The Financial Planning Coalition is advocating for new regulatory standards for financial planners, but is investor confusion enough to justify more rules in an arguably already overregulated industry?

The Coalition, which is made up of the CFP Board, the Financial Planning Association and the National Association of Personal Financial Advisors, released a report Monday contending consumers seeking financial planning services are harmed by the lack of regulation of those who hold themselves out as financial planners. Additionally, the coalition noted that consumers continue to be confused and flooded with misleading terms and practices in this space.

“Financial planners are really only regulated on a piecemeal basis at present,” says Janet Stanzak, president of the Financial Planning Association. “The piecemeal regulation really leaves a lot of significant gaps in the oversight of the delivery of the financial planning services,” Stanzak says. She adds that many key services such as budgeting, tax planning, estate planning and education planning are completely unregulated, not falling under any investment, securities or insurance regulations.

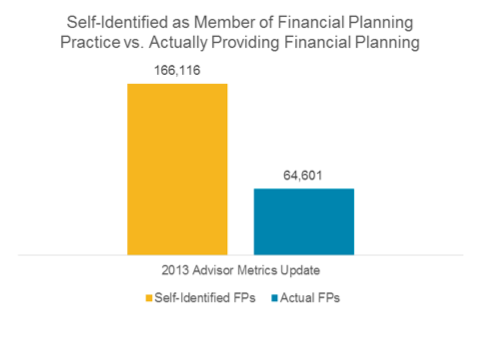

Yet the coalition’s report fails show that investor confusion directly equates to harm or what costs that harm entails. Certainly there are advisors that are perhaps not fully implementing comprehensive financial planning services into their practice while claiming they are practitioners. Cerulli research cited in a 2013 report showed only about 38 percent of self-identified financial planners actually provided comprehensive financial planning services.

But is that really harming investors? Could consumers not just simply switch advisors to get the services they want?

But is that really harming investors? Could consumers not just simply switch advisors to get the services they want?

In response to the question regarding the link between investor confusion and harm, the coalition said “as a result of this confusion about who can provide holistic, integrated financial planning, consumers don’t receive the services they need, want, and expect. Instead, they too often receive narrowly focused advice, the recommendation of a single product as a solution to a more complex financial planning challenge, or advice that is not in their best interests, but rather in the advisor’s interest.”

That still doesn’t take into account those consumers who may only want or need a portion of the full spectrum of financial planning services and therefore choose providers that only provide what they require. And expenses play a major factor here as well, as financial plans can cost thousands of dollars, compared to narrower services that may be less expensive.

The report also cites cases in which fraudsters held themselves out to be financial planners when they were not registered as an example of potential harm. The coalition argues these individuals take advantage of the lack of specific rules around financial planners by using the title to evade regulation. But there are far more cases where people have illegally held themselves out as financial advisors, investment advisors and brokers despite specific laws against such practices. Regulations are no guarantee people will abide by them.

As a possible solution to these perceived regulatory gaps, Ray Ferrara, CFP Board chairman, cited legislation in Nebraska that mandates unless advisors have at least one of a handful of designations, the CFP being amongst those, it’s illegal to call yourself a financial planner

Legislation of that kind across all of the states would go a long way toward helping clear up the confusion caused by those calling themselves a financial planner for their self-benefit when they haven’t demonstrated competency or high ethical standards, he added.

Regulation in this vein seems fraught with complications. And is it really a case of the industry needing more regulation among financial planning service providers? Or just another way to differentiate financial planners (and make expensive designations worth the cost) now that brokers and financial advisors are bringing on financial planning services?