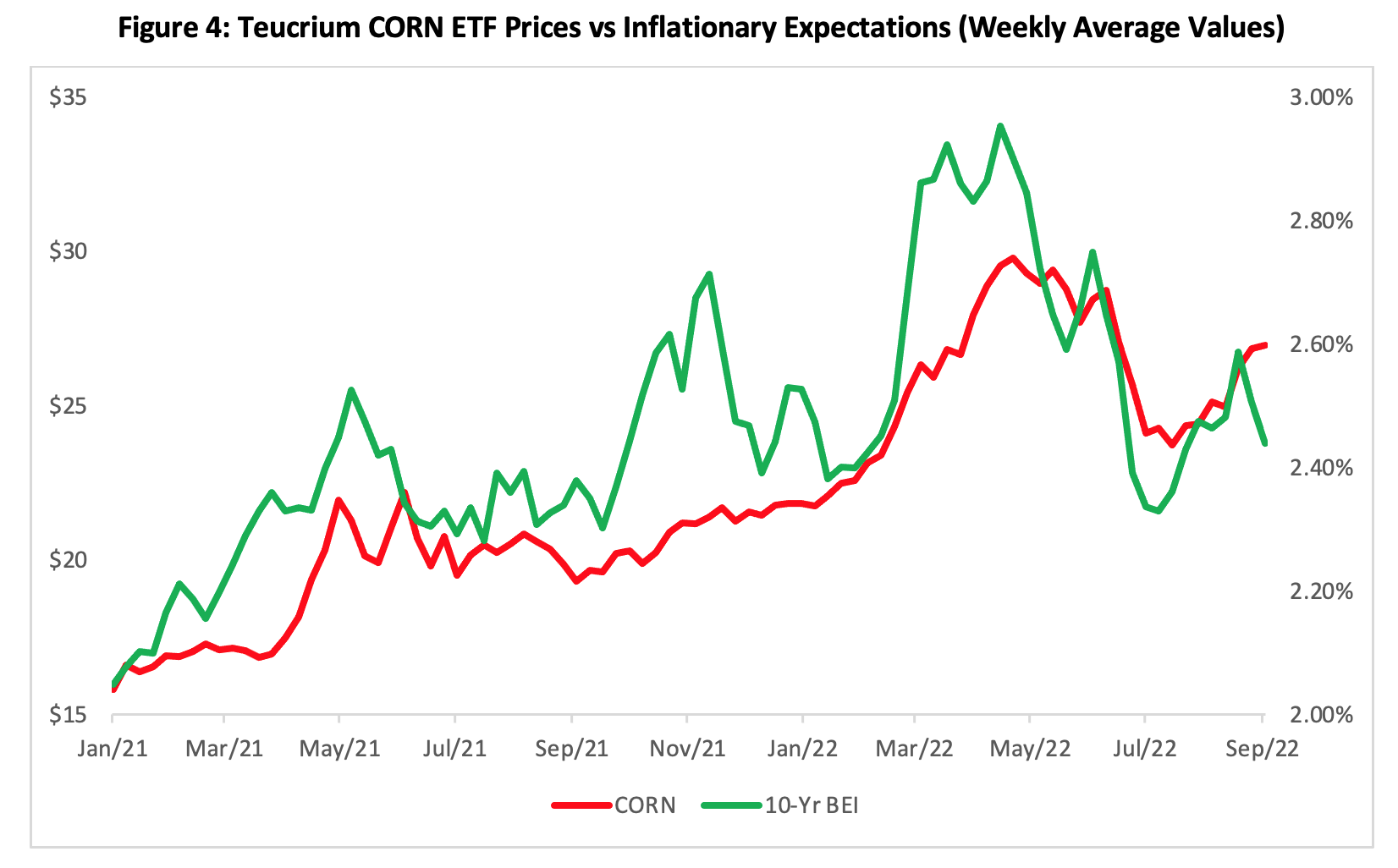

Inflation expectations are also linked tightly to agricultural prices, most particularly corn, the most ubiquitous grain in the food chain. Figure 4 shows how inflation expectations tracked the value of corn proxied by the Teucrium Corn Fund (CORN), a portfolio that optimizes its exposure to the corn futures market.

We examined the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC) earlier this year, comparing it to other broad-based commodity funds, including its sibling, the Invesco DB Commodity Index Tracking Fund (DBC). PDBC’s and DBC’s portfolios are essentially identical, though the former is tagged as an active fund. Both portfolios are composed of 14 futures contracts spread across the energy, precious metals, agricultural and industrial metal sectors. Presently, PDBC devotes over 60% of its real estate to energy futures with light crude comprising nearly 13% of the fund’s total commodity exposure. PDBC’s second heftiest sector--at 15%--includes the grain contracts, evenly split among corn, soybeans and wheat.

PDBC produced a modest gain in August even as oil prices continued their slide from their June highs.

Unlike PDBC, the abrdn Bloomberg All Commodity Longer Dated Strategy K-1 Free ETF (BCD) doesn’t rely solely on commodity prices for its gains and losses. It’s an index tracker but it has an active overlay.

BCD’s futures portfolio currently consists of 23 commodities. Energy contracts make up 30% of the portfolio with light crude oil accounting for 8% of the total commodity exposure alone. Grains comprise 23% of the total allocated weight, with corn and soybean each accounting for 6% of its heft.

The collateral used to secure the BCDs futures positions is actively managed to optimize appreciation and yields. That, together with the fund’s unique roll strategy, contributed to the fund’s outsized 1.8% August gain.

Robust exposure to energy and grains in the PDBC and BCD portfolios has made these two funds well-suited as inflation hedges in the current environment. But the nature of that exposure magnifies the funds’ utility, particularly with respect to crude oil.

A condition known as backwardation, or inversion, has characterized the crude oil market since January 2021, reflecting tightness in supply.

For storable commodities, normalcy exists when supplies are ample, meaning there’s enough to not only satisfy current demand but also enough to store for future delivery. Storage costs money, so a normal market’s delivery curve features higher and higher prices as you move to the outer months. The oil market vacillates between this condition, known as contango, and inversion as supply and demand ebb and flow.

Investors in commodity futures funds are keenly aware of contango’s and inversion’s impact on their returns. To maintain a long position in a commodity, futures contracts must be rolled forward before their delivery dates. A roll simply entails the sale of the expiring contract and the simultaneous purchase of a longer-term future. Rolling forward proves costly when the market’s in contango because the lower-priced nearby contract is sold to fund the purchase of the higher-priced distant delivery. A premium, however, is obtained when the market inverts. In backwardation, the high-priced nearby futures is sold then as the low-priced deferred delivery is bought.

Since the crude oil market inverted last year, the three-month premium has ranged from a per-barrel low of 6 cents to a high of $13.02. Backwardation peaked in the immediate aftermath of Russia’s invasion of Ukraine but has been waning ever since. Presently, the three-month spread averages $1.60 per barrel.

The question for investors and advisors going forward is this: Will tight supplies keep the market inverted and buoy front-month energy prices, or will an economic downturn flip the market into contango? A return to a normal energy market could prove to be a double whammy for unwary inflation hedgers.

Brad Zigler is WealthManagement's Alternative Investments Editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.