By Eric Balchunas

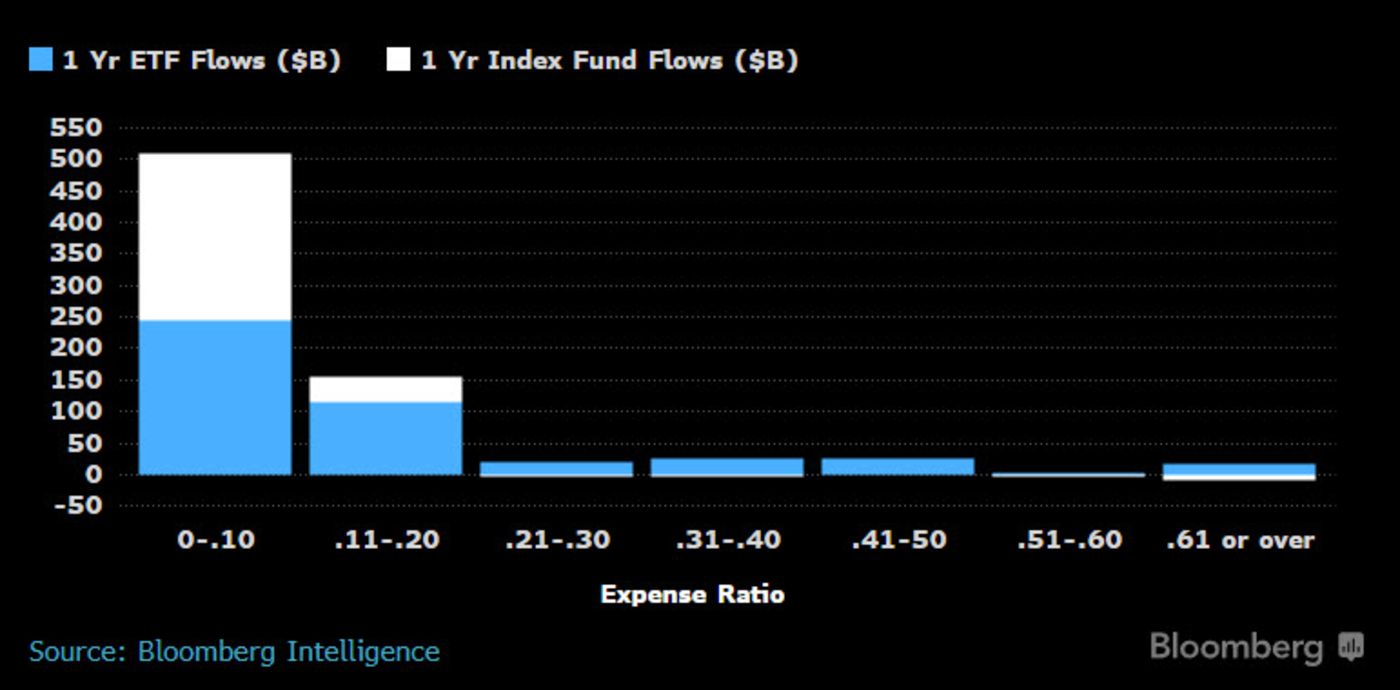

(Bloomberg View) --Bleeding assets under management, active fund managers have taken to demonizing passive funds as bad for markets and capitalism in an effort to win back investors. It isn’t working. The shift from active to passive -- which is really just a reflection of an even bigger move away from high-cost to low-cost funds -- is gaining steam, with almost $3 billion a day going into exchange-traded funds and index funds. And about 75 percent of these flows are going to products that charge 0.10 percent or less. Simply put, cheap beta is a smash hit.

So where do active funds fit in a world in which passive is the star of the show? Rather than fearmongering, they may want to consider a new role: supporting actor. The fact is, most of these newly passive investors are not going to be satisfied with buying and holding three index funds or ETFs over the long haul. The temptation to spice up the portfolio here and there to try and do a little better is too strong to ignore.

But using active funds in small doses to complement a broader portfolio creates a win-win situation for everyone. Here are a few reasons:

- It lets active managers be truly active. For decades, many active managers have had to worry about not straying from the benchmark for fear of underperforming and losing investors. This risk is why most were unable to limit the 2008 losses that ultimately turned off so many investors. But if benchmark-like returns (beta) are already being covered in the core of investors’ portfolios by an index fund or ETF, it frees the manager to be truly active and make high-conviction bets. A new generation of highly concentrated managers are starting to crop up in the ETF world.

- It increases investors’ ability to tolerate an underperforming active fund. If it isn’t a core position, an investor will generally stomach the ups and downs. This is key because most truly active, disciplined strategies will go through stretches -- sometimes long ones -- of underperformance on their way to generating long-term alpha.

- It keeps the overall cost of investors’ portfolios low while allowing active managers to still get paid. As long as the core of the portfolio is dirt-cheap, investors would be more willing to use a fund that has a higher fee as it won’t do too much to bring the overall cost of the portfolio up. Active funds that insist on wanting to be the core of a portfolio are going to have to compete with the likes of Vanguard on fees -- almost always a losing battle. But supporting-role active funds will be able to make a living. Investors are much more willing to pay true active managers that can consistently beat their benchmarks than those that hold virtually the same stocks as the S&P 500 Index.

- It allows active managers to embrace passive managers. Trashing index funds and ETFs is not a good strategy for an active manager. It looks like they hate the players, not the game. Active managers -- many of whom likely use some index funds in their personal accounts -- are better off admitting that free beta is great and then detail what they can provide to enhance portfolio returns.

- It keeps the market efficient. While active managers probably overestimate their value to capitalism, they are important for price discovery. To help to keep prices honest, you need active managers to do their homework.

Even so, many active funds will choose to wait for the pendulum to swing back from “peak passive.” But that isn’t going to happen. The internet has likely made this shift a secular change as opposed to a cyclical one by allowing for more transparency, more investor education and more options. And remember that we are coming from a place 25 years ago where 98 percent of assets were in active funds. It can be argued that was the peak and we are merely moving towards equilibrium between active and index.

The market needs active management, but maybe not as much as active managers think. They would be wise to stop the blame game, acknowledge the role they played in the rise of passive investing. and figure out the role they can play going forward.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Eric Balchunas is an analyst at Bloomberg Intelligence focused on exchange-traded funds.

To contact the author of this story: Eric Balchunas at [email protected] To contact the editor responsible for this story: Robert Burgess at [email protected]

For more columns from Bloomberg View, visit bloomberg.com/view