Federal Reserve Chair Janet Yellen, advancing beyond her ever-important mandate of promoting the dual goals of full employment and price stability in the world’s largest economy, appears to have stepped into the role of the country’s Chief Investment Strategist. Testifying in front of Congress, Yellen called out the valuations of senior loans and high yield bonds as potentially excessive but acknowledged that prices for a wide range of assets, including stocks, bonds and real estate, “remain generally in line with historic norms.” So much for the days of Fed speak.

Who am I to quibble with the planet’s most powerful figure in the financial world? Most—but not all—asset classes are trading reasonably in line with or slightly elevated to historic norms. Leveraged loans still appear relatively cheap based on historical spreads to short-term rates.

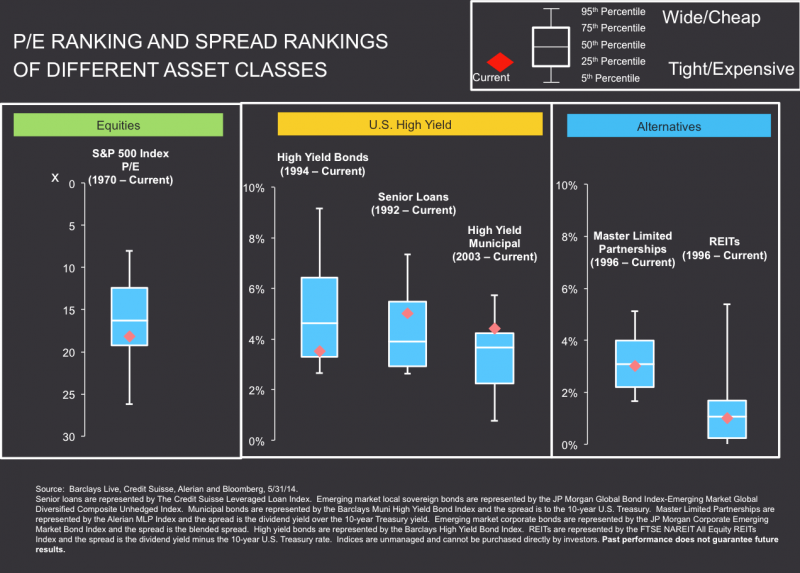

The chart below illustrates this point. To explain how to read the chart, first let’s focus on the current price to trailing 12-month earnings of the S&P 500 Index (as represented by the diamond). We compared the current P/E of the S&P 500 Index to the range of price-earnings multiples experienced by the Index since 1970 (as represented by the length of the box, with the whiskers representing the 5th percentile extremes on both ends). Given a current P/E of 18.2x versus a historical median of 16.3x, the current valuation of the S&P 500 Index appears slightly elevated by this metric and the diamond falls at the bottom of the box.

Turning our attention to more classic income-producing assets, we compare the current yield spread between each asset class and its respective benchmark (diamond) with its historical range (the length of the box, with the whiskers once again representing the 5th percentile extremes on both ends). To Yellen’s point, domestic high yield bond spreads appear tight by historical standards while other assets like real estate investment trusts and master limited partnerships are well in line with long-term averages.

But what about senior loans? The chart shows the diamond sitting near the top of the historic range spread. While the nominal yield for the asset category of near 5% may be near an all-time low, the spread between senior loans and short-term interest rates is still quite wide. Importantly, corporate balance sheets remain generally healthy.

We’ll pick and choose when we listen to Chairwoman Yellen. The most important thing we heard, irrespective of her call on senior loans, is that rates will remain low for the long term. To paraphrase my colleague Krishna Memani after the last FOMC meeting, Fed policy won’t change for a while and the volatility-killing, credit-working, risk-assets-appreciating environment will persist.

DISCLOSURES

The S&P 500 Index is a market-capitalization weighted index designed to measure the performance of the 500 largest stocks in the U.S. High yield bonds are illustrated by the J.P. Morgan Domestic High Yield Index, which tracks the investable universe of domestic below-investment-grade bonds in the U.S. Senior Loans are represented by the Credit Suisse Leveraged Loan Index, which is a composite Index of senior loan returns representing an unleveraged investment in senior loans that is broadly based across the spectrum of senior bank loans and includes reinvestment of income (to represent real assets). High Yield municipal bonds are illustrated by the Merrill Lynch BBB Municipal Bond Index, which is an index designed to measure the performance of below-investment-grade municipal bonds. BBB is the highest grade of rating by Moody’s that is considered below investment grade. Master Limited Partnerships are illustrated by the Alerian MLP Index which is a composite of the 50 most prominent energy Master Limited Partnerships (MLPs). REITS are illustrated by the FTSE National Association of Real Estate Investment Trusts (NAREIT) equity REITS Index which is an index consisting of certain companies that own and operate income-producing real estate that have 75% or more of their respective gross invested assets in the equity or mortgage debt of commercial properties. The spread of all of the fixed income indices (High Yield Bonds, Senior Loans, and high yield municipals) are spreads over treasuries of yields for these indices. The S&P P/E ratio is a measure of price-per-dollar earnings of the index and is measured against itself. Master Limited Partnerships and REITs are yield spreads over treasuries. Indices are shown for illustrative purposes only, are unmanaged, and cannot be purchased directly by investors. Indices are not meant to predict or depict the performance of any fund. Past performance does not guarantee future results.

Foreign investments may be volatile and involve additional expenses and special risks, including currency fluctuations, foreign taxes and political and economic uncertainties. Emerging and developing market investments may be especially volatile. Investments in securities of growth companies may be volatile.

Investing in MLPs involves additional risks as compared to the risks of investing in common stock, including risks related to cash flow, dilution and voting rights. Each Fund’s investments are concentrated in the energy infrastructure industry with an emphasis on securities issued by MLPs, which may increase volatility. Energy infrastructure companies are subject to risks specific to the industry such as fluctuations in commodity prices, reduced volumes of natural gas or other energy commodities, environmental hazards, changes in the macroeconomic or the regulatory environment or extreme weather. MLPs may trade less frequently than larger companies due to their smaller capitalizations which may result in erratic price movement or difficulty in buying or selling. Additional management fees and other expenses are associated with investing in MLP funds. The Oppenheimer SteelPath MLP Funds are subject to certain MLP tax risks. An investment in an Oppenheimer SteelPath MLP Fund does not offer the same tax benefits of a direct investment in an MLP. The Funds are organized as Subchapter “C” Corporations and are subject to U.S. federal income tax on taxable income at the corporate tax rate (currently as high as 35%) as well as state and local income taxes. The potential tax benefit of investing in MLPs depend on them being treated as partnerships for federal income tax purposes. If the MLP is deemed to be a corporation, its income would be subject to federal taxation at the entity level, reducing the amount of cash available for distribution which could result in a reduction of the fund’s value. MLP funds accrue deferred income taxes for future tax liabilities associated with the portion of MLP distributions considered to be a tax-deferred return of capital and for any net operating gains as well as capital appreciation of its investments. This deferred tax liability is reflected in the daily NAV and as a result a MLP fund’s after-tax performance could differ significantly from the underlying assets even if the pre-tax performance is closely tracked.

Fixed income investing entails credit risks and interest rate risks. When interest rates rise, bond prices generally fall, and the Fund’s share prices can fall. The Fund invests in below-investment-grade (“high yield” or “junk”) bonds, which are more at risk of default and are subject to liquidity risk. Investments in securities of real estate companies may be especially volatile. Because they do not have an active trading market, shares of Real Estate Investment Trusts (REITs) may be illiquid. The lack of an active trading market may make it difficult to value or sell shares of REITs promptly at an acceptable price. Senior loans are typically lower-rated and may be illiquid investments (which may not have a ready market). A portion of a municipal bond fund’s distributions may be taxable and may increase taxes for investors subject to the alternative minimum tax (AMT). Capital gains distributions are taxable as capital gains.

Brian Levitt is the Corporate Economist at OppenheimerFunds, Inc. He is responsible for the development and communication of the firm’s economic outlooks and insights. Mr. Levitt also serves on the firm’s New Product Development Committee.

{kind=link}