Recently, we wrote in praise of commodities—that is, a long-only broad-based futures portfolio—as the year’s best inflation hedge. Commodities, however, may not be the best risk diversifier over a longer investment horizon.

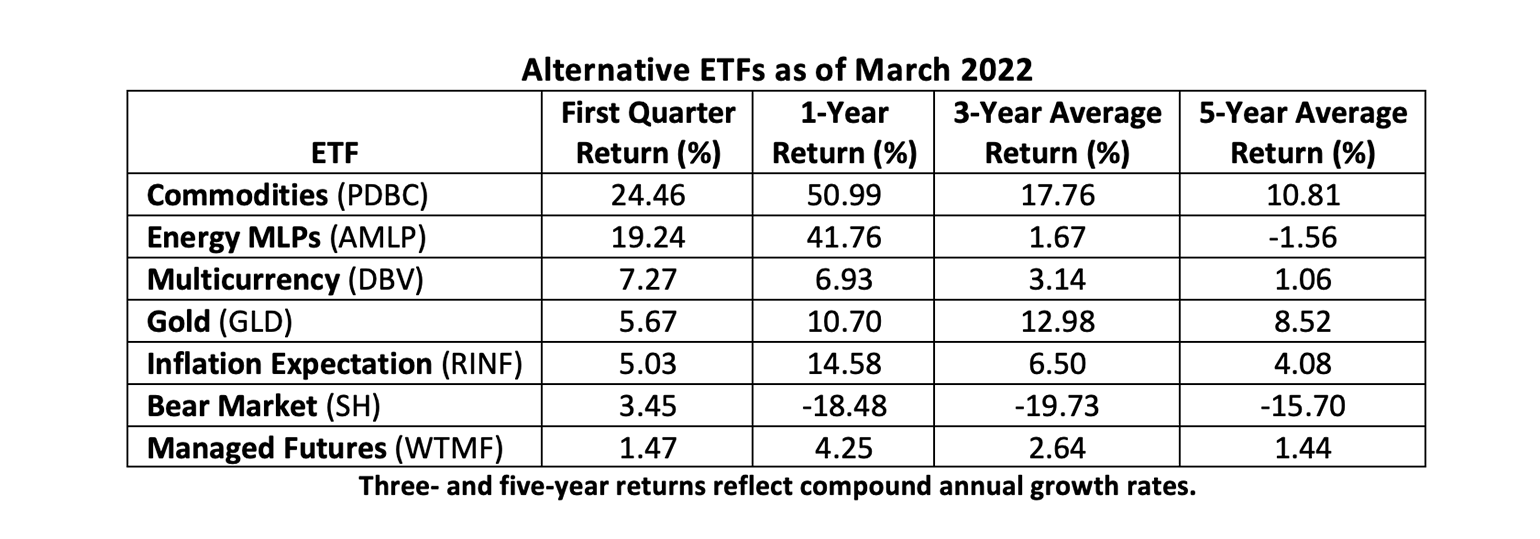

Let’s not get ahead of ourselves. There are a number of alternative investment ETFs that can be used to round out a portfolio and mitigate equity market risk. We regularly track 14 of the largest funds to gauge the state of the field. Half of this universe produced positive returns for the first quarter of 2022:

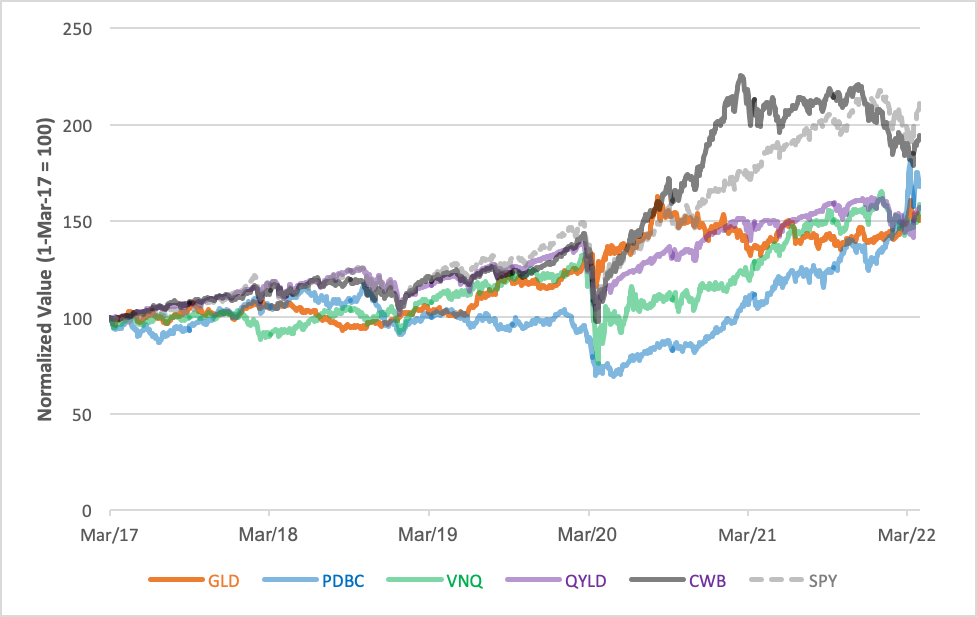

A quarter or a year’s one thing, but a year doth not a portfolio make. The alts universe looks a bit different when regarded through the lens of cumulative five-year returns. All but two of our 14 ETFs are now above their March 2017 values, with the top five funds growing 65% on average. Risk diversification, though, isn’t really measured by returns alone; volatility and correlation figure large in that calculation.

When we regard a traditionally balanced portfolio (60% equities/40% fixed income), we find there’s a diversification benefit obtained by the addition of bonds to an equity exposure. We’re all taught that making space in an equity portfolio for a fixed income allocation can significantly reduce overall volatility. And, empirically, that’s true.

How so? Well, given the isolated volatilities of an equity (the SPDR S&P 500 ETF: SPY) and a fixed income (the iShares Core U.S. Aggregate Bond ETF: AGG) exposure, a 60/40 mix should have cranked out a weighted standard deviation of 10.81% over the past five years. Synergy, however, worked to produce a realized volatility of just 9.51%. That gives us a diversification ratio of 1.14 (10.81% ÷ 9.51%) for the bond-enhanced portfolio.

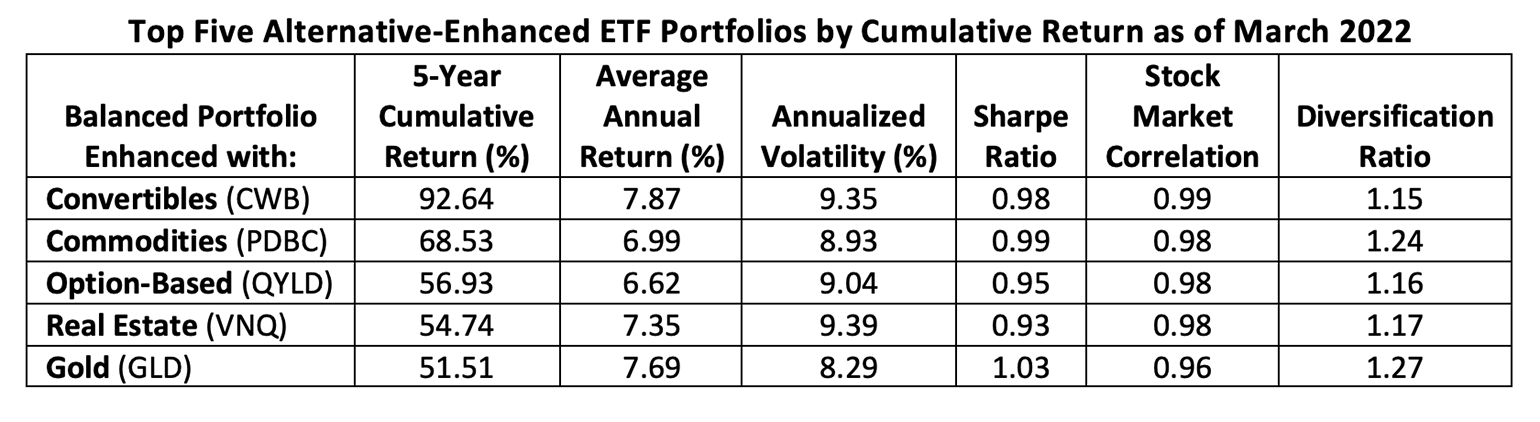

Now, adding an alternative exposure to this balanced asset mix—accomplished by carving out a 10% allotment from the portfolio’s equity side—ought to render a diversification ratio greater than 1.14 to be considered practical.

By this measure, all of our top five alt ETFs provided some diversification benefit, some to a great extent and some, well, not so much.

An exposure to gold, manifested through the SPDR Gold Shares (GLD) offers the greatest diversification benefit, owing to its near-zero correlation to stocks (0.03) and its modest correlation (0.33) to bonds.

Note, too, the gold-enhanced portfolio’s volatility (relatively low) and Sharpe ratio (relatively high). Gold, for much of the period, was the yin to the stock market’s yang, producing that most-sought after of portfolio prizes, a smooth ride.

Holding gold in your portfolio over the past five years might not have made you the richest of alt-savvy investors but you probably would have slept better when the equity market nosedived at the onset of the COVID-19 pandemic.

The metric that reveals a portfolio’s insulation against downside volatility is the Sortino ratio. Unlike the Sharpe ratio which compares an investment’s return to its total volatility—both upside and downside—the Sortino variant only penalizes downside deviation. The GLD-enhanced portfolio earned a table-topping Sortino ratio of 1.70 over the past five years. An investment with a Sortino ratio approaching 2.00 is generally considered very good.

Next best, at 1.58, is the portfolio augmented with the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), a long-only portfolio of diverse commodity contracts optimized to minimize the adverse effects of trading along the futures curve.

Adding the SPDR Bloomberg Convertible Securities ETF (CWB) to a balanced portfolio produces a Sortino ratio of 1.57. CWB is market cap-weighted portfolio of convertible bonds and convertible preferred stocks.

Sadly, the effect of contributing the Global X NASDAQ 100 Covered Call ETF (QYLD) to a balanced portfolio is actually negative. A 60/40 mix of SPY and AGG earns a 1.55 Sortino ratio but a 10% carve-out for QYLD drops the portfolio’s Sortino ratio to 1.49.

Worse still, the portfolio augmented with the Vanguard Real Estate ETF (VNQ) pulls down a rather lowly 1.44 Sortino ratio. Vanguard’s portfolio consists of a diverse mix of more than 160 domestic real estate investment trusts.

There’s no guarantee that diversification through alternative investments will provide investors with a smooth ride going forward. Still, we’ve always favored innovation (see Classic Commercial - Chevrolet's "Jet-Smooth Ride" - 1961 - YouTube) to level out the bumps and jolts in the road ahead.

Brad Zigler is WealthManagement's Alternative Investments Editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.