Transitioning advisors—whether leaving a wirehouse or IBD to start their own firm, or to join an existing firm—will need to repaper their book of clients to the qualified custodian leveraged by the new RIA. This repapering process is always the most daunting task for any transitioning advisor. Why? Because it requires contacting each and every client and inconveniencing them for not just one signature, but several.

In speaking with advisors contemplating a move, we do our best to set their expectations and highlight the work they have ahead of them. Many advisors will push back right away and say, “You don’t understand—I have a relatively simple book. I only have 100 clients, and they love me! They will sign whatever I ask. It will be painless.” They are envisioning a “simple” spreadsheet with 100 rows, containing name, address, phone number and email address for each client. What they don’t realize is that spreadsheet must track account applications for the new custodian, not household applications. If each of their clients has, on average, five accounts per household, their mental spreadsheet has just grown from 100 rows to 500 rows before we’ve collected any data.

Further, these advisors are failing to appreciate that beyond just basic contact information for each owner of an account, each account type will require different information in order to open the accounts. For example, trust accounts will require the Tax ID, date of trust, state of trust, and information not only on each trustee, but the grantor of the trust as well. An inherited IRA, for example, will not only need information on the account owner and each beneficiary, but will require information on the original depositor as well. Business accounts must be classified as operating or nonoperating, must indicate in which state the entity was organized, the title and role of each owner of the account, and may also require copies of the articles of incorporation for each entity. Multiply this level of information by every client in the advisor’s book, and you can see that things can get complicated very quickly.

The timing and method by which the advisor can collect this information from each client will depend on whether their exit from their former firm will be under the Broker Protocol or not. We have previously written about the nuances of a Protocol vs. Non-Protocol transition. Under either scenario, advisors cannot contact clients and notify them of their move until after they have resigned from their former firm. Advisors envision a smooth dialing process: call Client A, notify them of the move, hang up, send the paperwork for signature; call Client B, notify them of the move, hang up, send the paperwork for signature; wash, rinse, repeat. But it’s not that easy.

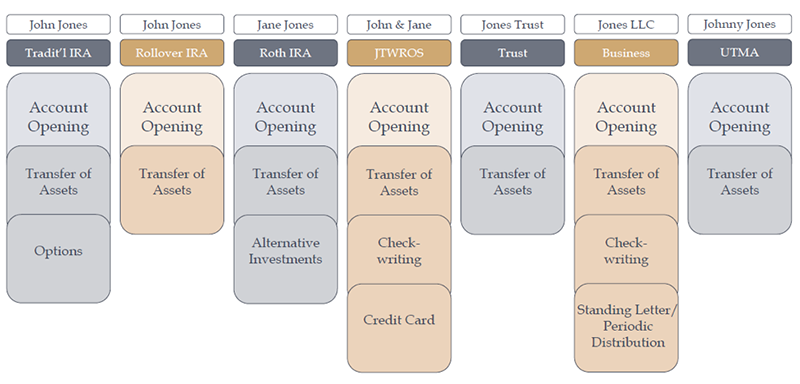

There is an additional paperwork complication that many advisors overlook when planning their transition strategy—in order to complete the paperwork and send it off to clients, the advisor not only needs to gather all the client and entity information for each account within the household, they also need to determine which features must be added to each account, as each requires a separate form be sent to the client for signature. For example, say the Jones household is made up of seven accounts—the advisor must know which of the seven accounts holds options; which of the seven accounts needs a checkbook or credit card; which of the seven accounts needs a standing letter of authorization for a periodic distribution to go out on the 15th of every month; etc. Each of these feature forms must be signed by the client.

When totaling the account applications, transfer of asset forms and each feature form for each individual client account, the advisor that assumed 100 client signatures were needed to move their “relatively simple book” now realizes they will need to track close to 1,500 signatures. (The Jones family, depicted above, requires 20 total signatures to transfer their household of seven accounts.)

This process is far from impossible. Thousands of advisors have successfully transitioned their book of clients from one institution to another, and thousands more will successfully transition their clients in the future. But for a successful transition, we believe it is essential to enter into the process with a proper mindset. If an advisor heads into a transition expecting perfection, they are liable to shut down at the first sign of adversity. It is a disservice to allow advisors to begin a transition thinking it will be easy. But with a proper plan in place to account for some of these inevitable complications, advisors on the other end of the transition can proudly say, “I should have done this sooner!”

Matt Sonnen is founder and CEO of PFI Advisors, as well as the creator of the digital consulting platform The COO Society, which educates RIA owners and operations professionals how to build more impactful and profitable enterprises. He is also the host of the popular COO Roundtable podcast. Follow him on Twitter at @mattsonnen_pfi