For Wall Street firms, retail traders are attractive market participants because they tend to be less informed about underlying security values and the true trading costs they might be incurring. To take advantage of the retail market, broker-dealers design strategies (such as low-fee and no-fee trading platforms) to increase retail trading. Trading in equity options is particularly attractive to individual investors because of its considerable embedded leverage and the opportunity it presents for lottery-like wins. The marketing strategies have been successful, as retail trading in options has grown from $20 billion in 2010 to $240 billion in 2020.

Empirical Findings

The December 2022 study Losing is Optional: Retail Option Trading and Earnings Announcement Volatility found that retail investors displayed a trio of wealth-depleting behaviors: They overpaid for options relative to realized volatility, incurred enormous bid-ask spreads (the typical percentage half-spreads were about 8%) and sluggishly responded to announcements, even as their prices predictably decayed. These behaviors resulted in losses of 5%-9% on average. Similarly, the authors of the April 2022 study Retail Trading in Options and the Rise of the Big Three Wholesalers found that over the period November 2019-June 2021, after trading costs retail trades lost more than $4 billion! Consistent with that finding, they also found that option market makers earned substantial profits by trading against retail order flow—justifying their payments to brokerage firms for order flow that incentivizes the promotion of the trading and for the commission-free trading that encourages it.

The dramatic increase in options trading raises the interesting question of whether that increased activity has an impact on the volatility of the underlying assets. The writers of the options undertake trades to hedge their positions—options market makers hedge their net positions (gamma hedging) and can transfer net price pressures from one market to the other because these dynamic hedging strategies entail buying (selling) the underlying asset when the option price increases (decreases).

New Research

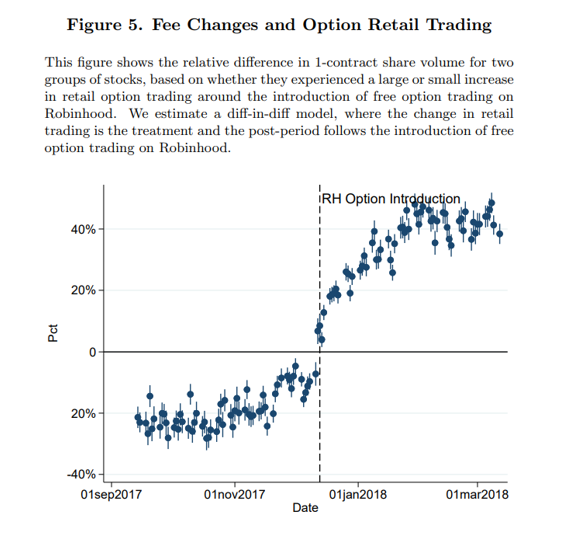

Marc Lipson, Davide Tomio and Jiang Zhang, authors of the March 2023 study A Real Cost of Free Trades: Retail Option Trading Increases the Volatility of Underlying Securities, examined the link between retail trading in options and the volatility of the underlying assets. They focused their analysis on the dramatic fee reduction experienced by retail traders when Robinhood introduced free options trading in January 2018. Fees (on other platforms) that ranged between $11 and $28 an option on discount brokerages became zero. The data sample covered the period June 2017-June 2018—six months before and after Robinhood’s option introduction—and included all ordinary shares of U.S.-listed companies and exchange-traded funds (ETFs) that had underlying options. Here is a summary of their key findings:

The elimination of fees dramatically increased options volume.

Volatility increased, and more so for stocks that saw a greater increase in retail options trading—naive traders are more likely to herd, leading directly to volatility in the markets they trade in—a 10% increase in option retail volume increased idiosyncratic volatility by 1%. The increase in volatility was greater for stocks where there was a greater buy/sell imbalance and higher market maker inventories. Stocks for which options retail trading increased the most experienced an increase in volatility that was 4% larger than the other stocks. In the lowest quintile, where options had a low relative price, the change in volatility was an increase of about 60% versus about 14% in the highest.

Another interesting finding was that stocks experienced an increase in retail trading in the options market became more liquid in the stock market despite an increase in their idiosyncratic volatility—an increase in “noise trading,” amplified by the leverage granted to retail investors by options, suggests that those stocks should also experience an increase in market liquidity. Thus, informed traders can more successfully trade without moving prices. Specifically, stocks in the top tercile for an increase in retail options trading exhibited a quoted (effective) bid-ask spread that was 1.8% (0.8%) smaller.

Their findings led the authors to conclude: “Retail investors increase volatility on the stock market indirectly by trading in the option market. In fact, thanks to the leverage embedded in options, their choice to trade in the option rather than the underlying market may magnify the effect of retail trades on the volatility of the stock market.”

Trading in equity options is attractive to individual investors because of its considerable embedded leverage and the opportunity it presents for lottery-like wins. This allure persists even though there now is a large body of research demonstrating that options trading has transferred billions of dollars from the wallets of retail investors to the pockets of the market makers in those options. That explains all those commercials from broker-dealers touting the elimination of commissions that has fueled a retail participation boom in financial markets, a rise in day trading and the “gamification” of investing.

The success of the zero-commission business model relies on payments for order flow from intermediaries that execute retail orders. That model incentivizes brokerages to induce more trading. Given that retail investors are basically uninformed and have a preference for lottery-like investing, wholesalers (like the casinos in Las Vegas) are extracting billions in spreads from the pockets of naive individuals who are engaging in something that is more akin to gambling than investing. Since bid-ask spreads on options exchanges are considerably higher than those on stock exchanges, market makers that receive retail buy and sell orders are likely to benefit more from executing transactions in options, often crossing these trades. Adding to the losses caused by expensive trading is that naive retail investors fail to optimally exercise options.

While the new generation of retail investors are tech-savvy, they are, nonetheless, uninformed amateurs who act more like gamblers in casinos than investors in capital markets. The result is that their options trading is highly unprofitable to them, but highly profitable for the wholesalers making markets in the options and paying for the order flow. Forewarned is forearmed.

Larry Swedroe has authored or co-authored 18 books on investing. His latest is “Your Essential Guide to Sustainable Investing.” All opinions expressed are solely his opinions and do not reflect the opinions of Buckingham Strategic Wealth or its affiliates. This information is provided for general information purposes only and should not be construed as financial, tax or legal advice.