It’s not easy building a proper portfolio. First of all, portfolio construction requires information. And, if you seek out actively managed investments, information ratios.

An information ratio, or IR, is the ultimate measure of an active manager’s worth. A positive IR is harder to come by than a positive alpha coefficient, so it’s not surprising that IRs aren’t headlined in most mutual fund or ETF marketing material. Not many managers earn a salable number.

And that’s a pity because investors and their advisors could save a lot of time and capital if they could readily sort an array of active funds by their IRs to find desirable portfolio allocations.

So, what’s an IR and why is it a more daunting metric than alpha? Well, like an alpha coefficient, an information ratio measures a fund’s performance against a benchmark, but IR goes one step further by gauging a manager’s consistency. Alpha quantifies a fund’s beta-adjusted excess return. An IR—derived by dividing a fund’s active return by its tracking error—reveals the length of time a manager outperforms the fund’s benchmark.

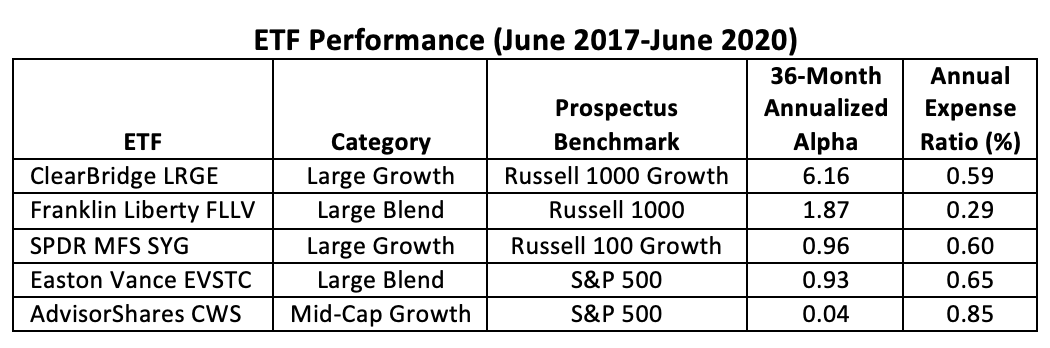

To test the current relationship between these two statistics, we queried the Morningstar active ETF database for funds with positive alpha coefficients across nine equity capitalization/style boxes. We found just five out of the 83 active funds cranked out positive risk-adjusted returns over the past three years. Why so few? Simply because Morningstar doesn’t publish alpha or other MPT stats until funds develop 36-month track records. Many active ETFs are just too young to get on investors’ radar. We’ll come back to that shortly.

Of the five ETFs, Morningstar calculates an average alpha coefficient of 1.99 with 0.96 as the median value.

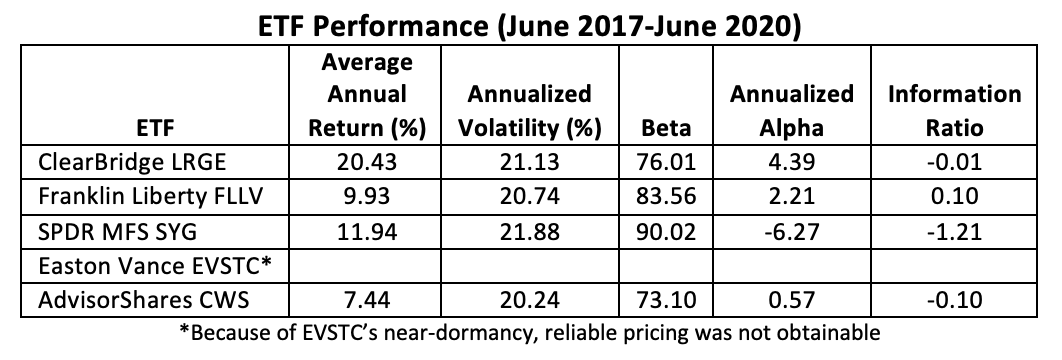

Morningstar’s reliance on 36 monthly data points is fine for getting a bird’s eye view of a fund’s performance, but the policy precludes evaluation of young and potentially promising funds. For that reason, we use daily, rather than monthly, returns to calculate performance statistics. Doing so creates a data string long enough to make judgments on a fund’s utility at an earlier stage in its development.

Using daily data also allows us to double-check the seasoned funds’ published stats against today’s reality. For example, the table-topping ClearBridge Large Cap Growth ESG ETF (Nasdaq: LRGE) alpha shrinks to 4.39 when it’s plotted against the daily performance of the iShares Russell 1000 Growth ETF (NYSE Arca: IWF), the investable version of its benchmark.

And LRGE’s information ratio? Using daily data, the ClearBridge ETF comes up a bit short with a -0.01 quotient. A negative IR signifies a fund unable to produce positive excess returns. Indeed, if you look at the daily returns of LRGE and its benchmark ETF in the chart below, you can see that LRGE had an edge on IWF until February when the coronavirus pandemic clipped the ClearBridge fund’s wings. Over the past three years, LRGE’s average annual return has been 20.43%. For IWF, it’s 20.61%.

Using daily data, our ETF universe now looks like this:

As you can see, only one ETF—the Franklin Liberty U.S. Low Volatility ETF (NYSE Arca: FLLV)—earned a positive IR. Positive, yes, but not by much. An IR under 0.40 indicates a manager’s inability to produce excess returns for extended periods of time. Normally, savvy portfolio builders eschew such funds.

ETFs sporting IRs between 0.40 and 0.60 may get a lookover, but it’s IRs between 0.61 and 1.00 that signify more desirable ETFs capable of producing higher potential returns.

In this case, investors looking for a blended large-cap exposure will have to balance the higher cost of the active ETF—29 basis points versus 15 bps for the iShares Russell 1000 ETF (NYSE Arca: IWB)—against FLLV’s history of higher returns. The low-vol fund grew at a compound annual rate of 9.93% over the past three years while IWB appreciated at an 8.93% average annual clip. FLLV, true to its mandate, cranked out its return with less volatility (20.74%) than IWB (22.19%).

In sum, it pays to look beyond a fund’s published MPT stats to gain more insight into active managers’ capability to consistently deliver market-beating results. The information ratio earned its name because it informs investors of the manager’s talent. If the IR’s too low or negative, you’re likely to be better off investing in an index fund.

Brad Zigler is WealthManagement's alternative investments editor. Previously, he was the head of marketing, research and education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.