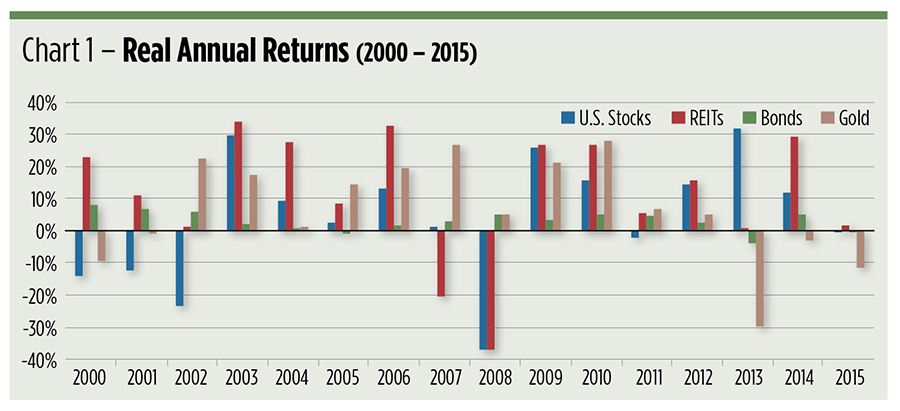

Try to guess the best inflation hedge of this century.

Thinking of stocks? Bonds? Gold? Nope. You should be thinking of real estate, specifically real estate investment trusts (REITs). REITs, as a class, have produced positive real returns in 14 of the past 16 years, earning an average 11.7 percent annually. Gold, the oft-touted inflation slayer, scored positive after-inflation returns in just 11 of the last 16 years. Bullion’s average real return? Just 7 percent (see Chart 1).

Not surprisingly, REITs have become the darling of the alternative investment (“alts”) chattering classes. REITs, too, have become fodder for fund manufacturers who have packaged them into 185 mutual, exchange-traded and closed-end portfolios, according to the National Association of Real Estate Investment Trusts (NAREIT).

The vast majority of these funds are long-only, meaning they have 100 percent exposure to real estate. A handful, though, pursue long/short strategies, tempering their bullish concentrations with short sales, credit/interest rate spreads or other hedges.

Long/short funds are being eyed more closely now as concerns about a maturing real estate cycle have heightened. The bull market is seven years old and, according to some observers, starting to tire. These pundits may be on to something. Near the end of August, REITs were up better than 11 percent for the year as measured by the Vanguard REIT Index Fund (OTC: VGSLX), which tracks a diversified benchmark of 150 publicly traded trusts. An 11 percent gain’s impressive, but more so was the 16 percent peak reached at the beginning of that month. Some analysts view August’s sell-off as normal volatility; others forewarn of a protracted downturn ahead of anticipated interest rate hikes.

If the bull market continues, you might think that long/short funds would forego some gains because of their bearish positions. If you’re thinking in terms of risk-adjusted returns, you’d be half right.

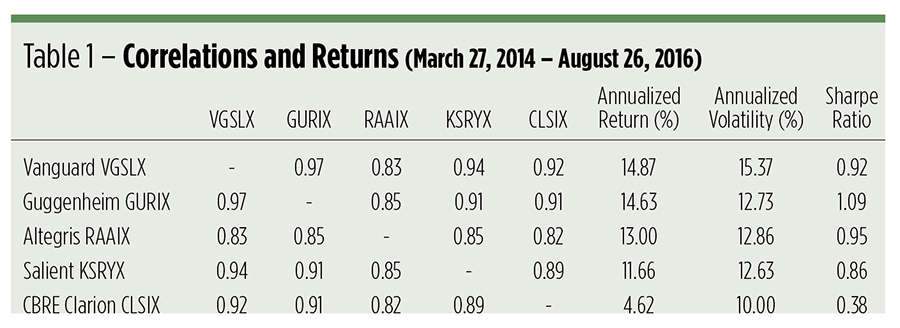

Among four readily identifiable long/short REIT funds, two have actually cranked out better Sharpe ratios during their tenure than the Vanguard index product (here, tenure refers to the lifespan of the newest fund).

Long/short REIT funds

Table 1 puts the long/short funds side by side along with the Vanguard portfolio. Most notably, you can see that the index tracker’s average annual return edges out the long/short funds. But look at the Vanguard fund’s volatility. It’s significantly higher than that of the other products. It’s so high that, in fact, it’s knocked down the index portfolio’s risk-adjusted return—its Sharpe ratio—below two of the short-enabled funds.

Clearly, the advantage of long/short REIT funds is volatility control. What more is there to know about these portfolios? What are they designed to do?

The oldest fund, the Salient Tactical Real Estate Fund (OTC: KSRYX, KSRAX), was launched in 2006 as the Forward Real Estate Long/Short Fund. The fund’s managers use a bottom-up investment approach, based on quantitative and qualitative analyses, to select REITs and real estate operating companies (REOCs).

In July, KSRYX’s net exposure was 84 percent long. The majority of the fund’s short exposure is obtained through exchange-traded category funds including the Vanguard REIT Index ETF (NYSE Arca: VNQ) and the iShares U.S. Real Estate (NYSE Arca: IYR). Over the past 12 months, the fund’s short position has swung between 6 and 19 percent and has averaged about 16 percent. KSRYX portfolio runners have been lightening up on short positions since the beginning of 2015.

The CBRE Clarion Long/Short Fund (OTC: CLSIX, CLSVX) at last look committed more than a third of its securities portfolio to short sales. CLSIX shuns ETFs, restricting investments on both the long side and the short side to REITs and REOCs. At last look, the fund’s largest gross short was the retail sector. On a net basis, CLSIX leans heavily to the long side of the office sector.

The Altegris AACA/Real Estate Long Short Fund (OTC: RAAIX, RAAAX) aggressively seeks alpha on both sides of its portfolio by pursuing a “125/25” strategy. Presently, the fund’s net long exposure is about 100 percent: 125 percent long and 25 percent short. The “extra” 25 percent dose of long exposure is financed through the proceeds of short sales and interest rate/credit spreads. Data centers are currently favored on the portfolio’s long side.

Market neutrality is sought through the Guggenheim Risk Managed Real Estate Fund’s (OTC: GURIX, GURAX) long/short strategy. But that’s just one prong of a tactical trident that also includes a long-only and a so-called dynamic exposure allocation. Like the Altegris portfolio, Guggenheim’s fund takes a leveraged long stance, financed by its short sales. GURIX’s net long exposure was last reported at 82 percent, with the largest short exposure obtained through ETFs.

Table 1 tells us that all the funds are, to one degree or another, highly correlated to the index product. There’s a definite long tilt to them all. Two of the funds, RAAIX and GURIX, are particularly aggressive users of leverage, while the CBRE Clarion portfolio has actually reduced leverage recently.

Future foretold?

During the real estate bull run, the funds’ short positions have been mostly tactical, i.e., alpha-seeking and focused on sectors thought to be underperforming. For most of the funds, the drag on performance from the short side can be attributed to goofs in opportunistic stock selection and timing. The Salient fund, however, seems most disposed to utilize sector ETFs for strategic hedging.

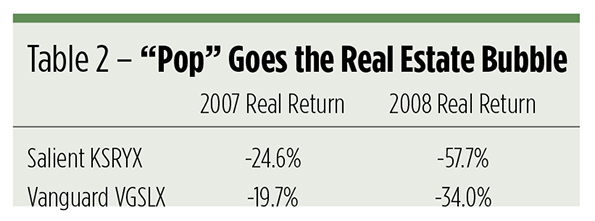

So what of hedging? If the real estate market turns down, will these short-enabled funds fare better than long-only portfolios like VGSLX? Unfortunately, we have a limited history to reflect upon. Long/short REIT funds are fairly new creations. Only one was extant during the 2007–2008 slide, so we’re pretty much left to speculate on their performance in the next bear cycle on fairly thin data.

We have the “grandaddy” of the short-enabled portfolios, the Salient KSRYX fund, which ruefully underperformed the Vanguard index portfolio as the real estate bubble burst in 2007–2008 (see Table 2).

Salient’s two-year peak-to-trough drawdown was stunning at nearly 78 percent. It took until January 2015 for the fund to fully recover the loss. The Vanguard index portfolio’s drawdown was 68 percent; breakeven was attained by April 2012.

We all know that past performance does not guarantee future results. And for that, perhaps investors in short/long REIT funds ought to be thankful.

Does this foretell fund behavior in the next sell-off? Well, there’s one thing we can tease out from our side-by-side fund comparison in Table 1. The RAAIX portfolio, with its relatively modest correlation to the Vanguard fund, stands out as more “off-index” than the others. Does that mean RAAIX could “zig” when REITs “zag”? Perhaps. The question we’re left to ponder is whether RAAIX’s portfolio runners will have the fund strategically hedged in time for the next bear market intermission. That can’t be known with certainty, but the lower coefficient suggests that it might be easier for RAAIX than it would be for the other funds.

For now, we know this: An allocation to REITs—taken from the equity side of a portfolio—can diversify risk and augment income. We know, too, that real estate is cyclical. Bull markets tend to be long-lived; bearish phases are often short and relatively shallow.

Whether or not investors use long-only or long/short REIT funds largely depends upon their risk tolerance—and their bullishness.

Brad Zigler is WealthManagement.com's Alternative Investments Editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.