Yesterday, Goldman Sach’s initiated on Delta Airlines (DAL) with a Sell Rating. This stock call comes two months after my note to clients recommending shorting DAL.

While Goldman’s call follows mine, it runs counter to S&P’s (confounding) decision to raise its outlook on DAL’s debt, which led me to think S&P has not done its diligence on DAL.

Goldman’s transportation analyst Tom Kim points to the flagging economic environment and high cost structure of the older carriers as key reasons behind his opinion.

I agree with him and think DAL faces additional pressure from its staggering $22.3 billion in mainly off-balance sheet liabilities, which include $14.1 billion in underfunded pensions and $8.2 in operating leases.

Pressure on DAL’s optimistic earnings outlook is building from within (pensions) and without (economy). Investors should beware.

Not only is Delta underfunding its pensions, it is understating, in my opinion, the cost of its pensions in earnings. Delta’s 2011 earnings would have been lat least $0.09 per share lwoer that if DAL had not chosen to use an abnormally high assumption for the expected return on the assets in its pension plan.

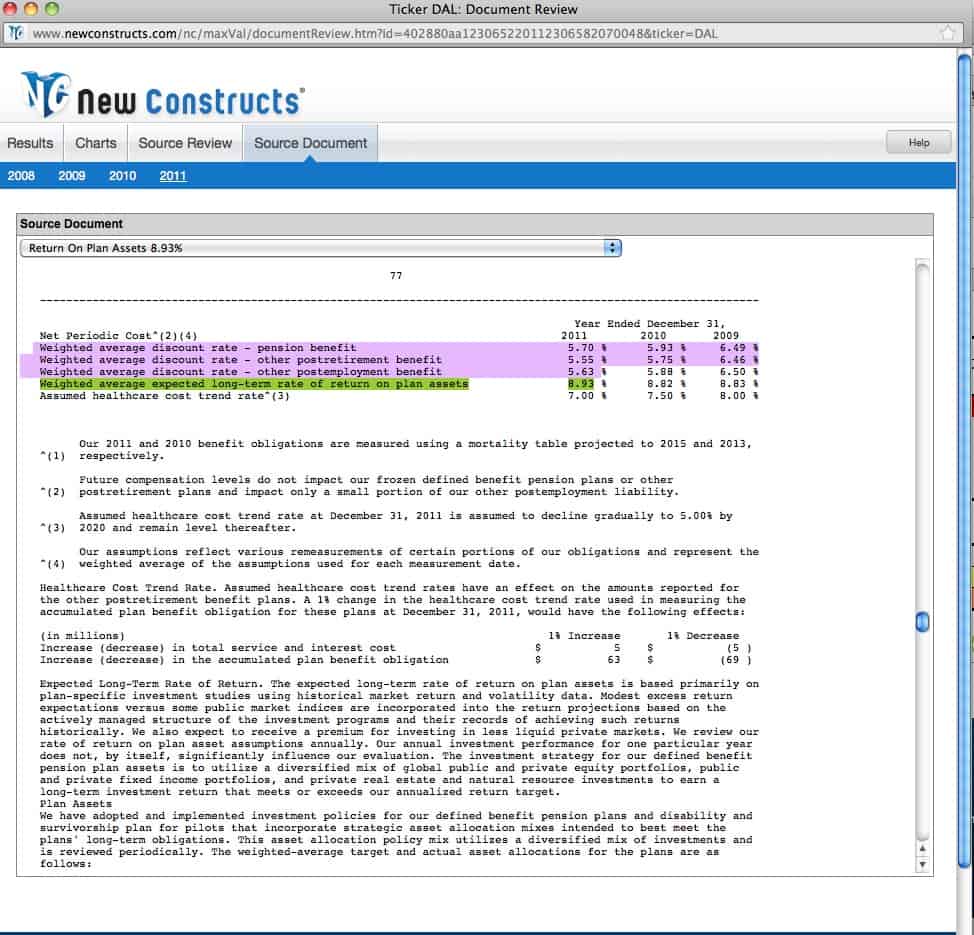

Here’s the scoop: DAL boosted its 2011 earnings by increasing its expected return on plan assets (“EROPA”) assumption for its pensions to 8.93%, up from 8.82% in 2010. Page 78 in DAL’s 2012 10-K filing has the details.

{kind=link}

For readers who wonder whether 8.93% is abnormally high, the answer is yes. Out of the 1,021 companies with pensions that I cover, 98% of them have a lower EROPA. Only 96 of the 1,021 raised their EROPAs in 2012 while 525 lowered and 400 made no changes. In other words, DAL’s EROPA assumption is not only among the highest but it is also rising when the majority is falling.

Raising its EROPA in 2012 looks worse when compared to my estimates of the company’s actual return on plan assets. I estimate 2011’s actual return on plan assets was -0.6%. I estimate the average return since the company emerged from bankruptcy is between 1.5% and 3.8%. These estimates are based on dividing the “Actual (loss) gain on plan assets” by the “Fair value of plan assets at the beginning of the period”. I get that data from the company’s annual reports as detailed in the model used to calculate the actual return on plan assets, which is based on data from the 2011, 2010, 2009 and 2008 10-Ks.

I think S&P should be considering a downgrade not an upgrade. More details are in Bail Out of DAL Before the Stock Crashes.

Disclosure: I am short DAL.