By Isobel Finkel

(Bloomberg) --You know your 60:40 asset allocation is dead. But do you know why?

In a fresh defense of professional stock pickers from the team that brought you “ passive investing is worse than Marxism,” analysts at Sanford C. Bernstein & Co. warn investors that the two-decade negative correlation between equities and debt is starting to unravel.

Yesterday’s unusual market moves would seem to lend urgency to the thesis, published earlier in the week. The S&P 500 ended the day 0.9 percent down at the same time as Treasuries sold off.

Funnily enough, this is where the New York-based brokerage says active asset managers come in. Investors will need guidance to pick their way through the new environment, according to Bernstein analysts led by Inigo Fraser Jenkins.

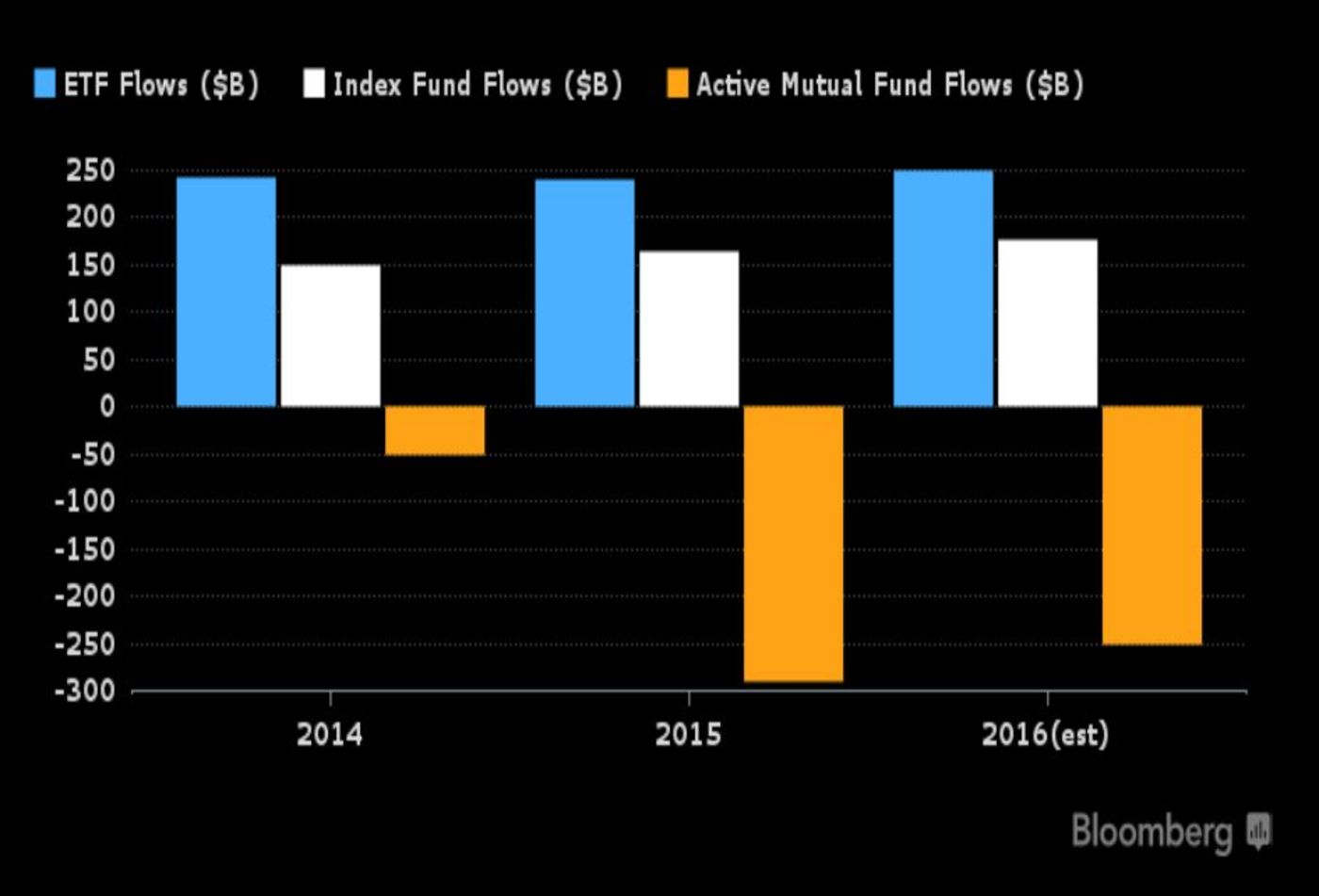

Passive Is Boring

Berstein’s is the latest in a series of bold claims by active fund managers touting their superiority over passive competitors. Computers will never be able to spot patterns like humans can, one money manager asserts. ETFs are “ weapons of mass destruction,” in the words of another. A more common refrain holds that passive investing is boring.

The question is whether this latest argument will be any more persuasive than its predecessors. In the first four months of this year, investors pulled nearly $75 billion from actively managed equity mutual funds, while adding nearly $200 billion to index-tracking passive vehicles, like exchange-traded funds.

The Bernstein analysts wrote that even though bonds and stocks have been delivering positive returns, they’ve actually been moving in opposite directions for much of the last two decades, providing free portfolio diversification to the casual investor.

Over the period in question, the assets “have been more negatively correlated than at any point since 1760,” they wrote. When that’s no longer the case, people will have to try harder than just buy and hold stocks and bonds.

Do Correlations Matter?

Of course, this assumes that investors prioritize the diversification element of the equation. After all -- as the analysts point out -- the 60:40 ratio became popular in the 1950s, well before recent market behavior would explain it.

If light-touch investment decisions have been driven instead by their returns, a shift in correlations per se may not be enough to sway them. Why? Because index tracking funds tend to do better than humans. The math is stacked in their favor.

“Ultimately this is a massive problem for society,” the analysts write, in echo of the utilitarian logic they used last year to dismiss passive investing as “worse than Marxism”: “Policy makers should care about active fund management because of the role it plays in allocating capital in the economy. This action is a force for social good,” they wrote back in August.

This time around, the appeal is to investors’ pockets. “The idea that it is somehow a low risk approach to asset allocation is wrong, and we think that investors will increasingly reject it as a default.”

To contact the reporter on this story: Isobel Finkel in Istanbul at [email protected] To contact the editors responsible for this story: Samuel Potter at [email protected] Eric J. Weiner