Gold is one of the most popular alternative investments. As of mid-April 2023, the two largest gold ETFs had almost $90 billion of assets under management: the SPDR Gold Shares ETF (GLD), with about $60 billion, and the iShares Gold Trust (IAU), with about $29 billion. But what drives investor motives for such a large commitment of assets?

Maximilian Schleritzko contributed to the literature on gold with his March 2023 paper “Households’ Expectations of Returns on Gold,” in which he examined the survey-based expectations of returns on gold of both households and professional forecasters. He sought to determine whether investor expectations aligned with the empirical research findings on the risks and returns of gold.

For the household expectations, he used two sets of surveys eliciting long-term (indeterminant) and short-term (over the next 12 months) beliefs about gold: the Gallup Poll Social Series (2012-2020) and the New York Federal Reserve Survey of Consumer Expectations (2013-2020). For professional forecasters’ expectations, his data is from a survey run by Consensus Economics, which elicits gold price expectations from a set of professional forecasters, economists and banks. Here is a summary of his key findings:

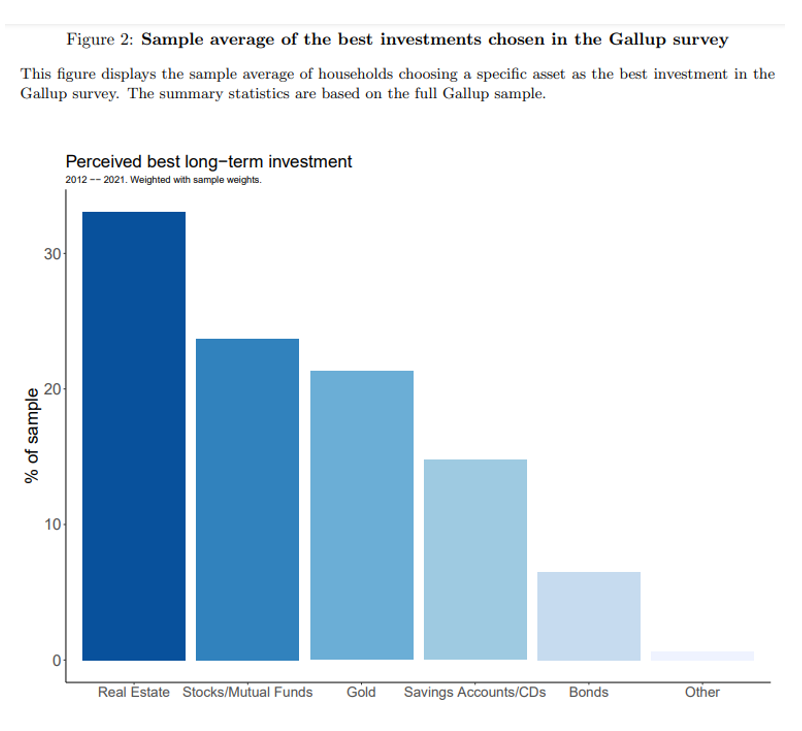

Over the last decade, and currently, around 20% of U.S. households reported gold as the best long-term investment. During that period, gold ranked as the third-most-favored long-term investment, after real estate or stocks and before savings accounts or bonds.

Distrust in the Federal Reserve was the strongest predictor for reporting gold as the best long-term investment across households: Distrusting the Federal Reserve was associated with a nearly 9% higher probability of choosing gold as the best long-term investment.

Households drastically underestimate the volatility of gold and gold’s downside risk. They estimate a return volatility of just 1% while realized volatility has been 15x higher. In addition, gold’s maximum drawdown was 40%. Return expectations were, on average, always positive. And, if households adjusted their inflation, government debt or unemployment expectations upward, they also tended to adjust their gold return expectations in the same direction. Thus, households’ beliefs align with popular investment opinions—gold is an inflation or currency hedge and haven. Households also acted on these beliefs—return expectations were positively correlated with net fund flows in gold-backed funds. Households’ and professional forecasters’ gold return expectations were negatively correlated.

Worse macroeconomic and personal financial expectations were positively correlated (and statistically significant) with beliefs about gold—households perceived gold as an asset that provides superior performance during turbulent macroeconomic times. Interest rates were negatively correlated (though statistically insignificant) with beliefs about gold.

That said, professional forecasters’ expectations are positively associated with gold lease rates, a measure of potential dividend income on gold. This finding is in line with empirical research findings and the model of Robert Barro and Sanjay Misra, authors of the study “Gold Returns.”

Schleritzko noted that his findings are inconsistent with the empirical evidence demonstrating that gold “is insignificantly correlated with consumption or GDP growth, its return is statistically not distinguishable from zero and it did not serve as a hedge in 56 disasters across 19 different countries.” His findings also are inconsistent with the empirical research that over the time horizons of most investors, gold is not an effective hedge against inflation, nor is it a currency hedge. Summarizing, he concludes: “Households have beliefs in line with anecdotal evidence rather than realized returns.”

Empirical Research Findings

In their study “The Golden Dilemma,” covering the period 1975-2012, Claude Erb and Campbell Harvey found:

- The change in the real price of gold was largely independent of the change in currency values; it is not a hedge of currency risk;

- Gold isn’t quite the haven some might think it is: 17% of monthly stock returns fell into the category in which gold was dropping at the same time stocks posted negative returns. As an example of gold’s failing to act as a hedge against bad times, gold prices declined over 30% during the worst of the financial crisis. (I would add that in 2022 when stocks and bonds produced double-digit losses, even though gold outperformed stocks and bonds, it failed to provide a true hedge, as it fell slightly, closing at $1,824 in 2022 after closing at $1,829 in 2021.); and

- There was little relation between the nominal price of gold and inflation when measured over even 10‐year periods—it’s not an inflation hedge except over the very long term.

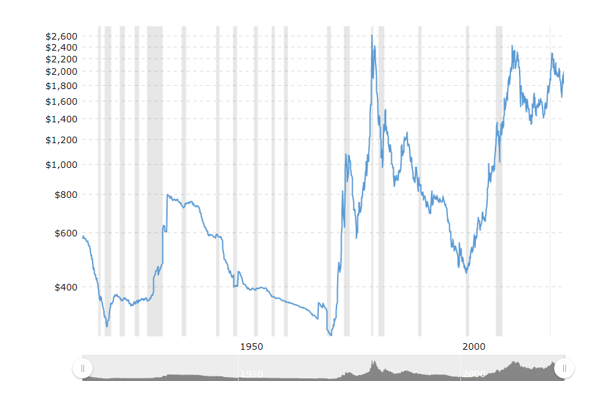

Here’s an example with an even longer period: As seen in the chart below, with gold now trading at around $2,000, it has lost more than 20% of its real value (inflation-adjusted) from its peak of about $2,533 in February 1980. That’s more than 42 years with a significant loss in real value.

As additional evidence that gold is not a good hedge against inflation, Goldman Sachs’ “2013 Outlook” included the following finding: During the post–World War II era, in 60% of episodes when inflation surprised to the upside, gold underperformed inflation.

In their 2023 study “The Golden Rule of Investing,” Pim van Vliet and Harald Lohre examined the strategic role of gold in investment portfolios, focusing on its marginal downside risk-reduction benefits relative to bonds and equities. Their study covered the period 1975-2022. They extended Erb and Harvey’s analysis to include 10 more years, covering the period 1975 (when gold became truly tradable) through 2022. They found:

The real returns for equities (CRSP total market), bonds (10-year Treasurys) and gold were 8%, 3.3% and 1.5%, respectively.

Equities and gold jointly declined in 17% of the months. Conversely, equities were down and gold was up in 19% of the months, roughly resonating with a 50/50 chance for gold to show negative returns in a given negative equity month—gold is not a perfect safe haven when evaluated at a one-month horizon.

At the three-year horizon, gold would have served as a haven in about three-quarters of down markets for equities—again, not a perfect safe haven. In addition, the somewhat limited protection came at a clear cost because gold was down half of the times when equities were up.

The risk of gold was high on a stand-alone basis—its downside volatility was 11.3% compared with 7.9% for equities and 5.3% for bonds. The Sortino ratio, which measures the return per unit of downside volatility, was 1.01 for equities, 0.62 for bonds and only 0.13 for gold. Judging by the loss probability over a one-year horizon, gold also was riskier (49.7% chance of loss) than both equities (24.9%) and bonds (34.6%). Notably, bonds had a greater probability of loss than equities, though lower than that of gold. Judging by the expected loss over a one-year horizon, gold was riskier (-6.1%) than both equities (-3.1%) and bonds (-2.5%). Finally, judging by the minimum return over a one-year horizon, gold was riskier (-46.1%) than both equities (-42.2%) and bonds (-25.3%).

When van Vliet and Lohre examined adding an increasing allocation of gold to a traditional stock and bond portfolio (with annual rebalancing), they found very little evidence of any real net benefits. In addition, allocations above 5%-10% not only reduced returns but also increased downside risk.

Investor Takeaways

Schleritzko demonstrated that retail investors’ interest in gold is motivated by their beliefs that gold is a safe haven asset in bad times and acts as a hedge against both inflation and currency risk. Unfortunately, in each case, those beliefs are contradictory to the empirical evidence.

While gold might protect against inflation in the very long run, 10 or 20 years is not "the very long run." And there is no evidence that gold acts as a hedge against currency risk. As for being a safe haven, Erb and Harvey noted in their study: “In the shorter run, gold is a volatile investment which is capable and likely to overshoot or undershoot any notion of fair value.” Over the 17-year period 2006-2022, the annual standard deviation of the iShares Gold Trust ETF (IAU), at 17.2%, was higher than the 15.6% annual standard deviation of the Vanguard 500 Index Fund Investor Shares (VFINX). In addition, it experienced a maximum drawdown of almost 43%; safe havens don’t experience losses of that magnitude.

That said, there have been periods when gold did act as a safe haven, just not reliably. It, nonetheless, cannot be considered portfolio insurance because insurance is meant to always be there when needed. Investors seeking to diversify their portfolios away from the risks of traditional stocks and bonds should consider other assets that have no or low correlations to stocks and bonds but have higher expected (though not guaranteed) real returns. Examples include reinsurance funds (such as SRRIX, SHRIX and XILSX); private, senior secured, sponsored (by leading private equity firms) floating-rate credit funds (CCLFX); and AQR’s style and risk premium funds (QSPRX and QRPRX).

Larry Swedroe has authored or co-authored 18 books on investing. His latest is Your Essential Guide to Sustainable Investing. All opinions expressed are solely his opinions and do not reflect the opinions of Buckingham Strategic Wealth or its affiliates. This information is provided for general information purposes only and should not be construed as financial, tax or legal advice. LSR-23-488