Back in my market making days, the term “edge” was commonly used among traders. The basic definition of trading edge is gaining an advantage over other players in the marketplace. What about investor edge? How can one investor outperform others in a marketplace that delivers unpredictable outcomes?

Reducing friction can be an effective way to boost portfolio performance. Frictional forces can come in many forms, but the most common facing investors are taxes, fees and expenses. All of these factors can significantly impact long-term investment performance but are often overlooked. Initial gross returns do not properly reflect the negative impact of these frictional forces. True investment outcomes (net results) factor in the friction and represent a better metric for measuring success.

Investors today are able to enjoy a much higher level of efficiency than what was experienced 25 years ago. For example, in the late 1990s, financial advisors typically charged a 2% management fee and invested in mutual funds that added another 1-2% in fund fees. Stocks traded in fractions with 1/8 to 1/4 point ($0.25) spreads and brokerages charged commissions on every executed trade. Bottom line: The difference between gross returns and actual (net) returns was sizable and presented a considerable hurdle for investors. Thankfully, all of these frictional costs have come down significantly. Advisory fees now range from 50-100 bps, indexed funds/ETFs carry minimal expense ratios that are nearing zero, most stocks trade with penny spreads, and almost all brokerages have eliminated commissions on trades.

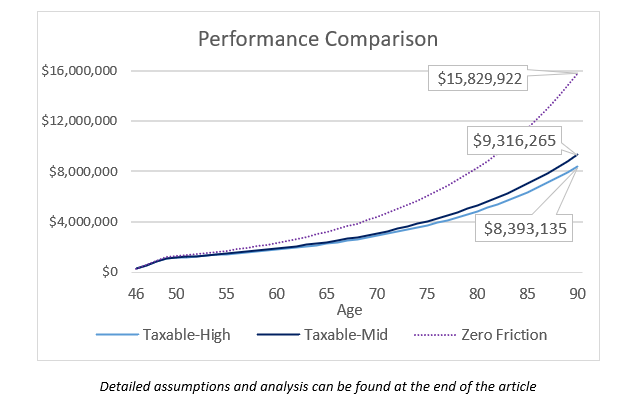

Unfortunately, there is one frictional force that has not been come down over time … taxes. Investors still get taxed on portfolio gains whether it be in the form of the lower long-term capital gains rate or the higher ordinary income rate. The charts and tables below illustrate the negative impact that taxes can have on a typical investment portfolio.

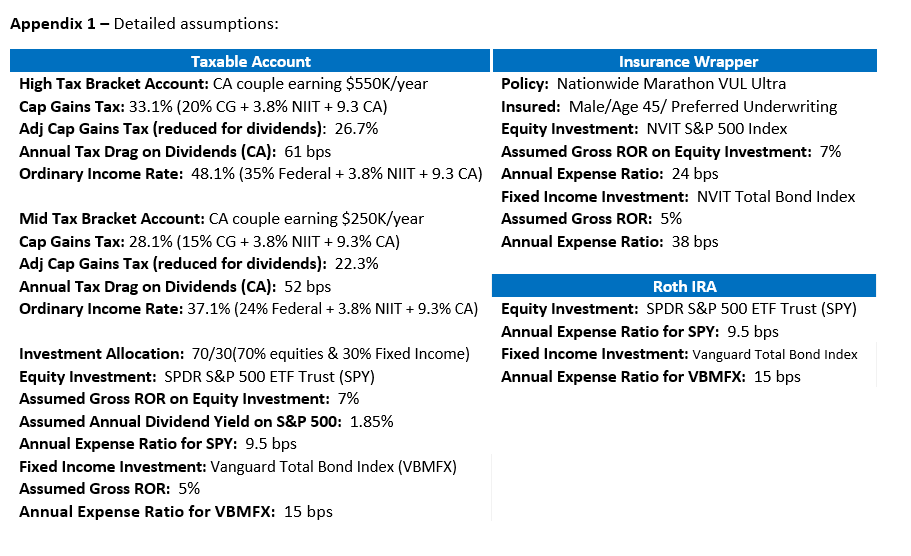

The analysis assumes a 45-year-old California couple investing $1 million ($250K/year for 4 years) in a typical 70/30 allocation with 70% in equities (SPDR S&P 500 index) returning a hypothetical 7% and 30% in fixed income (Vanguard Total Bond Index) returning 5%.

Two different taxable accounts will be compared:

- Mid-level tax bracket: $250,000/year in combined income; and

- High-level tax bracket: $550,000/year in combined income.

Performance Analysis:

- Tax implications for the S&P 500 investment are twofold: (1) annual taxes paid on dividends, and (2) long-term capital gains taxes owed upon liquidation (adjusted for dividends);

- Bond income is taxed at the higher short-term capital gains rate (ordinary income rate); and

- Assumes a buy-and-hold strategy (best case scenario for taxable accounts).

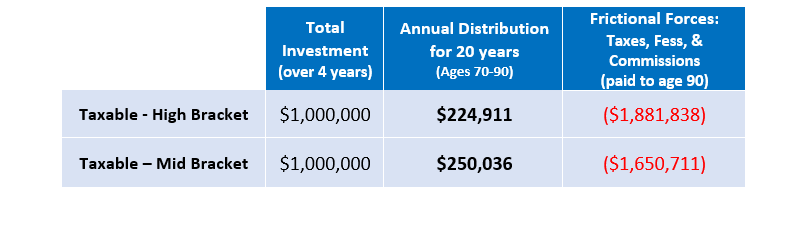

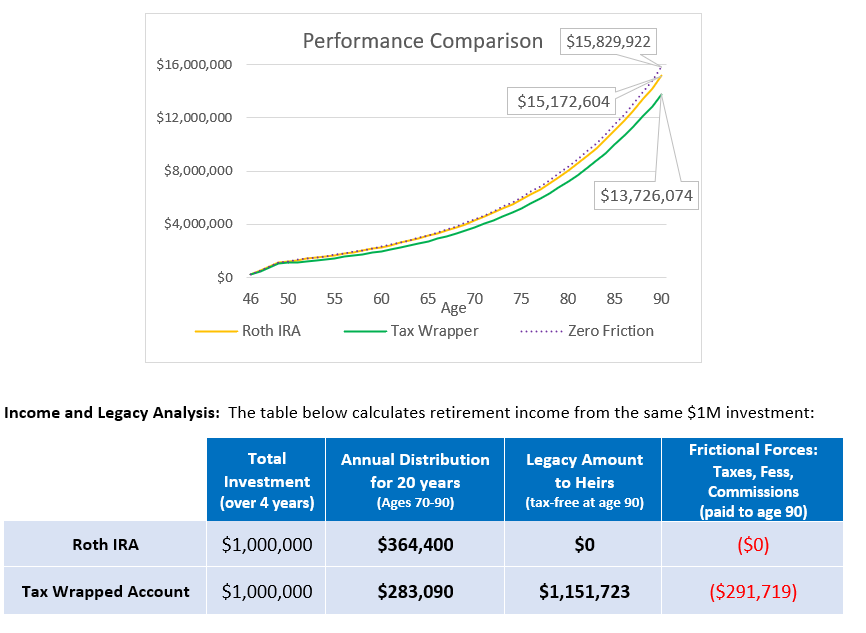

Income Analysis: The table below calculates annual retirement income from the same $1M investment:

In each of these examples, tax rates were kept constant throughout. Yes, it is possible that the investor may be in a lower tax bracket during retirement. They could also be in a higher one. The $1 million investment amount is in line with someone who might remain in a mid-to-high tax bracket.

So what steps can an investor take to narrow the gap and get closer to the “zero friction” line?

- Maximize contributions to Roth IRAs of all types. Traditional Roth IRAs, Roth IRA conversions/back door Roth IRAs and Roth 401(k) Plans. “Rothification” has become a popular movement in the US of late as the government has expanded the use of Roth’s under the recent Secure 2.0 legislation. Roth’s are designed to let participants invest after-tax dollars to capture tax-free growth and tax-free distributions during retirement. The government likes Roth’s because it is able to access the tax dollars upfront instead of waiting until retirement to collect as is the case in deferral based plans like traditional IRAs and 401(k)’s. In general, Roth IRAs represent an excellent way to reduce tax exposure and maximize retirement savings. Unfortunately, due to income limits and contribution caps, traditional Roth IRAs are not a viable option for most mid-to-high earners.

- Participate in company sponsored 401(k) and deferred compensation plans to defer taxes on income and investments. These can be especially advantageous when a company contribution match is provided. By utilizing pre-tax dollars, these plans offer significant tax-advantages on the front-end. However, upon distribution, they can be somewhat tax-disadvantaged as both the deferred income and all investment gains are taxed at the higher ordinary income rate. Whereas, normally, most investment gains are taxed at the lower long-term capital gains rate. 401(k) plans also carry additional administration fees (~1%) as well as higher fund fees when compared to Roth IRAs.

- Implement a tax-loss harvesting strategy. Tax-loss harvesting can reduce an individual’s overall tax bill by offsetting capital gains with generated losses. “Direct Indexing” is achieved by creating a separately managed account, or SMA, designed to track a specific index. This allows a manager or automated system to opportunistically sell stocks throughout the year that are trading at a loss and then replace them with securities having correlated characteristics/returns. For those planning to eventually sell their assets, loss harvesting will actually add to their future tax bill by reducing overall portfolio basis and, thus, increasing the amount of capital gains upon liquidation. However, after factoring in the time value of money, present day tax savings should generally outweigh any additional future tax obligations. The most ideal candidates for tax-loss harvesting are those planning to hold their investments until step-up in basis at death or donate them to charity.

- Utilize Tax Wrappers (also referred to as Insurance Wrappers) to reposition the same taxable investment allocation within a variable universal life insurance (VUL) chassis. This tends to benefit higher income level investors by delivering Roth-like results for those who have already maxed-out (or do not qualify for) traditional tax-advantaged accounts. It offers tax-free growth, tax-free withdrawals up to basis, and tax-free loans for all remaining distributions. The only requirement for this strategy is that the policy must remain in force with the death benefit being passed down to heirs. This is better suited for those with longer term investment horizons, who would like to build retirement income while also providing some legacy benefits to their family.

Performance Analysis: Looking at Roth IRA and Tax Wrapper results for the same 45 year-old CA couple investing in a 70/30 investment allocation.

As expected, the Roth IRA performs extremely well and is about as close as you can get to the “zero friction” benchmark. The only friction facing the Roth are fund fees which have already been baked into the performance analysis. The initial $1M outlay is purely hypothetical and probably unlikely to occur within a Roth IRA due to Roth contribution limits. However, relative performance remains the same so alternative funding levels (e.g. $50K, $100K or $10M) would still produce proportional results.

401(k) performance will typically lag that of a Roth due to the additional admin/fund fees. Varying expenses between plans along with occasional employer matching make 401(k)’s a challenge to accurately depict on a chart and why this option was not shown in the analysis above.

Quantifying the benefits of tax-loss harvesting can also be difficult and not easily demonstrated. A portfolio that uses tax-loss harvesting will generally outperform one that does not. The two main factors that determine loss harvesting success are market volatility (harvesting does better in highly volatile markets) and funding frequency (periodically adding money to the investment typically improves effectiveness).

The tax wrapper lagged the Roth IRA but outperformed the taxable equivalents by a fairly significant margin. The biggest downside to this option is public perception—many people simply do not like life insurance products and consider this type of strategy too complex. In terms of complexity, once in place, the insurance wrapper actually requires less maintenance than a taxable account with no annual 1099s or 1099-DIVs while retaining the ability to reallocate and/or shift investments at any time without triggering a taxable event.

Ernst and Young recently published a white paper titled “Benefits of integrating insurance products into a retirement plan.” The detailed analysis showed multiple investment combinations with the main takeaway being that adding a permanent life insurance component to an investment portfolio can potentially improve performance and generate higher returns.

Educating investors on the impact friction can have on their portfolio is an important first step. For example, take a high-net-worth investor with a 5% bond return:

- Do they realize this is roughly only 2.5% after taxes?

- Do they match the following year’s tax bill with the initial corresponding investment gain?

- Do they reconcile the two by taking the taxes out of the investment account? Or;

- Do they simply pay the IRS out of their checking account and complain about having high taxes?

Less Friction = Better Performance

Conventional wisdom says that stock picking and efforts to time the market simply do not work. A better and more basic approach may be to focus on the amount of friction facing an investment portfolio. Reducing friction is both doable and effective—potentially boosting performance while providing that elusive “edge” over other investors.

Jason Chalmers is a Director at Cohn Financial Group.