Ask market prognosticators about the recent market rout and prospects for 2016, you will hear a lot about volatility. A recent Barron’s Striking Price column warned investors that “stocks will do about as well in 2016 as they did in 2015, but with more frequent price swings,” citing central bank actions here and abroad, a shallower option market and lower corporate profit margins as contributors to more market oscillations in the year ahead.

Société Générale strategist Larry McDonald pointed to weak oil prices when he advised investors to “get long volatility.”

And, in a note to clients, Morgan Stanley stock strategist Adam Parker broadly exclaimed “we are likely headed for a choppy year of low returns, and suspect many others think the same.”

Volatility isn’t good for stock returns. You can see its deleterious effect especially displayed in the wake of drawdowns. A drawdown is a peak-to-trough decline in an investment’s value. A stock that topples from $100 to $80 before starting to recover suffered a 20 percent drawdown. That’s bad news certainly, but what’s worse is this: It takes more than a 20 percent gain to get back to even. To reach $100, an $80 stock must, in fact, rise 25 percent. After a 30 percent drawdown, a 43 percent move is required to recover lost ground. And on it goes. Big drawdowns need even bigger recoveries.

2016 looks to be studded with drawdowns, making it a banner year for low-volatility plays. And that’s good news for manufacturers of certain exchange traded funds (ETFs).

Large-Cap, Low Vol

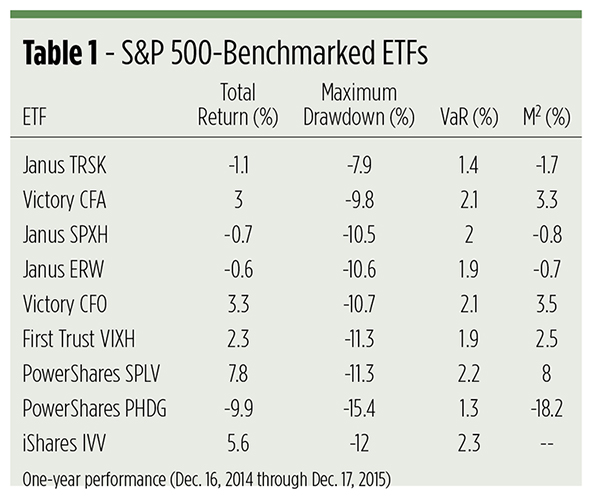

There are eight low-volatility ETFs benchmarked to the S&P 500, each trying to solve the drawdown problem in a distinct manner. If we compare these funds to an S&P 500 tracker such as the iShares Core S&P 500 (NYSE Arca: IVV), we can get a sense of their effectiveness along a number of risk parameters. First, there’s the maximum drawdown conceded in the past year. Seven of the low-vol funds countenanced smaller drawdowns than IVV’s 12 percent hit.

The entire set of ETFs beat IVV on a Value-at-Risk (VaR) basis. VaR represents an ETF’s potential daily loss at a 99 percent confidence level. IVV can be expected to lose no more than 2.3 percent of its value on 99 days out of 100. On average, the low-vol portfolios show a 1.9 percent VaR.

Another measure, M-squared (M2), gauges the risk-adjusted return of each ETF. M-squared depicts the ETF’s return if it was as volatile as the IVV portfolio. The higher the M-squared value relative to an ETF’s total return, the better. On this basis, the S&P 500-benchmarked ETFs are a mixed bag. Collectively, they skew negative, but that’s due to the performance of one extreme outlier. Without that one fund, the seven remaining ETFs exhibit an average 0.2 percent volatility benefit.

This brings us to returns. Only one of the low-vol products exceeded IVV’s gross performance last year. Six conceded upside as the cost of reduced volatility, and one was a double whammy of negative returns and deeper drawdowns.

The Best and Worst Performers

The best performer was the PowerShares S&P 500 Low Volatility Portfolio (NYSE Arca: SPLV), which tracks a weighted index of the 100 least-volatile stocks in the S&P 500. SPLV covers all four bases: a higher total return than IVV, a shallower maximum drawdown, less VaR and a significantly high M-squared value. Despite this, SPLV correlates highly to IVV with a .87 r-squared coefficient. Beta, at .90, is close to the benchmark ETF as well.

The worst overall performance was turned in by the PowerShares S&P 500 Downside Hedged Portfolio (NYSE Arca: PHDG), an actively managed ETF built on S&P 500 component stocks overlaid with VIX (CBOE Volatility Index) futures. PHDG can, during periods of exceptional volatility, maintain a substantial cash position as well. Presently, the asset mix is 90 percent stocks and 10 percent VIX futures.

Oddly enough, VIX futures are themselves notoriously volatile. And not in a good way. The annualized standard deviation in settlement prices for the January 2016 contract topped 51 percent over the past eight months alone, making it a very expensive exposure to maintain. That, and swaps into and out of cash, contributed to PHDG’s negative return.

Also noteworthy is the Janus Velocity Tail Risk Hedged Large Cap ETF (NYSE Arca: TRSK), a portfolio that allocates 85 percent of its heft to equity exposure and 15 percent to a volatility hedge. TRSK isn’t selective—it holds all the S&P 500 component stocks overlaid with a dynamic long/short exposure to short-dated VIX futures. The hedged portfolio aims for a 35 percent net long exposure. TRSK gets close to its target, too, earning a .31 beta coefficient over the past year. Still, TRSK trades return for low drawdown risk.

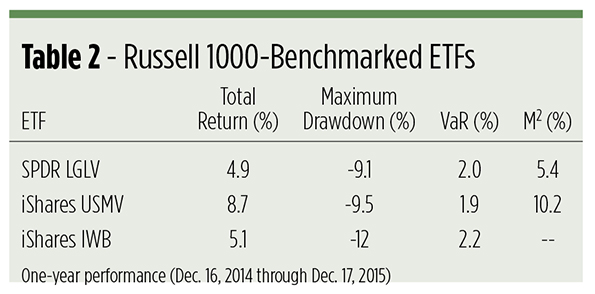

Two other low-vol portfolios trade in the large-cap space, but are not benchmarked to the S&P 500.

The SPDR Russell 1000 Low Volatility ETF (NYSE Arca: LGLV) draws the least volatile stocks from the Russell 1000 universe on an unconstrained basis, while the stocks selected for the iShares MSCI USA Minimum Volatility ETF (NYSE Arca: USMV) are chosen and weighted subject to sector and correlation limits.

Even though the USMV portfolio is a derivative of a different index, it’s been more closely correlated to the iShares Russell 1000 ETF (NYSE Arca: IWB) than LGLV over the past year. (The only domestically traded ETF tracking the MSCI USA Index is now equal-weighted. Accordingly, we used an ETF tracking the cap-weighted Russell 1000 as LGLV’s benchmark to better gauge the effectiveness of the embedded low-volatility strategy.)

In the end, USMV comes out on top, producing significantly higher total returns and lessened downside risk compared to IWB.

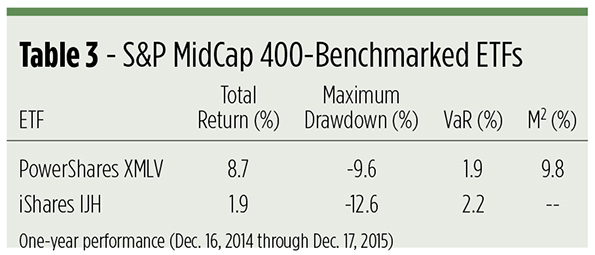

Don’t Forget Mid-Caps and Small-Caps

The stock universe for the iShares Core S&P MidCap 400 ETF (NYSE Arca: IJH) is the same trolled by the PowerShares S&P MidCap Low Volatility Portfolio (NYSE Arca: XMLV). Currently, about 80 of the least volatile S&P MidCap 400 companies take up residence in XMLV. The fund ends up fairly well correlated (r-squared at .81, beta at .79) with IJH, but handily outdoes the index tracker in terms of total returns and risk.

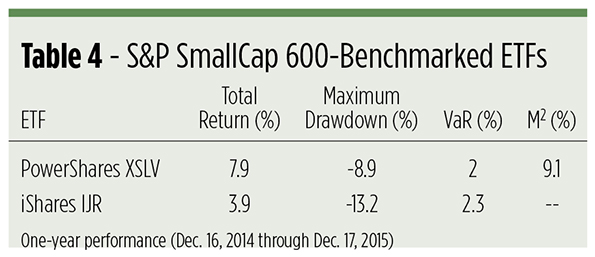

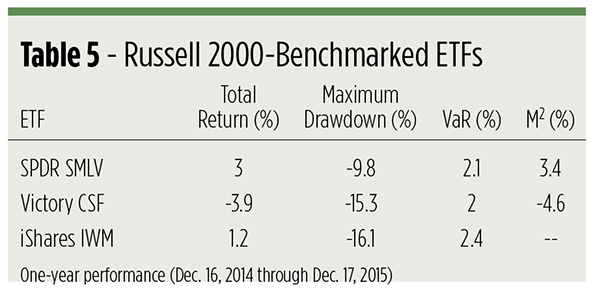

Three ETFs follow low-vol strategies in the small-cap space, one tied to the S&P SmallCap 600 Index and two bound to the Russell 2000.

Like its SPLV and XMLV siblings, the PowerShares S&P SmallCap Low Volatility ETF (NYSE Arca: XSLV) tracks a volatility-weighted index of stocks derived from its benchmark. About 120 of the least volatile securities in the S&P SmallCap 600 Index populate the XSLV portfolio, producing a .80 beta and a .84 r-squared value. Even so, the low-vol ETF’s one-year return was double that of the iShares Core S&P SmallCap 600 ETF (NYSE Arca: IJR).

The SPDR Russell 2000 Low Volatility ETF (NYSE Arca: SMLV) comprises small-cap stocks selected and weighted by low volatility and other factors, yielding a portfolio modestly correlated to the iShares Russell 2000 ETF (NYSE Arca: IWM). IWM’s movements explain about two-thirds of SMLV’s. The low-vol fund delivers a .70 beta and a .64 r-squared coefficient while nearly trebling IWM’s one-year return.

Summing it all up

You could say that the low-vol ETFs we’ve examined do what they promise—if VaR is your yardstick, that is. All 14 portfolios produced VaR values below that of their benchmark ETFs.

In terms of maximum drawdowns, 13 ETFs—93 percent of those analyzed—experienced shallower slumps than their bogeys.

But here’s the kicker: Only 36 percent—5 of 14—low-vol products outdid their associated index trackers’ total returns.The common denominator for these funds is simplicity. Most utilize a straightforward screen that filters stocks by standard deviation, with the least volatile issues given greater weight in the ETF portfolio. Overlays, equal risk weighting and other complex schemes can produce portfolios with low risk parameters, but they often do so at the cost of truncated returns.

It’s no wonder really. Many of these low-vol strategies are products of sophisticated financial engineering. Complexity often engenders unintended or unwanted outcomes. Investors seeking low-risk returns in 2016 may want to heed the words of that great engineer Leonardo da Vinci who declared, “Simplicity is the ultimate sophistication.”