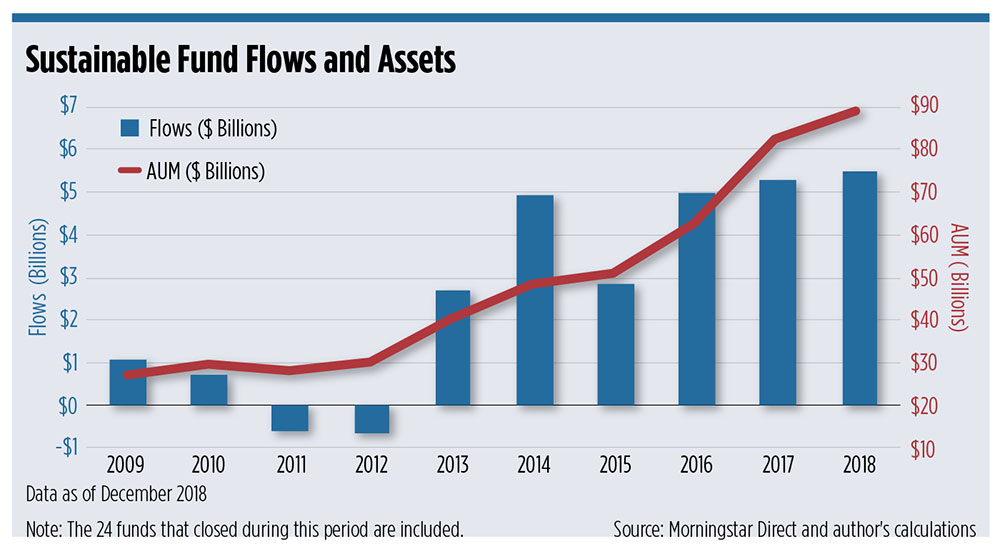

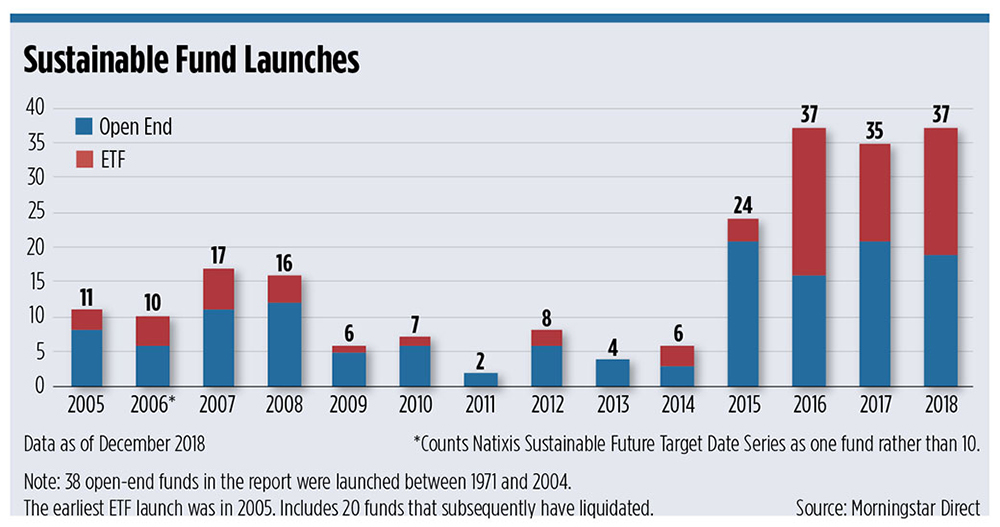

The hype around sustainable investing has been growing for a number of years, and many asset managers, faced with pressure to lower fees on their traditional lineup of mutual funds, have jumped on the bandwagon. Last year, the number of exchange traded funds and mutual funds in the sustainable universe grew by almost half to a total of 351, with a record 37 new funds launched during the year (tied with 2016), according to Morningstar. And while stock market returns were basically flat in 2018, ESG funds pulled in nearly $5.5 billion of new money during the year and already a record $8.9 billion in the first half of this year.

But a good portion of those assets are in funds that did not start out as ESG products but were "repurposed" to include an ESG mandate. Some managers simply made a change to the previously plain vanilla fund's prospectus, adding a gloss of verbiage about using ESG criteria, without changing the fund's holdings.

“The assets didn’t come into those intentionally because of the ESG mandate,” says Neil Bathon, founder and partner at FUSE Research. “When you strip away the noise that’s in the data, you realize that there’s very little evidence one can point to to suggest momentum for ESG offerings.”

Total assets under management in ESG funds was $161 billion at the end of last year, Morningstar says, but $72 billion of that was in repurposed funds. Morningstar pointed out in its report that asset managers had rarely added sustainability criteria to the prospectuses of existing funds before 2017, but the trend of putting the language of ESG in fund literature is accelerating.

Last year, 62 existing funds added ESG criteria to their prospectuses for the first time, according to Morningstar, yet only 11 of those funds involved "a complete makeover" with changes in the funds' holdings. In the other cases, the funds were simply signaling that they now consider ESG factors as part of their overall investment process, without necessarily changing the portfolio.

“Transforming funds into sustainable offerings is a way for asset managers to build their sustainable investing business without creating new funds from scratch and having to wait for them to reach scale,” wrote Jon Hale, global head of sustainability research at Morningstar, in the Sustainable Funds U.S. Landscape Report. “Because of the massive investor move to passively managed funds, many asset managers have an inventory of actively managed funds that are unable to attract new assets at the rate they are losing assets.”

For example, Goldman Sachs added ESG criteria to its International Equity Fund, now the Goldman Sachs International Equity ESG Fund. Putnam in 2018 completely retooled its actively managed, $4.5 billion Multi-Cap Growth Fund and renamed it the Putnam Sustainable Leaders Fund, with an emphasis on corporate sustainability metrics alongside its regular stock selection criteria. The smaller $450 million Putnam Multi-Cap Value Fund became the Putnam Sustainable Future Fund.

Putnam Spokesman Jon Goldstein argues that the change was not a defensive move to stem outflows from those funds but rather part of a much bigger strategy at the firm to incorporate sustainable investing across its platform. The firm hired Katherine Collins in May 2017 as head of sustainable investing, and she has been building out a dedicated team focused on ESG issues.

“Offering these types of strategies, we were making a very strong statement about our belief in the ability of this approach to enhance returns and limit downside risk," Goldstein said. "We think these are strategies that offer shareholders a different and arguably very strong way to take advantage of this investment lens.”

A spokesman for Goldman Sachs Asset Management declined to comment.

Aberdeen, J.P. Morgan and Morgan Stanley, on the other hand, simply added "ESG considerations" to the prospectuses of many of their funds, without neccessarily changing the portfolios. "These "ESG consideration" strategies do not go as far in their commitment to sustainable investing as those that have been completely retooled, but their growing number is an indication that ESG consideration is becoming a standard part of many investment processes as asset managers have developed ways to complement their existing approaches using ESG criteria," according to the Morningstar report. Few are being actively marketed as "sustainable" investment funds.

“I think it pays to look to see how deeply ESG is actually integrated into the investment process, and it really can vary,” says Daniel Kern, chief investment strategist at TFC Financial Management, a registered investment advisory in Boston. “It's important to ask questions of the fund manager or the representatives of the fund firm to really understand whether ESG is really core to the fund's manager's process, or whether it's just something that's added on as a paragraph in a perspective or a page in a pitchbook.”’

Kern says some statistics about ESG funds include those offerings that simply exclude certain types of stocks, such as tobacco or arms manufacturing, and that can be misleading. “That may be technically correct in some way, but it’s certainly outside of what I think the spirit is of the ESG universe.”

In its research, Morningstar considers “sustainable funds” as any that state in their prospectus that they consider a firm's ESG criteria in their investment process, or say that they pursue a sustainability-related theme or measurable sustainable impact alongside financial return. They exclude those funds that employ values-based criteria, such as exclusions of so-called “sin stocks.”

Kern says that while there’s a lot of new products available and some asset flows, he would consider it slow growth. There are still barriers for advisors to get clients to adopt the strategies more broadly.

For one, it can be an expensive proposition for clients to switch from their current positions to a more ESG-focused portfolio in taxable accounts.

In addition, many clients still get that “deer in the headlights look” when presented with the amount of choices in the ESG space, he says.

“Some clients are focused on climate change, so they want a solution that either avoids fossil fuels or that moves the dial on going to a cleaner world,” Kern says. “Other clients have different hot buttons; private prisons are a hot button for certain clients now; diversity is an issue for an increasing number of clients. So it's hard. It's not a one-size-fits-all category, so sometimes I think the degree of choice creates a barrier to making a change.”

Much of the growth comes from institutional investors. During the first quarter, the newly launched Xtrackers MSCI USA ESG Leaders Equity ETF (USSG) took in the most assets of any other sustainable fund, but $870 million was seed money from Finnish insurer Ilmarinen, according to Morningstar.

Institutional investors have mandates to allocate to sustainable investments, but Bathon says he doesn’t see broad adoption of the strategies on the retail side. The big brokerages, for instance, talk a lot about their ESG initiatives, but none of them have dedicated support staff for them.

“On the retail side, I hear a lot of talk from distributors about promising this massive influx of assets, but I think if you ask them if they’ve incorporated ESG into their models, they would say, ‘No.’ And they’d say, ‘We have separate models that are ESG,’ which no one uses,” Bathon says.

And there are few prospects for stand-alone ESG offerings, he adds. Bathon believes ESG will eventually become integrated into the day-to-day process for valuing securities. Some asset managers have been incorporating ESG criteria for years as standard risk analysis; they just don’t publicize it as such. If you look at the largest U.S. open-end funds with four or five globe ratings from Morningstar, a measure of how well the holdings in a portfolio are performing on ESG, many of them are not ESG-focused funds. American Funds, for instance, tend to have high sustainability grades, according to Morningstar's criteria, even though they’re not categorized or sold as "sustainable" funds.

One reason for that could be that nearly every active asset manager uses the “G” (governance) to assess risk in terms of how companies are being governed. “There isn’t a reputable portfolio manager working today that doesn’t place significant time and energy evaluating the governance of the firms in which they invest,” Bathon says.

“Ultimately, ESG will become mainstream—whether it's mainstream because of client demand or mainstream because fundamental investors realize that the E and the S are important from at least a risk management perspective,” Kern says. “I think that ESG is going to grow over time in part because clients demand it and figure out how to implement it, but I think also investors are going to start to say, ‘Well, this is something we should be doing anyway to be better investors.’”