Much Equity Investing should be Invested in Such

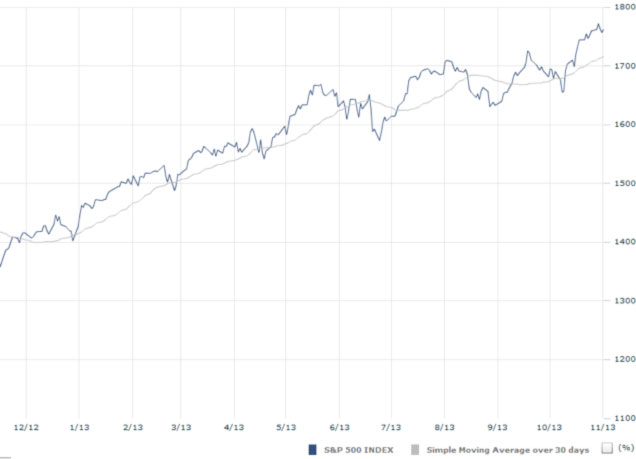

With earnings season rolling along basically in line with expectations, investors continue to focus on macro issues, political policy platforms and the new Fed personnel. As a result, economic data that has largely come in at or below expectations continues to push the equities markets higher. How you may ask? The market appears to be back, at least temporarily, to “bad economic news is good for the stock market” mode.

And, YTD equities have seen $231bn inflows versus a mere $16bn inflows to bond funds.

Therefore, it seems clear that the rally is less about fundamental earnings momentum and has more to do with the improved outlook for public and monetary policy and the U.S. economy.

S&P 500 Index

Source: IDC

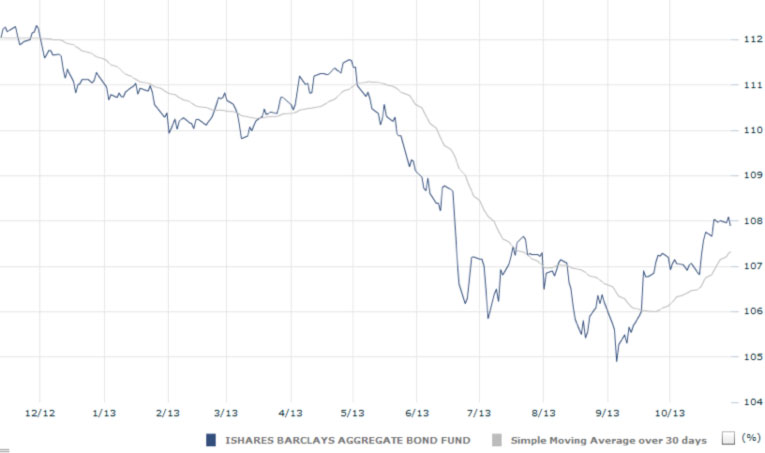

Fixed Income Bruises On-Top Safe Haven

On the rates curve, the question remains, have rates moved too much and too swiftly? As seen in the chart below (AGG – IShares Barclays Aggregate Bond Fund) one can see that price movements began an early re-trace of its sell-off lows in mid-September.

IShares (AGG) Barclays Aggregate Bond Fund

Source: IDC

The rationale for the move is that sluggish economic news means the Federal Reserve is less likely to “taper” or reduce the magnitude of the current quantitative easing (QE) program any time soon.

The market seems to accept that any adjustment in monthly bond purchases (currently $85 billion) is likely to start sometime in the New Year -provided economic data improves on a consistent basis. And at present, the data does not appear to be consistent.

But, nothing lasts forever, not even quantitative easing. Generally speaking, Wall Street probably

won’t be too happy about what may be coming.

No High Points to Bull

Going forward, what is a market to do? As the chart below depicts, the CBOE Volatility Index for the year appears to be in a somewhat mild-mannered band. However, between the massive equity inflows and the potential for quantitative easing taper, ultimately, something has to give. We would expect to see increased volatility in the coming months –to both the equity and bond markets.

CBOE Volatility Index

Source: IDC

Up -does not always signal -Up and Away

And so these days we see a tenuous link between much of the market indicators. If the U.S. growth remains below the markets perceived potential, U.S. equities are likely mispriced and the rates curve is not. However, if growth accelerates to above the markets perceived potential then equities will be viewed as reasonably priced. AND that would mean that either the interest rates market is mispriced or signal that the Fed policy has been too accommodative and therefore either asset or price inflation are the inevitable side effect.

Pioneer Advisors, LLC

The founding Principals of Pioneer Advisors have spent their entire professional careers analyzing and managing assets for several of the world’s leading financial and investment firms. Pioneer Advisors’ team has over 150+ years of Wall Street investment experience providing decision making on $100+ billion of assets.