In 1992, I remember thinking: compact discs are here to stay. They sound great; they’re more durable than records, 8-tracks or cassette tapes, and they’re vastly easier to store and carry around. With CDs, we could skip and repeat tracks easily, and when multidisc players became the norm, the music never stopped. The real beauty of the CD, though, was its medium—a beautiful, binary code that could store a huge amount of data, a whopping 700 megabytes of the highest quality recordings we had ever heard.

Tragically, the very essence of the CD was the thing that led to its downfall: the invention of digital music. As innovators quickly learned, digitization lent itself easily to transference and conversion, and ta-da! The MP3 was born, and CDs went the way of the dinosaurs.

Modern Portfolio Theory has suffered a similar fate: what began as a groundbreaking tool for investors has fallen prey to the subsequent innovations born out of the original theory. The key tenets of the theory are “diversification” and “correlation”—a well-diversified portfolio constructed of lowly-correlated assets will provide higher returns without a commensurate amount of risk. While the basic tenets of MPT hold true, its present-day application often results in the construction of over-complicated and needlessly over-diversified portfolios.

In 1952, when economist Harry Markowitz first wrote about Modern Portfolio Theory, the investing world was a different place: only 4% of Americans owned stocks, and the value of marketable Treasury debt was approximately $142 billion. In 1954, when the Dow Jones Industrial Average finally regained its pre-Depression peak, only about 100 mutual funds were in existence. By contrast, today nearly 60% of Americans own stocks, marketable Treasury debt is over $23 trillion, and investors have over 125,000 mutual funds and 7,600 exchange-traded funds from which to choose.

At the birth of MPT, diversification was a narrow concept given the relatively limited investment options available to the public, comprising primarily large-cap domestic stocks, government bonds and corporate bonds (and mutual funds that held stocks and bonds). While stock-bond correlations have swung broadly throughout history from negative to positive, the degree of risk—return variance—has largely been more reliable: stocks are riskier and have a higher standard deviation; bonds are less risky and have a lower standard deviation. Markowitz’s objective of achieving “lower volatility” hinged on the optimal combination of these risky and less-risky assets working in tandem.

Over the last several decades, as the investment advisory industry adopted prudent investor standards that demanded “diversification,” and as access increased to a myriad of investment vehicles, portfolios have come to resemble less and less how a “modern portfolio” may have looked in 1952. Instead, today’s portfolio has become a “chiclet chart:” an account that holds not only broad asset classes but also every flavor and color of sub-asset class in addition to vehicles that provide access to real assets such as commodities, real estate and gold.

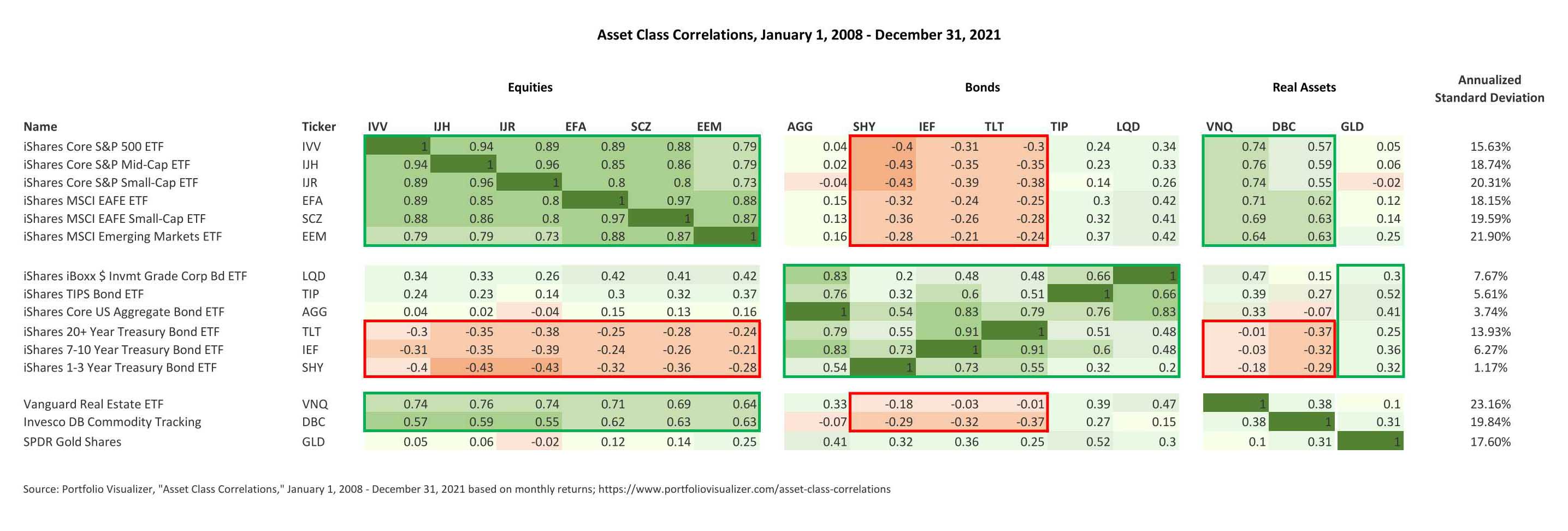

The chart below illustrates relative correlations from 2008 through 2021 for popular ETFs that represent both broad asset classes and sub-asset classes. The chart sorts the ETFs in descending order of correlation to the iShares Core S&P 500 ETF (IVV). Areas of strong positive correlation are shaded and boxed in green, and areas of relatively negative correlations are shaded and boxed in red. From this, several observations become clear:

- Equity index ETFs across geographies and capitalizations are strongly correlated to the S&P 500 (coefficients greater than 0.70) and do not provide meaningful return variance diversification from large cap U.S. stocks (e.g. the S&P 500 index ETF);

- Real estate and commodities are moderately to strongly correlated to the S&P 500 while gold ranges from near-zero correlation to only modest correlation across all asset classes; and

- Treasuries offer the greatest degree of negative correlation to equities as well as to real estate and commodities while investment grade corporates and TIPS are positively correlated to large cap US stocks.

The principal conclusion from these observations is that today’s staggering array of investment options provides a false sense of meaningful diversification. Beyond correlations, investors will also find that among broad asset classes, sub-asset classes typically offer a narrow range of risk exposure (i.e. standard deviation).

Today’s truly modern investor would be best served by segregating accounts by purpose and allocating to those accounts the asset classes whose return and risk characteristics reflect the respective objectives. An MPT-driven portfolio may be most appropriate for investors seeking some combination of lower volatility, current income and long-term appreciation in a single account. That said and regardless of the objective of a specific portfolio, selecting high-quality securities within the chosen asset classes will position investors to retain the potential for outperformance while reducing the needless complications of an over-diversified, beta-yielding portfolio.

Jonathan Justice is a Managing Director, Senior Advisor at Chilton Trust