No doubt you’ve noticed gold’s recent bullishness. At first glance, you’d think gold supplies are tightening. At least that’s what casual observers of the gold futures market might think.

You see, there’s this thing called contango. A contango exists when a contract calling for delivery in a distant month trades at a premium over a contract with a nearby expiration date. This is the normal situation for the gold futures market. A contango typically approximates the carrying costs associated with holding bullion until its putative delivery date. Carrying includes the payment of storage and insurance fees, together with the cost of money (read: interest).

But here’s the thing: Contango isn’t constant. Many observers equate the size of a contango with the supply/demand for balance for a commodity. And that’s why some gold aficionados have been getting excited about bullion’s prospects. They’ve noticed a distinct narrowing in gold’s contango. For storable commodities, a shrinking spread typically signals tightening supplies. Or read another way, increasing demand.

How’s that? Well, when people are anxious to have something, they don’t want to wait for delivery, so they bid up the price for the nearby deliveries. That’s certainly what we’ve seen, off and on, in the oil market of late. But gold’s a different animal.

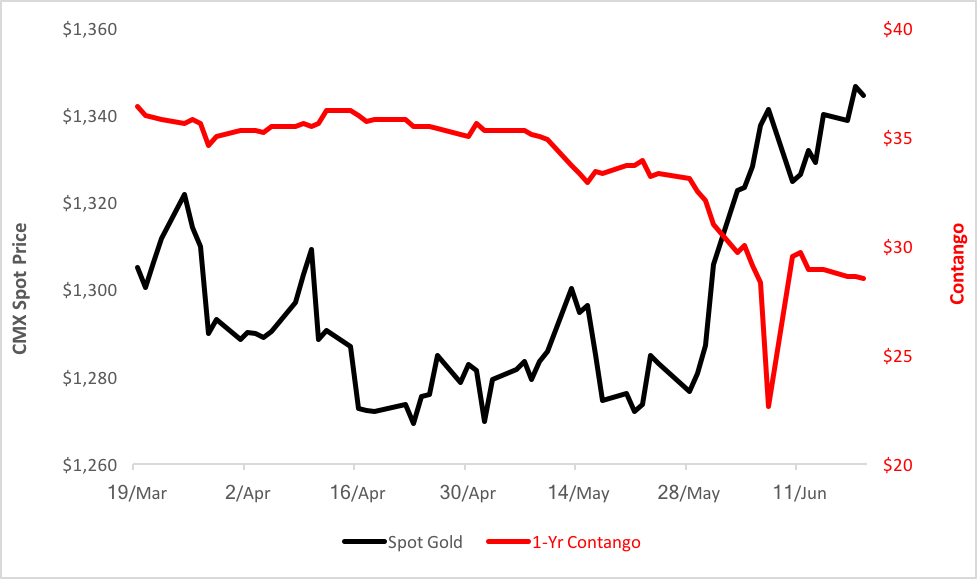

Let’s not get ahead of ourselves. Here’s what the gold market’s done recently:

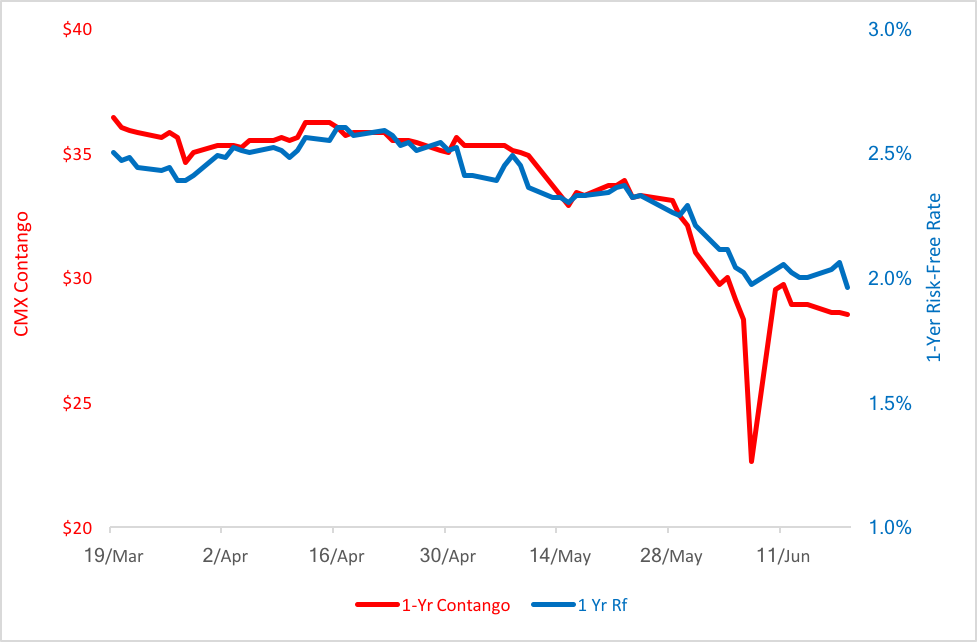

Notice at the end of May how gold’s spot price shot up? And how the one-year contango slumped? Now, you might be tempted to think gold supplies were drying up. But you’ve got to keep something in mind. Since storage costs for gold are negligible (at least for size traders), carrying costs are really driven by the cost of money—interest rates. If you track the gold contango against the risk-free (Treasury) rate, you get a very strong correlation:

So, is there anything to gold’s recent rally besides the decline in yields? Is gold in short supply? Nope. Not really. So cool your jets, gold bugs.

Here’s the deal. The gold market’s been used as a money market proxy by traders for decades. They exploit a gold contango to create synthetic T-bill positions by buying spot gold and simultaneously selling a distant futures contract.

As an example, look back three months. On March 19, the March gold contract—essentially the spot price—closed at $1,305. The April 2020 contract settled at $1,342.90, a premium of $37.90, or 2.90%. Roughly annualized, that translates to 2.68%, a bit of a premium over the then-current 12-month T-bill yield of 2.50%.

If you’ve got a bunch of cash in this low-yield environment, an 18 basis point premium ain’t nothin’ to sneeze at. By purchasing spot gold and selling an April 2020 gold futures contract, traders would be protected from price risk because they’re holding the physical metal they’re obliged to deliver in 2020. They’d then pocket the premium. After costs, of course.

Obviously, not everybody can do this. You need big bucks to pull off a cash-and-carry operation like this, as well as the means to store bullion to await delivery per the terms of the futures contract. These financial hurdles help explain the contango’s premium over T-bill yields. The operation makes sense only if one’s carry costs are well under 0.18%.

This is not to say that gold isn’t worthy of a look. It certainly is. Technically, gold is setting up for a test of the $1,555 level. That, if attained, would be a gain of more than 12%. ETF investors have myriad choices to play gold on the upside. Two of the most actively traded issues include the bullion-backed SPDR Gold Shares (NYSE Arca: GLD) and the futures-based Invesco DB Gold Fund (NYSE Arca: DGL).

Brad Zigler is WealthManagement's alternative investments editor. Previously, he was the head of Marketing, Research and Education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.