Russ Norwood, CEO and founding partner of Venturi Wealth Management in Austin, Texas, was recently in a meeting with a client and, reviewing his portfolios, discovered three variable annuities, paying a thick commission stream to the agent who sold them.

“Probably close to 20 percent of his assets are tied up in these annuity contracts,” says Norwood, a fee-only advisor. Instead of shrugging his shoulders and moving on, Norwood will likely roll them over to one or more of a new breed of annuities, designed to do away with the commission structure or otherwise make the insurance contracts more appealing to registered investment advisors.

“There’s been a lot of product innovation in the last 10 to 15 years with annuities. For a client to go from a commission-based product to a no-load or low-load product, where you strip out the commission structure, results in substantial savings. In his case, it’d be $10,000 plus a year in savings and internal expenses that would go away.”

Many financial advisors have long shied away from annuities, complaining that the products are too opaque, too complicated and too expensive for clients. The variable indexed annuity has come under particular scrutiny by financial advisors, as it traditionally locks buyers into big, risky bets on the direction of the market

But there is a revolution quietly occurring in the annuity space, as carriers, consultants and distribution companies focus on making these products more attractive to retail financial advisors. Some are creating annuities that work with an advisor’s fee-based platform; others are creating more transparent and useful fixed indexed annuities designed to help give advisors a total view of their clients’ overall investment holdings.

The trend is profound enough that the largest private equity firms are making bets on the space. Apollo Global co-founded Athene, the second-highest-ranked fixed indexed annuity carrier by market share, according to LIMRA, with $118 billion in total assets; Blackstone recently acquired a minority stake in Annexus, an insurance product design and distribution company. Both firms are working on building better fixed indexed annuities using different indices and weightings to make them slightly more customized to an end client’s needs.

Advisors may be suspicious of annuities, but there is no doubt they solve a problem for many clients. The looming longevity crisis no doubt helped push total annuity sales up 14 percent last year to $232.1 billion. Fourth-quarter 2018 sales were the highest quarterly results in 10 years, according to LIMRA. Baby boomers are retiring, just as interest rates are trending higher, which doesn’t bode well for fixed income investors. And with the shift from defined benefit to defined contribution plans across the workforce, investment and longevity risk has fallen back on the consumer.

“The real inconvenient truth for asset managers is that you can’t asset allocate your way out of the (longevity) risks that you’re going to face in retirement,” says Don Dady, co-founder of Annexus. “For the majority of Americans, insurance integrated into your portfolio is the only answer.”

And while insurance carriers are good at selling products, they’re not good at helping advisors incorporate annuities into their clients' portfolios. Companies like DPL Financial Partners, LLIS and The BluePrint Insurance Services act as insurance back offices for advisors. These companies work on addressing advisors’ friction points with annuities and incorporate them into their asset allocations.

“The biggest thing that DPL is doing today that will pay big dividends down the road … they’re really positioning themselves as your outsourced insurance department,” Norwood says.

What’s New in FIAs

In his latest research, Roger Ibbotson, the economist known for his Stock, Bonds, Bills and Inflation chart, argues that fixed indexed annuities have the potential to outperform bonds in the near future and smooth the return pattern of a portfolio, given their downside protection.

A fixed indexed annuity is a contract issued and guaranteed by an insurance company; it is a tax-deferred accumulation vehicle whose growth is benchmarked to a stock market index, rather than an interest rate. It offers capital protection over a three-year period, and they’re typically structured as nine- to 12-year products.

“A fixed indexed annuity provides the variable earning potential like a variable annuity does, but it'’ a hedged product so the insurer can protect themselves on the downside,” Annexus’s Dady says. “We’re able to provide people the opportunity to get a principal protected product with strong upside potential that can produce great income.”

Annexus currently has 15 patents and another 23 patents pending around indexed annuity design. For one, unlike traditional annuity products, Annexus can track daily values of an annuity. The company also uses longer reset options, meaning the firm may not physically credit interest to the client’s account until the end of that time period, which materially reduces its hedging costs and creates greater upside potential.

In addition, the firm is designing annuities based around different indexes than the typical S&P 500 or Dow Jones; recently firms have introduced smart beta and risk management indices.

“What that’s done is opened up a whole world from an investment perspective where we can create different exposures for the client,” Dady says. “All the biggest investment banks on Wall Street and asset managers on Wall Street are now collaborating with us to basically construct indices that follow the traditional investment methodologies that these guys had used to manage money. We’re constructing indices around those techniques and putting it inside a principal protected risk managed product.”

Athene, an insurance provider, licenses indexes from Societe Generale Group, BNP Paribas, Bank of America and Barclays to use in its fixed indexed annuities.

“Historically, most of the crediting strategies within our products were based on the S&P 500,” says Adam Politzer, senior vice president of the product actuary team at Athene. “Now you are seeing the introduction of many new proprietary index strategies. They’re often volatility-controlled, and they take advantage of smart beta concepts to create value for our customers.”

One example is the BNP Paribas Multi Asset Diversified 5 Index, which targets a volatility level of 5 percent. “Historically we may only be able to offer a 5 percent cap on the S&P 500; with this product, because of the lower volatility we are able to offer participation in that index without a cap,” Politzer says.

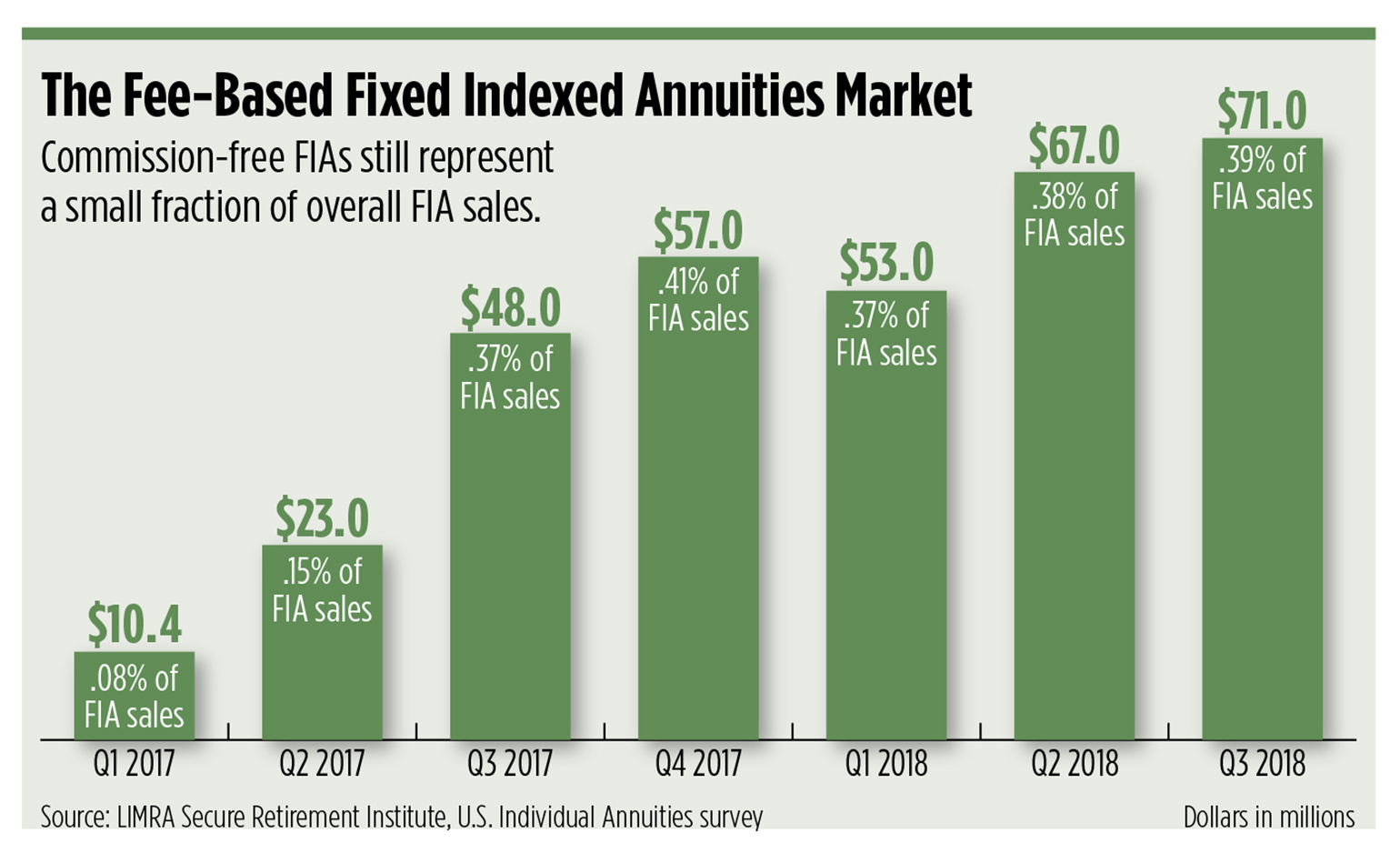

Commission-Free

Jefferson National was perhaps the first to come out with a flat-fee variable annuity marketed toward registered investment advisors, called Monument Advisor, in 2005.

But the number of choices has expanded. David Lau, the former chief operations officer at Jefferson National, realized the need for that kind of innovation went beyond one carrier. So he founded DPL, an RIA insurance network. Lau has worked with close to 15 insurance companies to help them reach fee-based advisors.

“We started working with carriers on a consulting basis to help them understand how to innovate their products in terms of pricing, features, structure, etc. along with modifying their technology to be able to work with fee business rather than commission business and all of that,” Lau says.

DPL recently penned a deal with Jackson National Life Insurance Company to distribute its three fee-based annuity products to RIAs. Lau’s firm also recently partnered with Security Benefit to launch a new commission-free fixed indexed[JK11] annuity, ClearLine.

A number of carriers have come out with so-called “buffer annuities,” a sort of hybrid between variable and fixed indexed annuities, including AXA, Great West, Brighthouse and Allianz. DPL has worked with AXA, Allianz and Great West to provide commission-free versions.

Stripping out commissions can significantly impact expenses, Lau argues. For instance, mortality and expense (M&E) fees on traditional variable annuities can be 135 basis points on average, versus just 20 to 30 basis points[JK12] on the commission-free version.

A Cottage Industry

In addition to changes in product design, a whole cottage industry has popped up to help advisors navigate the insurance offerings, positioning themselves as a kind of “outsourced insurance department,” says financial advisor Norwood.

The BluePrint Insurance Services is an operational insurance platform that provides access and support to advisors around insurance products. The company, established in 2016, helps with the underwriting and delivery of insurance products, and educates advisors as to how they can talk to clients about annuities.

“We recognize that the insurance companies—and really insurance distribution—has a lack of transparency; the products can be complicated; the process is cumbersome and has in the past always involved a lot of paper,” says Matt Meyer, co-founder of The BluePrint. “We understand that, especially for an advisor that manages assets for a client, incorporating something that doesn’t have transparency, that can be complicated, that may require them to know more about their clients’ health history than they wanted to, is a barrier for a lot of advisors.”

The company recently partnered with tru Independence, a consulting and services platform for advisors going independent. Tru advisors will have access to a turnkey program that will help them speak to clients about risk management and insurance.

“The first step is that we’ve got to gain trust, we have to have transparency, we’ve got to pick this thing apart and talk to the advisors and RIAs in a different way. That’s what we’re trying to do,” Meyer says.

It remains to be seen if these annuities will take off in the marketplace; but by creating new, transparent or commission-free products that work for fee-based advisors and their clients, these firms will go a long way toward rehabilitating the reputations of annuities just as more and more investors are going to need them.